Food delivery major Zomato has bounced back strongly in the current year after a weak show last year in 2022. The stock has exhibited a remarkable recovery in 2023 so far, jumping over 55 percent. The stock lost 57 percent of its investor wealth in 2022.

Multibagger: Zomato recovers, up 105% from 52-week low; what lies ahead for the stock?

TL;DR.

Zomato's stock has seen a remarkable recovery in 2023, jumping over 55% after a weak performance in 2022. The brokerage house Ventura Securities expects the stock to rise further and recommends a ‘buy’ call with a target price of ₹156.

The stock hit its 52-week high of ₹102.85 earlier this month, surging over 35 percent from its IPO price of ₹76. After starting its downward trend in June 2022, the stock re-hit its IPO price a year later in June this year.

Currently trading at around ₹91, the stock has given multibagger returns, rallying over 105 percent, from its 52-week low of ₹44.35, hit in January this year. Meanwhile, in the last one year as well, the stock has advanced 47 percent.

Brokerage house Ventura Securities expects the stock to rise further going ahead. It recommends a ‘buy’ call on the stock with a target price of ₹156, indicating an upside of over 71 percent in 24 months. The brokerage said that it is 'long-term constructive' on the fortunes of Zomato.

"The industry structure is likely to remain a duopoly of Zomato and Swiggy with limited disruptions from the likes of Amazon and weaker offering propositions from direct ordering companies like DotPe Thrive and ONDC, etc. due to limited networks in Indian cities. Coupled with the moats of network effects, branding, last-mile delivery, customer user behaviour (convenience and addiction) and wide geographical reach, we believe that the duopoly is likely to dominate in the visible future. Zomato's strategic acquisition of Blinkit has proven to be a judicious one, delivering revenue results, and we anticipate it will also positively impact EBITDA," explained the brokerage.

Zomato stock price trend

Earnings

In the June quarter (Q1FY24), the food aggregator reported its first-ever consolidated net profit of ₹2 crore as against a net loss of ₹186 crore in the year-ago period. The revenue from operations during the quarter came in at ₹2,416 crore versus ₹1,414 crore in the year-ago period.

The company said its food delivery business posted adjusted revenue of ₹1,742 crore in the first quarter as compared to ₹1,470 crore in the year-ago period. The gross order value (GOV) for the food delivery business showed strong growth, rising by 11.4 percent QoQ to reach ₹7,318 crore in Q1, compared to ₹6,569 crore in the preceding March quarter. Furthermore, Blinkit, the grocery delivery service, also performed well, with revenue reaching ₹384 crore in Q1, a significant increase from ₹164 crore in the year-ago quarter. The GOV for Blinkit grew by 5 percent QoQ, reaching ₹2,140 crore.

Overall, the company's EBITDA loss narrowed sharply to ₹48 crore in Q1 from ₹307 crore in the year-ago quarter.

Commenting on the Q1 performance, Zomato Chief Financial Officer Akshant Goyal said, "Realistically speaking, we were expecting to hit this milestone in the September quarter, and we were being conservative in our earlier guidance. However, some critical parts of the team across our businesses out-executed our expectations/plans, and some of our initiatives delivered better outcomes than we had expected."

"We expect our business to remain profitable going forward, and knowing what we know today, we believe we will continue to deliver 40 percent-plus YoY topline (adjusted revenue) growth for at least the next couple of years," Akshant said.

The brokerage also lists the advantages to Zomato from the Blinkit acquisition:

A ready infrastructure and systems in place: Blinkit has built key infrastructures such as a robust technology platform, strong third-party tie-ups, a dark-storage network, and a business that has achieved credible scale. Instead of building the same systems and infrastructures, which would have been an additional drain on the capital, ZOMATO acquired Blinkit and the combination of both quick commerce and food delivery is expected to form better synergies.

A natural extension to the food delivery business: Quick commerce space forms a natural extension to ZOMATO’s food delivery business as both segments operate on a hyperlocal model. It has been the priority for ZOMATO since 2021 to increase the share of the wallet of its online food delivery customers. Blinkit could be a ready launchpad for ZOMATO for the expansion in quick service commerce.

Better utilisation of existing assets (delivery fleet): Acquiring a grocery delivery business will increase the range of operations of ZOMATO. Food delivery is peaks at only once a week, whereas grocery delivery has a higher frequency in a week. Thus, asset (fleet) utilisation is better, and this improves overall profitability.

Higher order frequency and larger addressable market: With the ’10-15-minute delivery’ model in place, the customers’ ordering frequency has improved significantly and they are motivated to shop spontaneously. Therefore, ZOMATO’s addressable market is expected to witness a healthy expansion through the addition of Blinkit’s quick-commerce.

Faster growth in GOV: Blinkit’s AOV is 50 percent higher than ZOMATO’s AOV and the monthly ordering frequency per MTU for both companies are same at 3.5X. ZOMATO can use its existing MTU base to improve Blinkit’s MTUs, which will translate into faster growth in Blinkit’s GOV. Both companies are expected to benefit from each other’s customer base.

Bull and Bear Case Scenarios

The brokerage has also prepared likely Bull and Bear case scenarios for FY26 price, based on revenue growth and Price to Sales multiple.

Bull Case: In this scenario, Ventura has assumed revenue of ₹22,000 crore (CAGR growth of 46 percent) and EBITDA margins of 8.4 percent at Price to Sales ratio of 8x which will result in a Bull Case consolidated price target of ₹205 (an upside of 118 percent from CMP).

Bear Case: In this scenario, the brokerage has assumed revenue of ₹18,000 crore (CAGR growth of 36.5 percent) and EBITDA margins of 7 percent at Price to Sales of 4X, which will result in a Bear Case consolidated price target of ₹84 (a downside of 10.6 percent from CMP).

Key Risks & Concerns

- The company has sacrificed operating profitability to achieve faster growth and has been reporting losses. To cover these losses, the management raised capital several times and diluted its equity. But these efforts do not guarantee future revenue growth and profitability, said the brokerage.

- Zomato's business model is app-based and it doesn't require any major capex on fixed assets and distribution network. In terms of consumption growth, India is next to China, and it could attract global food delivery players who have deep pockets which can help them sustain over the longer term and play price wars with Zomato, it added.

Estimates

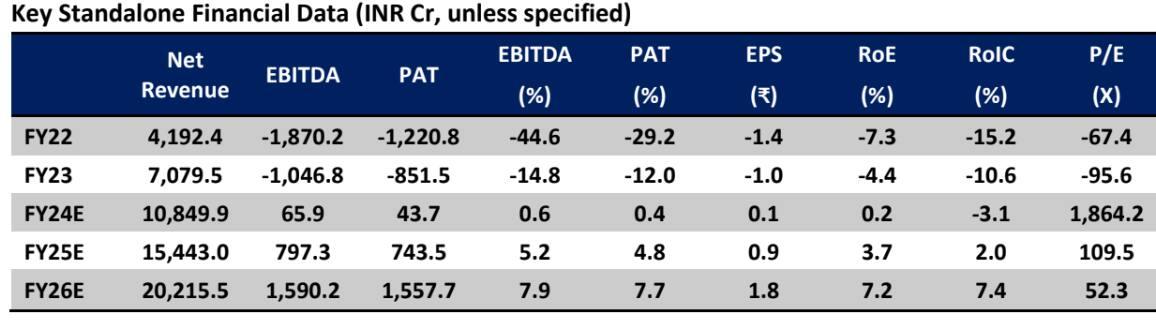

Over the period FY23-26, Ventura expects Zomato’s revenue to grow at a CAGR of 41.9 percent to ₹20,215.5 crore, driven by 31.7 percent CAGR growth in food delivery revenue to ₹10,632 crore, Hyperpure CAGR of 62.4 percent to ₹6445.9 crore, dine-out & subscription CAGR of 13.3 percent to ₹340 crore and Blinkit’s revenue CAGR of 51.4 percent to ₹2,797 crore.

Consolidated EBITDA/PAT is expected to turn around in FY24 at ₹65.9 crore/43.7 crore. Further EBITDA/PAT is expected to grow at a 2-year CAGR of 391.2 percent/497 percent to ₹1,590/1,557 crore.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

25 analysts polled by MintGenie on average have a 'Buy' call on the stock.

Source: Ventura

First Published: 28 Aug 2023, 02:00 PM IST

Related Stories

personal finance

What are the different types of valuation ratios and how to use them efffectively?

Kirti Jhamarkets

Zomato spikes over 13.5% to a 17-month high after company turns profitable in Q1

A Ksheerasagar