With midcap IT services companies gaining focus, in a recent report, global brokerage house Macquarie said it believes that growth outperformance by these firms against India Tier-1 – TCS, Infosys, HCL Tech, Wipro and Tech Mahindra – will continue, but the gap will narrow.

Midcap IT firms to outperform largecaps, says Macquarie; lists 5 stock picks with over 50% upside

TL;DR.

Despite the growth gap narrowing to some extent, it sees midcap IT delivering a higher revenue CAGR than the ‘India Tier-1’. The brokerage highlighted that this is the time to be selective among midcaps.

It said that the Indian IT midcaps have improved their positioning during Covid. While it expects near-term organic incremental revenue for the midcap space to be relatively subdued QoQ and below the high watermark hit immediately post Covid, it sees incremental revenue remaining in positive territory as no kneejerk cuts unlike during the pandemic are expected.

"The more level playing field for India IT Services midcaps and their growing capability to successfully play the same role as the largecaps (i.e., as a cost-efficient and capable outsourcing partner for both new development and maintenance) has been rewarded with a PE re-rating in recent years. We think this is well deserved, but think that the valuations should reflect the differences in both growth rates and risks to growth," explained the brokerage.

Despite the mega deals that the Tier-1 won, midcaps have held their market share at pre-Covid levels, it pointed out.

Overall, the brokerage highlighted that this is the time to be selective among midcaps and not assume that the industry no longer has the benefits of scale. Investors should consider not just return ratios, but also growth as well as the sustainability of growth when considering the valuations of the midcap IT services firms, advised the brokerage.

Its preference is for firms with 1) proven client mining ability; 2) increasing offshore execution; and 3) declining top-client concentration.

Its top midcap picks are Persistent Systems and LTIMindtree (LITM) but its top sector picks remain HCL Tech followed by Persistent and LTIM ahead of TCS as it sees relatively low risk and greater upside.

Top midcap stock picks

Persistent Systems and LTIMindtree are the brokerage's top picks in the midcap IT services segment.

The brokerage has an ‘outperform’ call on both of these stocks. For Persistent Systems, the brokerage expects multi-bagger returns. It has a target of ₹8,330 for the stock, implying an upside of 105 percent. It sees broad-based growth drivers that have helped deliver superior growth despite a drag from the top 5 clients.

Persistent Systems is scaling up accounts by chasing larger, longer-term deals, according to Macquarie. It has also shifted to offshore execution, is improving margins and is reducing client concentration. It is Macquarie's top pick within the midcap IT space and the brokerage believes that it has the potential to be the fastest-growing firm within the sector.

On the other hand, for LTIMindtree, the brokerage has a target of ₹7,540, indicating a potential upside of 76 percent.

Interestingly, Macquarie noted that as a combined firm, LTIMindtree ranks much higher than LTI and Mindtree as individual firms. The brokerage believes LTIM deserves a re-rating given how the combined entity has much lower business risk vs the individual firms of LTI and Mindtree. It sees this as a very safe choice and with broader exposure to verticals and the benefit of scale vs Persistent Systems.

The firm adds that as a combined entity, its top client concentration has reduced and the company has sufficient scale across major industry verticals to compete with larger peers. The brokerage further said that LTIMindtree offers the best prospects for long-term share-price outperformance with the least risk in its peer group.

Macquarie's third preference is Coforge, for which it has a target of ₹6,260 (upside 60 percent). Macquarie expects a sustainable growth trend for Coforge, due to its timely investments. It is poised to gain scale in the banking vertical after tapping into the US retail bank sector through its recent acquisition.

"We do not see Coforge’s high reliance on BFS as a risk as this is a relatively smaller vertical that has been scaled up quickly both organically and inorganically. We view the BFS contribution positively as it has diversified Coforge’s vertical portfolio and repositioned it for better growth. Furthermore, we view Coforge’s exposure to mid-size US banks, which is one of the fastest growing market segments for India IT Services, as a key positive," explained the brokerage.

Its fourth preference in the midcap IT space is Birlasoft, which is a sub-US$1bn market-cap firm that it thinks could surprise with a growth turnaround. Birlasoft has demonstrated effective capital allocation by returning excess cash to shareholders through recent buybacks and by a series of dividends since listing. Macquarie sees Birlasoft as a company with the ability to scale up giving its strong outsourcing value proportion and delivery credentials with a large deal. The brokerage has an ‘outperform’ call on the stock with a target price of ₹500, implying a potential upside of 65 percent.

Macquarie has a target price of ₹2,720 for Mastek, implying a 55 percent potential upside. As per the brokerage, the firm has been doing transformational M&A starting with Evosys. The brokerage stated that it is showing signs of being able to enter large accounts and also expects it to be able to cross-sell other services. However, within the sub-$1 billion market capitalisation, Macquarie prefers Birlasoft over Mastek.

Among other midcap IT stocks, the brokerage also has an ‘outperform’ call on L&T Tech with a target of ₹4,630, an upside of 20 percent. It, however, has a ‘neutral’ call on Mphasis with a target of ₹1,880, implying a downside of 6 percent.

IT sector outlook

Overall for the IT industry, the brokerage feels that digital transformation is likely to be a multi-year growth driver.

"While consensus worries about growth rates halving, we think Covid-19 ushered in a new regime in which IT spending will be more resilient. We also think the demand for Digital Transformation has a long growth runway. Digital Transformation programs rely on an approach in which a minimum viable product is created in weeks and then improved iteratively with new features added. These programs are deployed almost daily or weekly, reducing the risk of catastrophic failure, making clients amenable to experimenting with new vendors," it explained.

Macquarie also believes that with server spending still strong, worries about large cuts to IT services are overdone. The currently widely anticipated US recession is unlike the GFC or the 2001-02 recessions that arrived with little warning, noted the brokerage.

The brokerage expects good managements with strong balance sheets to continue spending and using this opportunity to pull further ahead of digital laggards in their respective industries. The Indian IT services firms have exposure mostly to the Fortune 500 (with strong balance sheets) and it sees these customers continuing to grow spending on IT services.

Its top IT sector pick remains HCL Tech as the firm is poised for a significant rerating.

Its largecap pecking order remains “HCLT > TCS > INFOSYS > WIPRO > TECH MAHINDRA”.

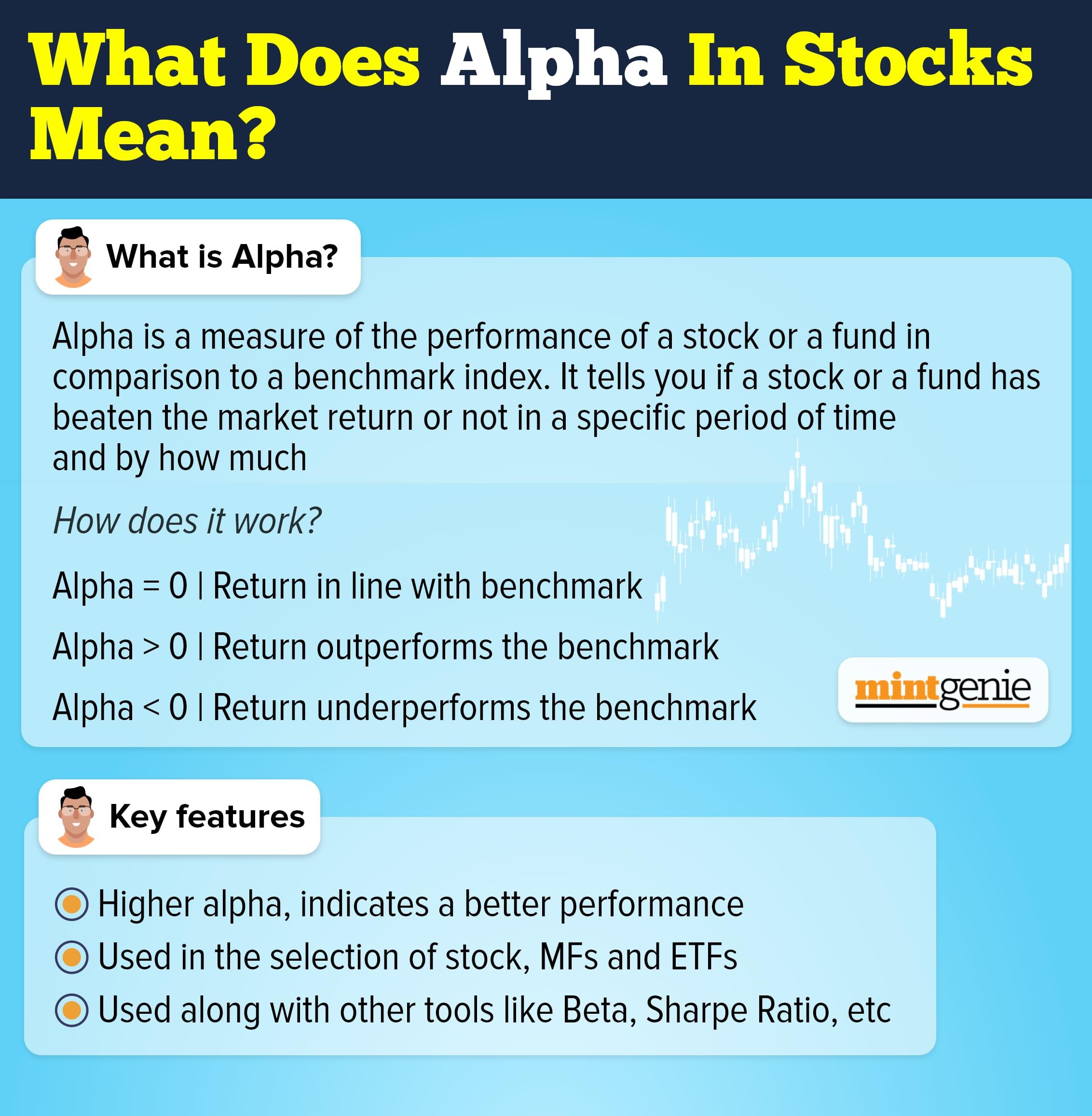

What is alpha in stocks

First Published: 20 Jan 2023, 03:35 PM IST

Related Stories

Explain Like I am 5

personal finance

Had a bitter stock market experience? Here's why you should consider having an investment advisor

Abeer Raypersonal finance

Your Questions Answered: Are there any hidden conditions in a ₹1 crore term plan with return of premium?

International Money Matters