_1641277474905_1676887438098_1676887438098.jpg&w=3840&q=75)

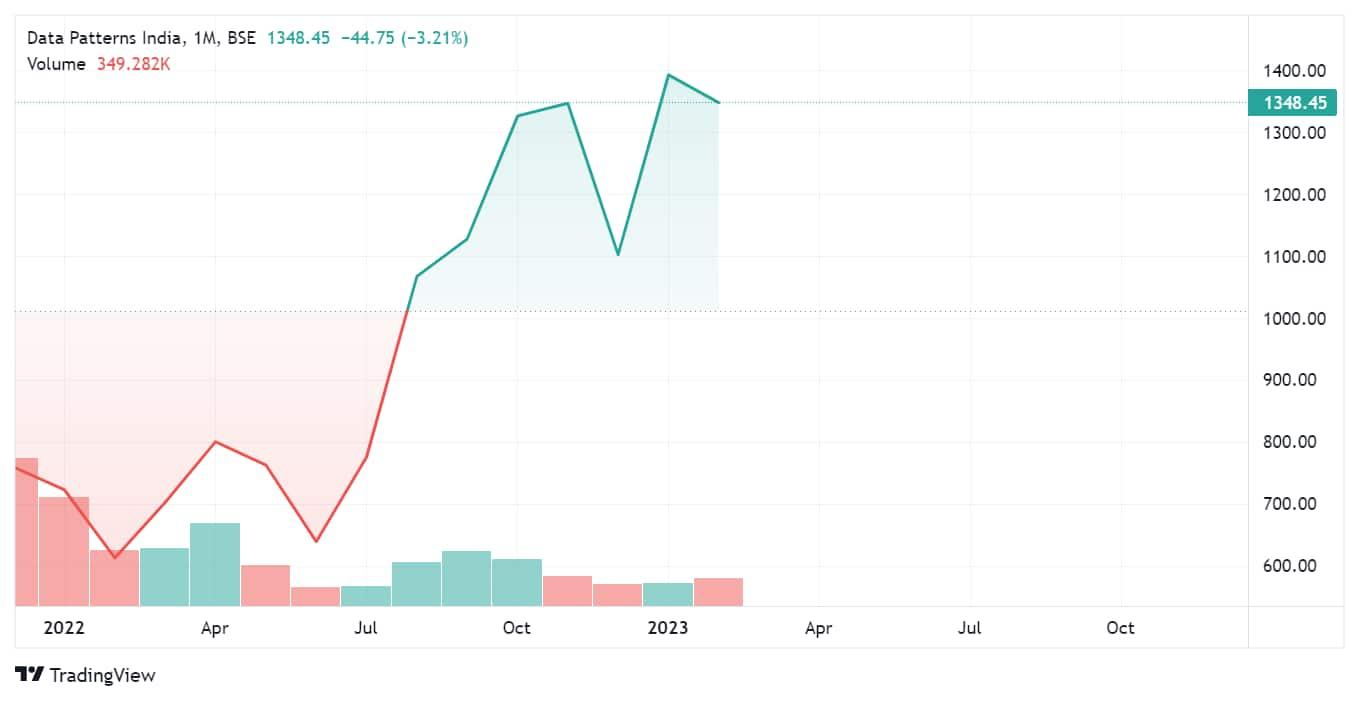

Listed in December 2021, defence stock Data Patterns India has given robust returns to its investors. Its stock has surged 121 percent in the last 1 year to ₹1,436 and 145 percent from its IPO price of ₹858.

The stock had also listed at a sharp premium of 47 percent at ₹864 per share last year.

If an investor had invested ₹15,000 in its IPO in 2021, it would have turned to ₹36,750 currently.

The stock has lost 3.5 percent in Feb so far after a 27 percent jump in January.

Data Patterns is a provider of vertically integrated defense and aerospace electronics solutions to the domestically produced defense goods market.

The company reported an exceptional performance in the December quarter, wherein the revenue and profit after tax (PAT) more than doubled. As of date, it has healthy orders of ₹890.40 crore, the firm said.

The firm reported a three times or 271.88 percent rise in profit to ₹33.32 crore in Q3 against a profit of ₹8.96 crore in the corresponding quarter last year. Its sales also zoomed 155 percent to ₹111.81 crore against ₹43.84 crore in the year-ago period.

On account of better execution, gross margins rose 140 bps QoQ and EBITDA margins for Q2FY23 climbed 42.2 percent as against 34.2 percent in Q2FY23 and 35.7 percent in Q3FY22.

With the expectation of new orders in the January-March quarter (Q4), the management said the company is focused on improving execution effectiveness to promote operating leverage and maintaining a diversified order book.

"With the new manufacturing facility anticipated to commence in Q4FY23, we are well positioned to benefit from the strong sectoral tailwinds given our R&D prowess and our manufacturing capabilities," the management announced.

After the strong earnings as well as stock performance, brokerage house JM Financial has recommended a buy call on the stock with a target price of ₹1,500. Data Patterns reported a strong beat on estimates, led by higher-than-expected revenue in both production and development contracts, it said.

The brokerage increased its EPS estimates by 6/9 percent for FY23/24, but maintain FY25 estimates, due to better order inflows and execution visibility in FY23.

"We bake in sales and EPS CAGR of 31 percent and 28 percent respectively over FY22-25E, as increasing share of development orders (56 percent of order book) will drive future growth," it said.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.