For the stock markets, the 2023rd year of Christ is beginning on a cautious note.

The global narrative is swinging from an orderly decline to a precipitous crash.

With the last man standing Haruhiko Kuroda (BoJ Governor) falling this week, it is clear that the “crusade” against inflation will continue in 2023 - and money will be expensive and tighter.

This is most likely to reflect in slower economic activities, and aggressive trade and currency conflicts.

The developed markets that have thrived mostly on the steroids of cheap and easy money will show withdrawal symptoms which may include volatility, recession, protectionism, financial instability, etc.

The emerging markets largely dependent on exports to developed markets (commodity or merchandise) shall also suffer collateral damage.

However, the emerging market with strong domestic economies, stable fiscal conditions and stronger financial markets might find themselves in a position to take advantage of the flight of capital from the developed and weaker emerging markets and lower commodity prices.

India, arguably, is placed in the latter category of emerging markets.

It cannot be denied that a precipitous crash in the global markets will hurt the Indian market badly, just like it did during the market crashes of 2000, 2008-09 and 2020.

However, in case of an orderly decline in the global economies and markets, India may stand out again in 2023, just like it did in 2022.

The risks to Indian markets are evenly balanced.

The absence of a bubble in any pocket of the market, low volatility, strong domestic flows, economic growth still close to the past decade’s trend, and stable fiscal and financial conditions support the markets; while the rising probability of a precipitous crash, a deeper recession than presently estimated and the geopolitical conditions taking a turn towards the worst, pose a material threat to the markets.

The investors are therefore faced with high uncertainty in formulating an appropriate investment strategy. I would be extremely untruthful and dishonest to claim that my situation is any better than most of the investors.

Nonetheless, after evaluating the entire situation I have shortlisted the following factors that would support my investment thesis for the next 9-12 months and help me navigate the turbulent waters.

1. There are no signs of a bubble in the Indian equity market.

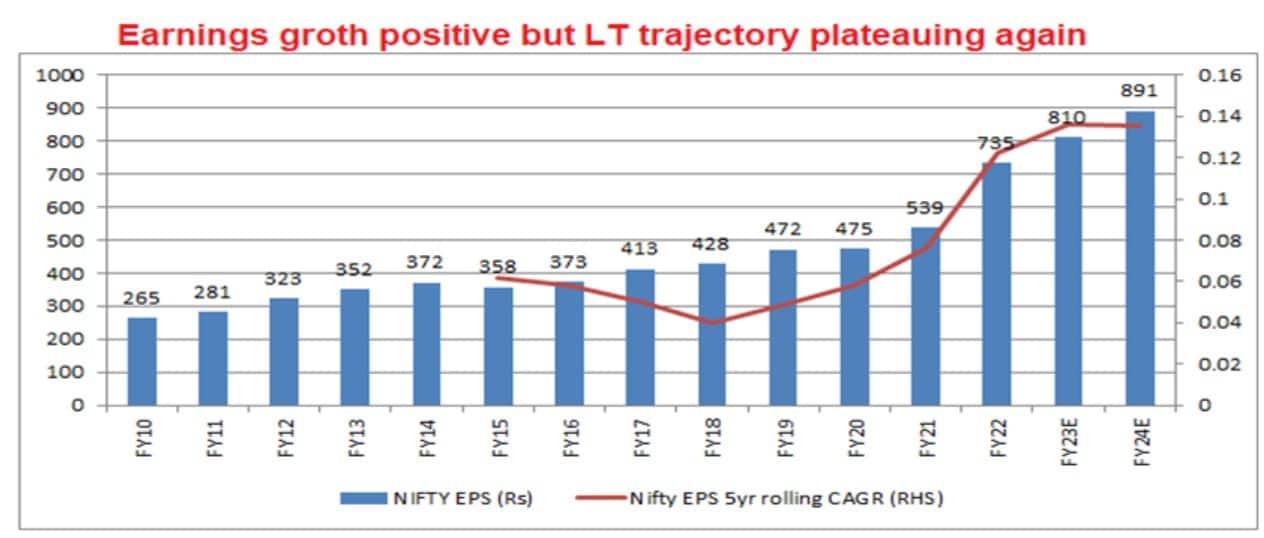

2. The earnings growth is likely to stay positive for at least a couple of more years.

3. Margins may bottom as inflation, rates and USDINR peak sometime during 2023.

4. The leverage in Indian markets is substantially lower compared to 2000 or 2008-09. The chances of a sustained crash are therefore much less this time.

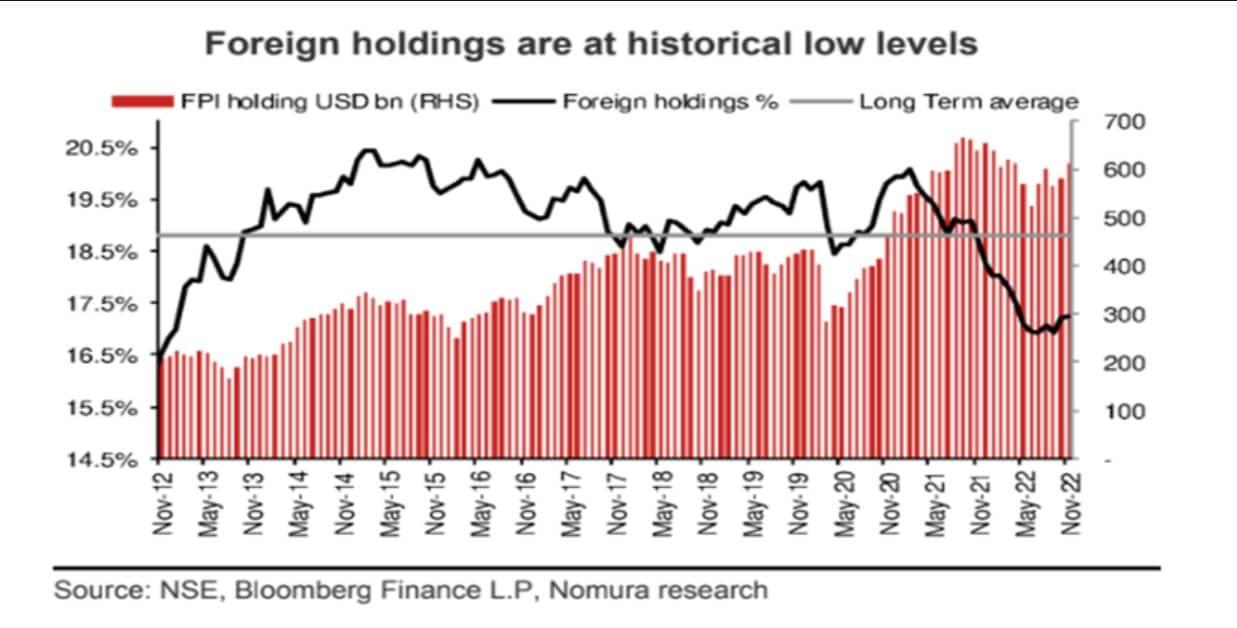

5. Despite the outperformance, foreign investors have not been enthusiastic about Indian equities in the past couple of years. The foreign ownership of Indian stocks is at a multiyear low. Besides, India's weight in MSCI EM has seen a steady increase. The probability of accelerated selling is therefore low.

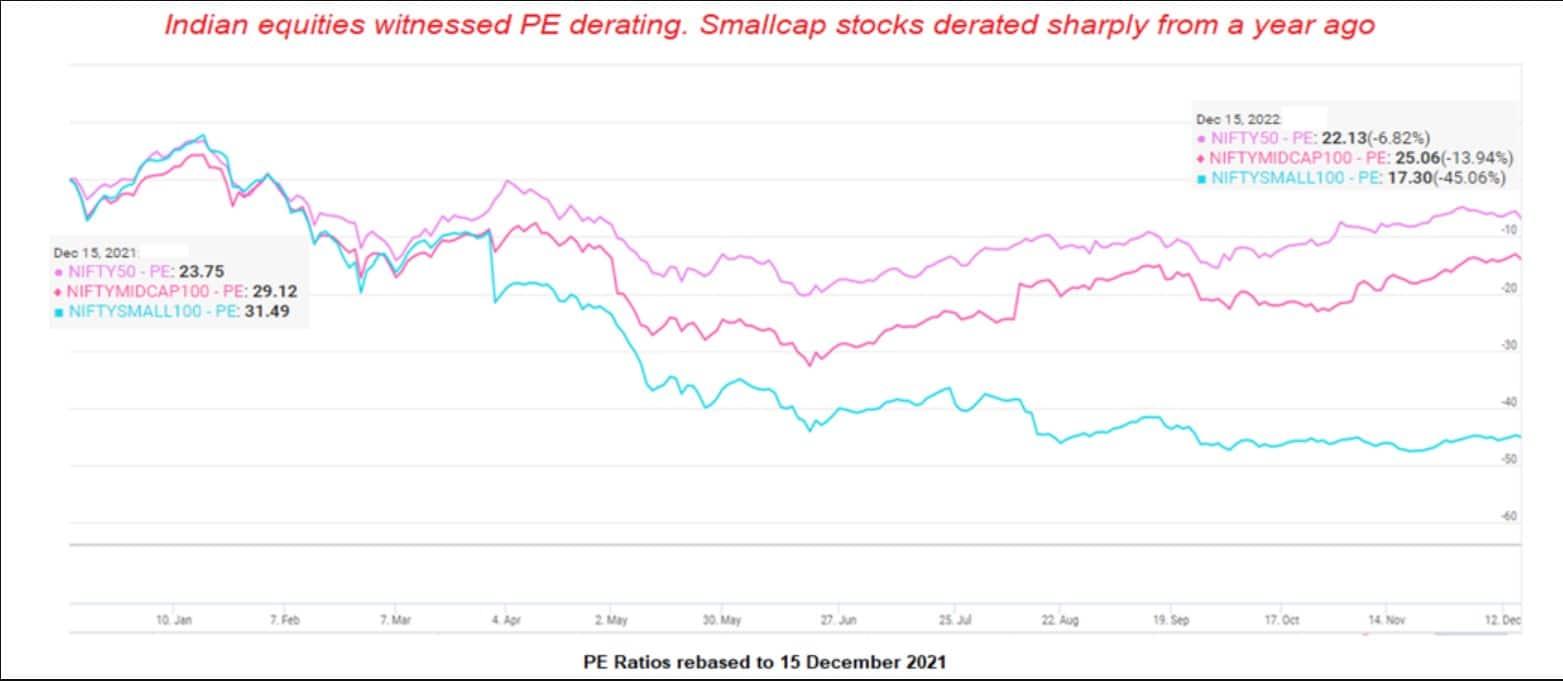

6. The valuations are not cheap though closer to the long-term averages. Given the slower growth and higher bond yields, it is likely that Indian markets may witness some PE de-rating and trade below long-term averages.

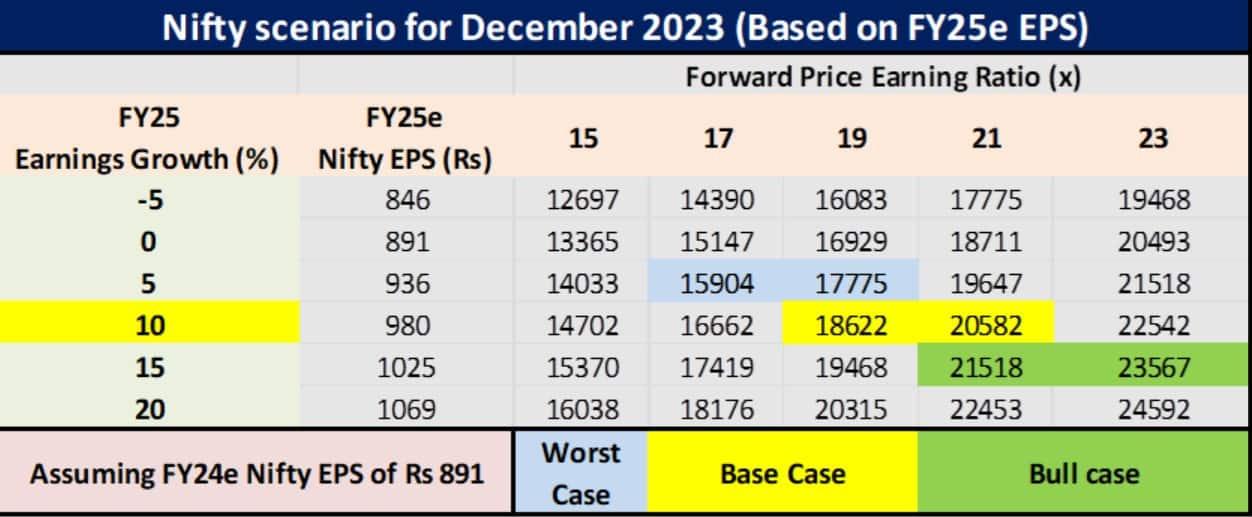

7. The bull case for Indian equities as a whole is weak. The upside from the current levels is limited, given slowing growth momentum and higher rates; whereas a panic bottom could be profound.

8. There are some pockets of the economy (and market) that are witnessing a sustainable transformation. These pockets offer once-in-a-decade type opportunities. Some examples are defence production, biofuels, real estate, manufacturing modernization, self-reliance in intermediates manufacturing, and modern retail. These pockets of growth have been well identified and analyzed, therefore, the risks are mostly known and the growth path is well illuminated.

9. Presently the opportunity cost of holding cash is minimal as liquid funds and short-term fixed deposits offer decent returns. There is no rush to go out and deploy cash in equities and other assets.

10. The developed markets may hit the rock sometime in 2023, though a sustained recovery may elude them for a couple of more years at the least. The stronger emerging markets may find favour with the yield hunters in this scenario.

(The author is a market observer and the director of the Equal India Foundation)

Disclaimer: The views and recommendations given in this article are those of the author. These do not represent the views of MintGenie.