Monthly or quarterly equity allocation adjustments are not the best approach to invest, says Dr Mohit Batra, Founder & CEO, MarketsMojo. In an interview with MintGenie, he noted that this could imply attempting to time the market, which is a poor strategy. He believes that investing in the equity market requires a 3-5-year time horizon because stock market investing is all about long term. He sees Nifty at 19,200 by March 2023.

Edited Excerpts:

With 2022 coming to an end, what lessons did you take from the year?

The stock market can be frustrating and has been particularly challenging for equity investors in 2022. The year began with high inflation, was followed by the Russian-Ukrainian war, and was further aggravated by the increase in global interest rates. All these have had a substantial impact on the global economy.

Many investors entered the stock market for the first time during the Covid months, expecting to make substantial gains year after year. However, the 2021 crash and current market volatility dashed their hopes as they expected the stock market to provide them with quick returns.

There will be years with substantial returns and years with moderate returns when investing in the stock market. On the other hand, you may occasionally experience negative returns. If you lack discipline and a plan, market volatility may cause you to become disillusioned and incur massive losses. This is a crucial lesson that investors must learn. In conclusion, the equity market is dominated by nonlinear returns, calling for restraint and planning.

What will be your investment mantra for the upcoming year?

Our mantra has remained consistent year after year. We adhere to specific philosophies as outlined below.

1. Look for companies that are focused on India. A company that focuses on India will likely fare much better in an uncertain global market than one that focuses on and serves outside the country.

2. Look for companies that are future-ready or India-ready, as the world is changing rapidly. Technology, innovations, and other such developments are occurring much faster than anyone could have predicted. Consequently, many companies that believed they had a moat are no longer in business. This is because technology has been the main disruptor in breaking through the moat. For the coming year, we will seek companies that are future-focused and are looking to invest in future products, while being future-ready. We are also looking for companies that are open to change, such as those that discuss new technology, innovations, and ESG.

What is also important to remember is the need to refine one's investment strategy. Based on market conditions, it is vital that investors give greater prominence to certain parameters and less to others based on prevailing conditions.

Where do you see Nifty by March 2023?

Examining the data over a longer period reveals that the market typically yields returns in the teens. So, based on our research and algorithms, the Nifty could reach 19,200 by March 2023.

Is it a good time to allocate more to equities? Or should you look at debt products as interest rates are likely to head north?

While some fund managers advocate for monthly or quarterly equity allocation adjustments, we believe this is not the best approach. This could imply attempting to time the market, which is a poor strategy.

We believe that investing in the equity market requires a 3-5-year time horizon because stock market investing is all about the long term. Perhaps an investor could assert that they have sufficient knowledge to exit debt instruments and invest in equity at the appropriate time. However, achieving that feat is extremely rare. As a result, we do not recommend it to investors.

In India, the equity rate cycle is nearing its peak, and interest rates will start declining somewhere in 2023. Given the stock market's potential to generate significantly higher returns than debt over the medium to long term, you may want to keep three to five years' worth of annual expenses in a debt instrument as emergency funds.

For example, if you need money right away but the market is bearish, you may be forced to exit on the wrong side. As a result, we recommend investing in the stock market over a three to five-year horizon, with the remainder in debt instruments. And that money should be invested regardless of the interest rate in the market. Hence allocation to debt is not a function of interest rate.

Is geopolitics a bigger worry for markets than rate hikes?

In the history of global markets, there has never been a year without geopolitical tension. This suggests that the market has adapted to geopolitical circumstances and could be temporarily impacted at various times.

Global concerns will always exist. So, if you observe the market becoming anxious due to geopolitics, it will only be for a brief duration. Rather, we believe the rate hike could be a greater concern than geopolitics for the equity market.

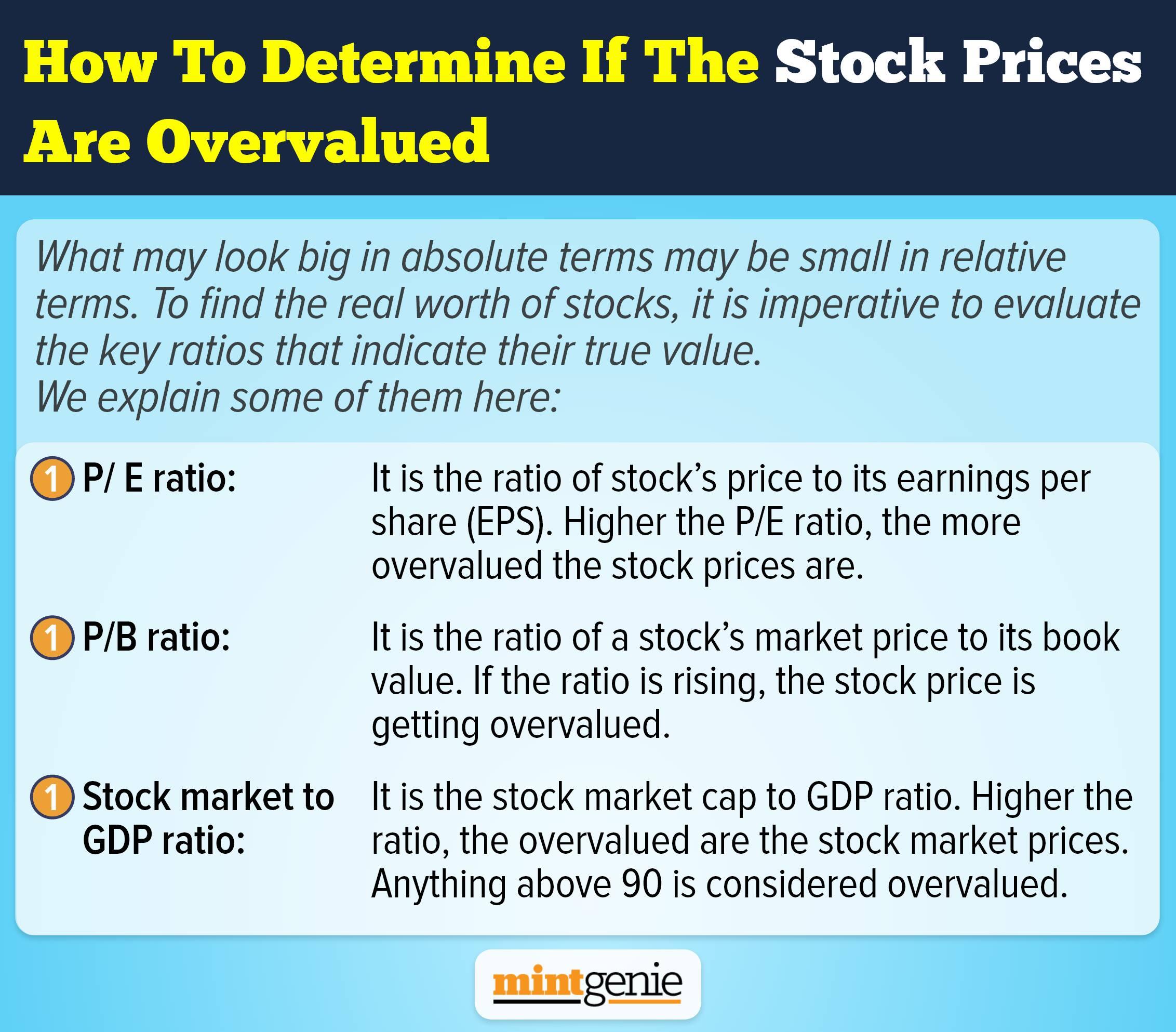

India has been outperforming global peers, is India overvalued?

MSCI Emerging Markets returned 1 percent in USD terms, while MSCI India returned 8 percent (USD). That means India has grown eight times faster than other emerging markets.

We do not think India is overvalued. A high-growth company commands a high valuation in the same way that a fast-growing economy always commands a higher valuation than the global average. Another encouraging sign is that India's return on equity (ROE) has begun to rise. According to empirical evidence, as ROE rises, so does valuation. Hence, we disagree that the Indian equity market is overvalued. Rather, it is undervalued, with plenty of room for a re-rating.

Even though we are at an all-time high in November, FIIs continue to pour money into the market. This suggests that even foreign institutional investors do not believe the Indian market is overvalued.

Midcap IT firms performed better than large-cap IT in Q2. Do you see this trend continuing?

A year ago, we were not particularly optimistic about the IT industry. Since the September results were announced, our perspective on the IT sector has shifted. We are now optimistic about the IT industry since we believe supply-side issues have been resolved, thanks to the ability of Indian IT companies to demand or renegotiate customer prices.

Despite the economic slowdown in Europe and the US, we have seen little to no impact on the financial performance of Indian IT firms. In addition, if you pay attention to the commentary provided by Indian software companies, you will notice that they do not foresee a dire future. Therefore, when and if the global economy enters a period of sluggishness, there will be a greater need for them to adopt technology to reduce costs and improve processes.

Indian IT software companies have substantial room for growth. Therefore, we believe a re-rating of the Indian IT sector is imminent. We do not analyse industries within market caps at MarketsMojo; instead, we compare one company to another. Hence, we believe it is important to be stock-specific as certain IT companies may perform poorly. But overall, we are bullish on the IT industry.

Do you see FII inflows turning positive in 2023? What factors will affect that?

India is a bright spot in the global scenario of gloom and doom. As a result, a global fund manager seeking alpha on funds has little choice but to enter India. This is why we are seeing significant FII inflows. So, while FIIs have been net sellers from FY 2021-222 and FY 2023, we believe net selling has ended.

Given India’s considerable potential for re-rating, there has been a significant inflow of funds from FIIs. Because of the Indian economy's stability, growth, policy reforms, and China plus one policy, FIIs will return. Moreover, India Inc. has demonstrated remarkable resilience despite global unpredictability.

Despite global challenges, India Inc.'s net profit has more than doubled from the pre-Covid year to the present. Furthermore, in the first half of the fiscal year 2023, India Inc.'s net profit increased by 10 percent, demonstrating their perseverance. We, therefore, believe that FIIs will return.

Value stocks vs growth stocks: which do you prefer?

MSCI Growth Index has outperformed MSCI Value Index over the last five and ten years. But that’s not the case in India, as MSCI Value Index outperformed the MSCI Growth Index.

We assess a company's potential based on its capital appreciation. For instance, many developing businesses might not provide capital appreciation such as some of the recently listed IPOs. Although they are mostly growth companies, we have observed some companies collapse after going public.

Therefore, we evaluate each company to see if its current situation enables wealth creation irrespective of whether it is growth or value. What is our investment mantra, then, to return to the earlier question? Our selection criteria do not consider where a company stands in terms of growth or value. Our criteria are distinct.

We assess whether businesses are:

• Focused on India.

• Accepting Change.

• Making themselves Future-Ready.

Key themes to keep in mind for 2023?

Due to significant corrections in the market and their availability at favourable prices, we think the IT sector could thrive.

Another crucial sector to pay attention to in 2023 is infrastructure. In order to highlight completed projects, the government typically invests a sizable sum of money in infrastructure right before an election. As a result, the substantial investment would be made in infrastructure to help some capital goods companies.

Additionally, we think that this would be the last complete budget before the elections. In light of this, the government might provide some income tax breaks. If that happens, more money will be in the hands of the taxpayers, which could encourage an increase in consumption. FMCG and consumer durables should perform very well as a result.

Auto ancillaries are yet another promising trend that could succeed in 2023 as India could become a major hub for sourcing for international automakers.