After a weak August, Indian markets have recovered significantly in September, hitting multiple new highs. This has been driven by several factors, including strong economic growth, robust corporate earnings, solid loan growth, an unprecedented retail investing boom, and the success of a pivotal G20 summit.

Most importantly, successful deals at the G20 summit, spanning sectors like railways, shipping, biofuels, and power transmission, have bolstered investor confidence, positioning India favourably on the global stage.

In Friday's deals, the benchmark Nifty rose half a percent to its new peak of 20202.60. Meanwhile, Sensex also gained 0.5 percent to its new high of 67,861.61.

Both benchmark indices have now advanced around 20 percent from their March lows. Meanwhile, from the COVID-lows hit in March 2020, the indices have given multibagger returns, skyrocketing over 165 percent.

Not just the Sensex and Nifty, broader markets have also given exceptional performance and outperformed benchmark indices, also rallying to new peaks in September.

Just this year so far, while benchmark indices have risen around 11.5 percent, broader market indices Nifty Midcap and Nifty Smallcap have soared over 29 percent and 31 percent, respectively.

Going ahead, experts continue to see strong performance in the Indian markets.

"On the economic front, real GDP growth came in at a four-quarter high of 7.8 percent in 1QFY24 vs. 6.1 percent/13.1 percent in 4QFY23/1QFY23 Better private consumption and investments led to better-than-expected growth, while growth was offset by weak fiscal consumption and real exports. Also, corporate earnings for 1QFY24 came in strong and could support the underlying overall optimistic narrative of India. Nifty posted a beat with EBITDA/PAT growth of 22 percent/32 percent YoY vs. our expectation of 18 percent/25 percent. Once again, the earnings growth was propelled by domestic cyclicals, such as BFSI and Auto. Going forward, we anticipate earnings to remain healthy and pencil in over 20 percent earnings growth for Nifty in FY24. We are positive on Financials, Consumption, and Automobiles," said brokerage house Motilal Oswal in a recent note.

The brokerage has come out with investment ideas under both large-cap and midcap space. Let's take a look.

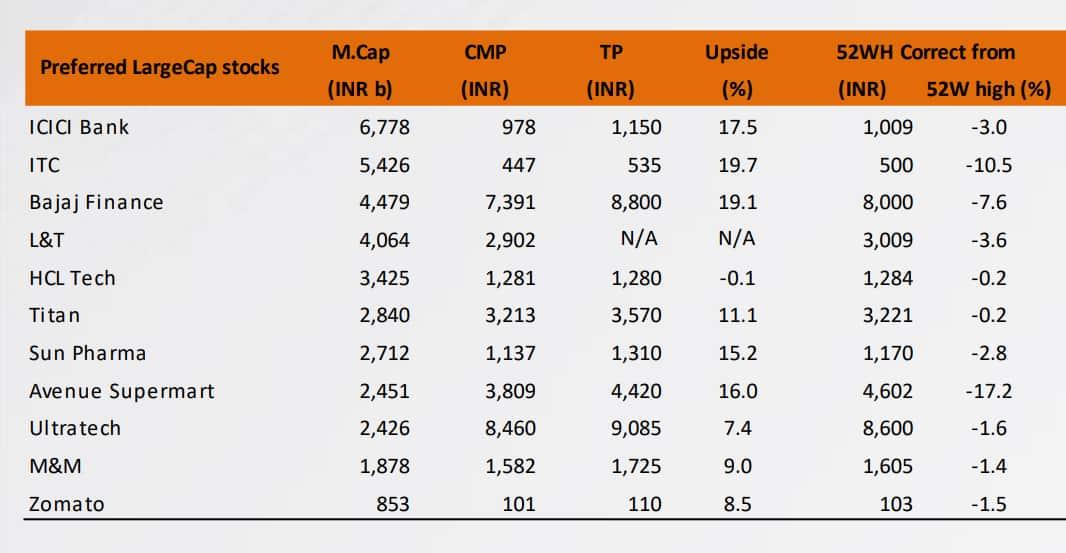

Largecap Ideas

Its top largecap ideas include ICICI Bank, ITC, Bajaj Finance, L&T, HCL Tech, Titan, Sun Pharma, Avenue Supermart, UltraTech Cement, M&M and Zomato.

The brokerage sees the highest upside potential in ITC and Bajaj Finance, over 19 percent followed by ICICI Bank at 17.5 percent, Avenue Supermart at 16 percent, Sun Pharma at 15 percent and Titan at 11 percent. For the remaining stocks, the brokerage estimates single-digit upside potentials.

ITC: MOSL is positive on ITC as a result of (a) better earnings visibility over peers in the next few quarters, (b) inexpensive valuations; and (c) attractive dividend yield. ITC’s earnings outlook is better compared to other large-cap staples players in FY24 and FY25. ITC posted a healthy 24% EPS growth in FY23 and MOSL expects an EPS CAGR of 15% over FY23-25

Bajaj Finance: BAF has made significant progress in optimizing its processes and has made significant structural changes to its technology stack. It estimates an AUM/PAT CAGR of 29%/26% over FY23-FY25 and expects BAF to deliver a RoA/RoE of 4.6%/25% in FY25.

ICICI Bank: ICICI Bank is well positioned to deliver steady earnings, supported by pristine asset quality and strong momentum in business growth. It estimates RoA/RoE of 2.2%/17.9% in FY25 and earnings growth of 17% CAGR over FY23-25.

Avenue Supermart: MOSL believes same-store sales growth is set to recover in FY24, due to: 1) easing general inflation along with raw material cost reduction that may help in reviving discretionary demand; and 2) the company’s strategy to open larger stores as the smaller ones are likely to report a growth plateau after almost three years. Robust store additions (72% footprint additions over FY20-23), healthy cost efficiencies and recovery in discretionary demand could drive growth. It factors in a revenue/PAT CAGR of 26%/27% over FY23-25 aided by 16%/9% growth in footprints/revenue productivity.

Sun Pharma: MOSL remains positive on Sun Pharma backed by its robust innovative products franchise targeted for global markets and superior execution in branded generics markets. It expects overall US sales CAGR of 11% to $2b over FY23-FY25. and the company to exhibit a 10% CAGR over FY23-25. The ROW and emerging markets are expected to witness a CAGR of 12% (in CC terms) over FY23-25 to reach $2.2b driven by factors such as increasing traction in the existing products, increased reach as well as new launches.

Titan: Titan has a strong runway for growth in the consumption space in India, with robust earnings growth visibility and compounding for the long term. Given its sub-10% market share in jewelry and the struggles of unorganized and other organized peers, it sees a promising growth outlook for the firm. Its medium- to long-term earnings growth opportunity is best-of-breed, reflected in five-year sales/EBITDA/PAT CAGRs of 20.3%/24.3%/23.9%.

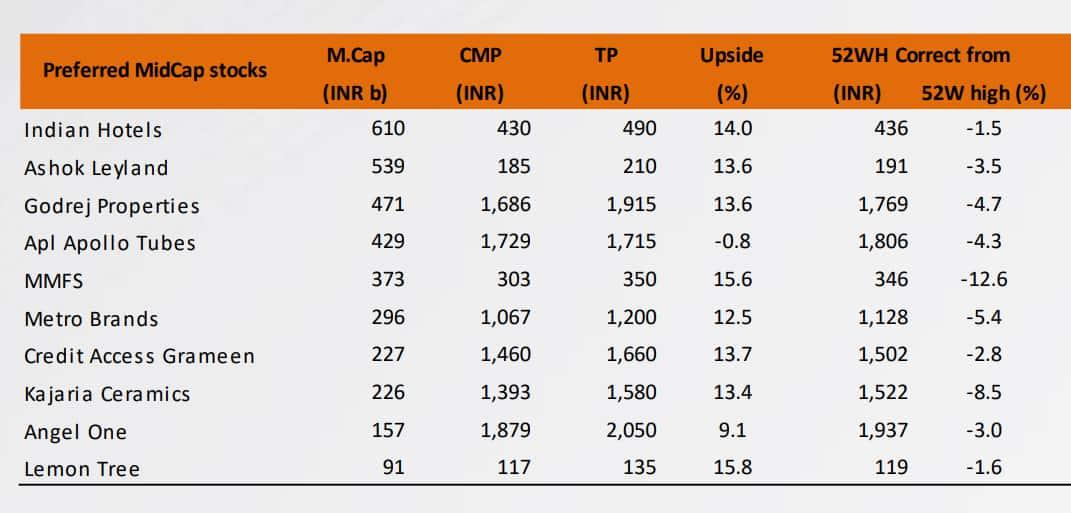

Midcap Ideas

Its top midcap ideas include Indian Hotels, Ashok Leyland, Godrej Properties, APL Apollo Tubes, M&M Financial Services (MMFS), Metro Brands, CreditAccess Grameen, Kajaria Ceramics, Angel One, and Lemon Tree.

The brokerage sees the highest upside potential in Lemon Tree and MMFS, over 15.5 percent followed by Indian Hotels at 14 percent, CreditAcess Grameen, Ashok Leyland, Godrej Properties, and Kajaria Ceramics at over 13 percent each. For the remaining stocks, the brokerage estimates 12.5 percent upside in Metro Brands, 9 percent in Angel One and around one percent downside in APL Apollo.

Lemon Tree: MOSL expects the strong momentum to continue going forward, led by improvement in occupancy and ARR, and strong addition of hotels under management contracts. It expects Lemon Tree to deliver a revenue/EBITDA/Adj. PAT CAGR of 28%/25%/ 43% over FY23-25. Its RoE would improve to 21.9% by FY25E

MMFS: Strong liability franchise and deep moats in rural/semi-urban customer segments position MMFS well to reap the rewards of the hard work that is ongoing in evolving this franchise. It expects a CAGR of 19%/20% in AUM/PAT over FY23-FY25E, with RoA/RoE of 2.3%/15.4% in FY25E.

Indian Hotels: The brokerage expects the strong momentum to continue in FY24, led by improvement in occupancy due to multiple large global events such as G20 and ICC Cricket Men’s World Cup in CY23; improvement in ARR, higher income from management contracts; and value unlocking by scaling up reimagined and new brands. It estimates a revenue/EBITDA/Adj. PAT CAGR of 13%/19%/21% over FY23-25.

CrediAcess Grameen: CREDAG’s robust execution has been vindicated by its resilience across various credit cycles and external disturbances. It will continue to deliver robust return ratios, aided by a strong underlying business model. MOSL estimates an AUM/PAT CAGR of 24%/44% over FY23-FY25, leading to a RoA/RoE of 5.6%/23% in FY25.

Ashok Leyland: AL is the best investment choice in the CV growth cycle, as it has positioned itself to expand revenue/profit pools. A strong recovery in buses and demand improvement in long-haul trucks also augur well for AL, said MOSL. AL aims for near-term EBITDA margin to be in double digits. It expects the benefits of lower steel prices to reflect in the 2HFY24 margin, it added.

Godrej Properties: On a pre-Covid equity base, the company is not far from its 20% RoE target. GPL has done strong business development in FY23 and if these projects are launched on a timely basis, its RoE profile will improve notably as these projects hit P&L in 3-4 years. The firm has highlighted its key strategic objectives - to achieve ₹14,000 crore in pre-sales, fuelled by a robust launch pipeline; and capitalize on its strong balance sheet to boost market share through business development.

Kajaria Ceramics: Lots of positive triggers are being witnessed on the ground, which should help a strong demand pick-up. Management expects demand to pick up from Sep’23 and guided for 14-16% YoY revenue growth along with an EBITDA margin of 14-16% in FY24. It expects 33% earnings CAGR over FY23-25 and projects improvement in return ratios (RoE to be at 22% in FY25E v/s 15% in FY23) and to maintain its premium valuations.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie. We advise investors to check with certified experts before taking any investment decisions.