Carmaker Maruti Suzuki reported a 130 percent jump in its net profit in the third quarter of the financial year 2023, beating analyst estimates. On the back of its impressive quarterly results, many brokerages have revised their estimates upwards for India's largest carmaker for FY24 and FY25, while some have also upped their price targets for the stock.

Maruti Suzuki Q3 earnings: Brokerages raise estimates, target prices after profit surges 130%

TL;DR.

On the back of its impressive quarterly results, many brokerages have revised their estimates upwards for India's largest carmaker Maruti Suzuki for FY24 and FY25. Meanwhile, some have also upped their price targets for the stock.

Maruti's consolidated net profit surged to ₹2,391.5 crore in the quarter ended December 2022 driven by higher sales, a strong margin performance, a better product mix, and lower input costs. The auto major had reported a profit of ₹1,041.8 crore in the same quarter last year.

Its total revenue from operations rose 25 percent to ₹29,057.5 crore versus ₹23,253.3 crore in the corresponding quarter a year ago. The EBIT margin of the company also improved 350 basis points YoY to 7.6 percent whereas its profit margin jumped 380 basis points YoY to 8.4 percent.

During the December quarter, the company sold a total of 4,65,911 vehicles, up 8.2 percent YoY. Sales in the domestic market were 4,03,929 units and exports were 61,982 units versus a total sales of 430,668 units comprising 365,673 units in domestic and 64,995 units in export markets in the same period the previous year.

Most brokerages retained their bullish stance on the stock. Let's see what they have to say:

Motilal Oswal

Maruti reported a strong beat in Q3FY23, driven by a better mix (8 percent beat on ASPs) and higher other income, noted the brokerage. Its recently launched products will reflect in the P&L from Q1FY24, however, the commodity price benefit was largely reflected in Q3FY23, said MOSL. It expects continued improvement in performance and response to new products to act as catalysts for the stock.

The brokerage has upgraded FY23 EPS estimates by 14 percent to reflect the benefit of mix and higher ‘other income’, but reiterated the FY24 estimates as the mix benefit is offset by the forex impact. It has reiterated a Buy rating for the stock with a target price of ₹10,500, indicating an upside of 21 percent.

"Good demand and favorable product lifecycle for MSIL augur well for market share and margins. We expect a recovery in both market share and margins in FY24, led by an improvement in supplies, favorable product lifecycle, mix and operating leverage," it said.

Prabhudas Lilladher

The brokerage increased its EPS (earnings per share) estimates by 6 percent for FY23, 3 percent for FY24 and 1 percent for FY25 as it builds in higher realisations led by improved product mix along with volumes for the newly launched Jimny and Fronx.

In Q3FY23, Maruti’s EBITDA margin at 9.8 percent expanded 50 bps QoQ led by better-than-expected realisations driven by increased contribution from UVs and benefit from raw material cost softening, noted the brokerage. The company currently has an order book of 363,000 units of which 33 percent is contributed by new models – Brezza, Vitara, Baleno. Newly launched Jimny (off-roader) and Fronx (compact SUV) have also received good response and deliveries are expected to commence from the beginning of FY24, it pointed out. As per the brokerage, this will lead to increased contribution from UVs in the product mix along with market share gains.

"We remain positive on MSIL as the company will benefit from (1) market share gains and ASP increase coming from filling white spaces in UV portfolio, (2) 260bps increase (over FY23-25E) in EBITDA margins on the back of commodity cost softening and higher UV share and (3) rural revival," explained PL. It has reiterated a Buy call on the stock with a revised target price of ₹10,600 ( ₹10,000 earlier on Sep-24E) at 26x Dec-24E EPS. The new target price implies an upside of 21 percent.

Nirmal Bang

The brokerage has maintained a Buy call on the stock with a target price of ₹11,188, indicating an upside of 28 percent. It remains positive on the stock and factors in EPS CAGR of 37 percent over the next three years.

"We remain confident about market share gains by Maruti as historically also, it has demonstrated its ability to regain lost market share, led by new product launches and network expansion (Baleno and Brezza despite late entrants became market leaders in their respective category, facilitating market share gains). Moreover, it has also addressed the concerns around premiumisation and safety in its recent launches in addition to sticking to its existing value proposition. We are thus factoring in volume CAGR of 15 percent over FY22-FY25E, along with an increase in ASP, led by a higher share of SUVs," explained the brokerage.

Nuvama

The brokerage house upped its target for the stock to ₹11,291 (upside 30 percent) from ₹11,191, as revenue growth came in 10 percent higher than its projections and EBITDA 15 percent above its estimates. Maruti's superior franchise raises hope that it will make a strong comeback, noted the brokerage. It expects Maruti's market share to grow to 48 percent from 45 percent over FY22–24E, as it builds on the potential success of already launched UVs – Brezza and Grand Vitara and the next set of UV launches namely Jimny and FRONX.

"However, competition in UVs is intense with 45 existing models capturing 45 percent of the PV market (compared to 19 models in the hatchback segment). Having said that, semi-conductor shortage is still a bottleneck and can act as a dampener in the near-term as far as ramp-up of its UVs is concerned," it added.

Emkay

The brokerage increased Maruti's FY23E EPS by 7 percent to ₹263 on higher margins and other income assumptions. It retained a Buy call on the stock with a target of ₹10,700 (upside 23 percent) per share from ₹10,500 earlier, based on 27 times core P/E on FY25E EPS and cash of ₹1,260 per share. Key downside risks include macro slowdown, lower-than-expected volumes in new products, higher competitive intensity and adverse movement in currency rates, it noted.

CONTRARIAN VIEW

Kotak

Kotak Institutional Equities, however, maintained a Sell call on the stock with a target of ₹7,850, indicating a downside of 10 percent. It expects Maruti Suzuki's product mix benefit to partly reverse in the coming months. It also sees domestic PV segment demand moderating sharply in FY2024E due to cost headwinds and the waning of pent-up demand.

"We also expect the Ebitda margin to remain below 11 percent over FY2024-25E, as we expect discounts to inch up, especially in the entry-level segment, unfavorable forex, and an uptick in base metals prices," it said.

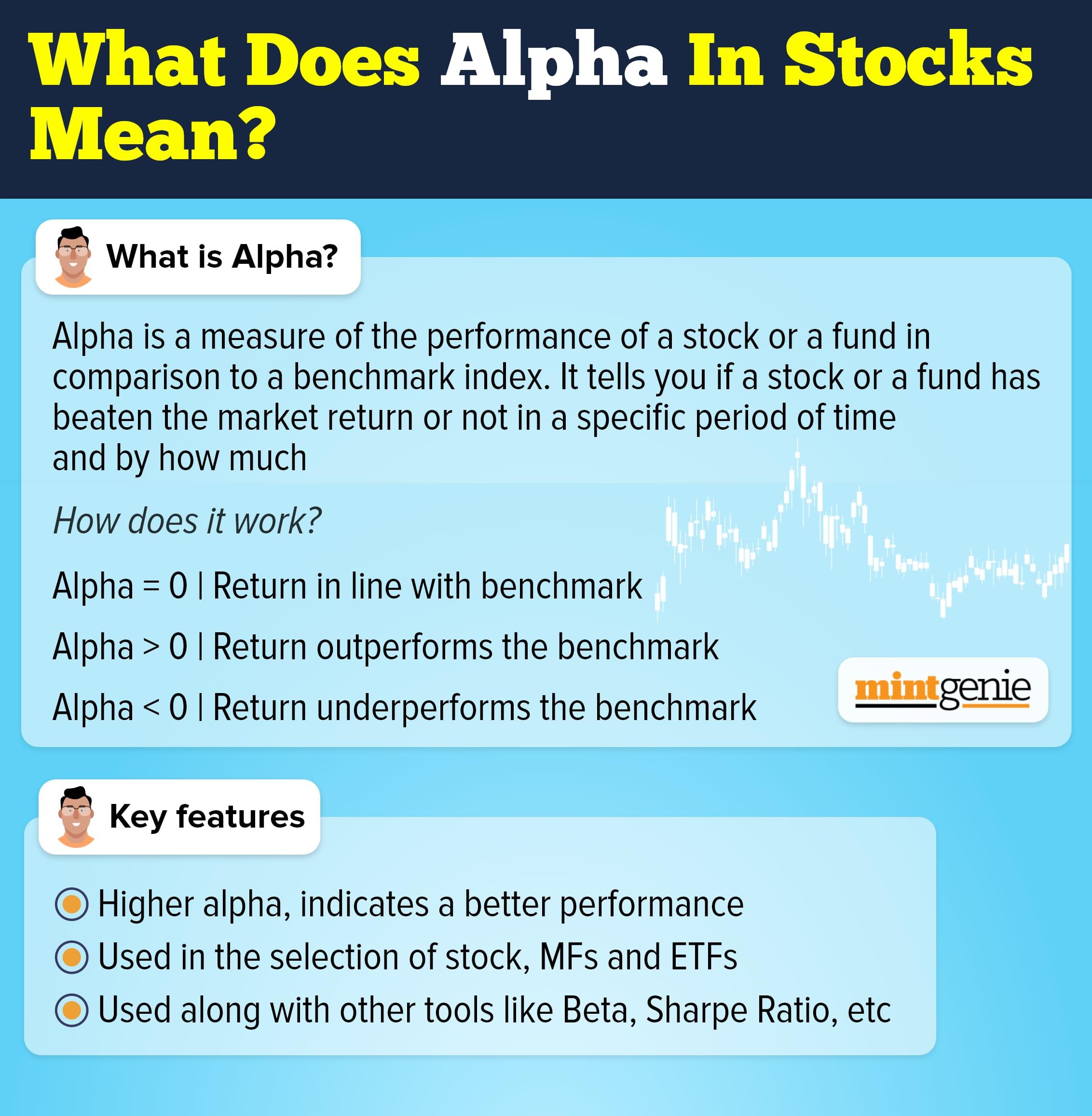

What is alpha in stocks

First Published: 25 Jan 2023, 01:34 PM IST

Topics to follow

Related Stories

Explain Like I am 5

personal finance

What is financial filtration and why do you need it this year? Here are 3 reasons

Anushka Trivedi