At first glance, it appears that the PSU banking stocks have started losing their mojo as most of them have suffered losses in double digits in the last one-and-a-half month.

With a gain of almost 71 percent, the Nifty PSU Bank index stole the limelight in 2022 when the return of the benchmark Nifty50 was just 4 percent.

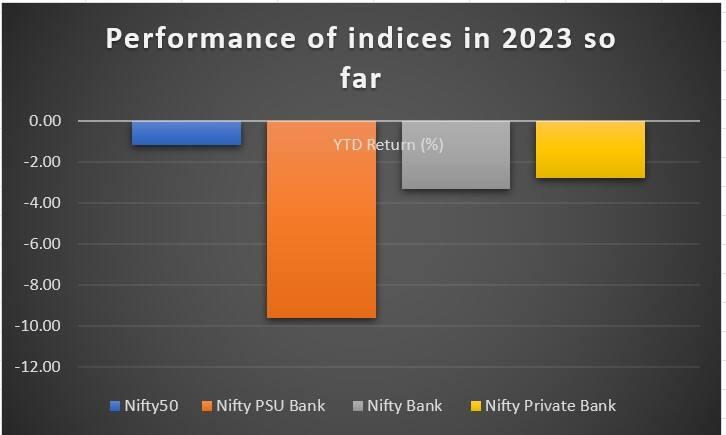

But now the situation appears to be changing. Data show that the Nifty PSU Bank index is down nearly 10 percent in the calendar year 2023 so far, against a 3 percent loss in the Nifty Bank and Nifty Private Bank indices. Benchmark Nifty50 is down over a percent for the same period.

Barring shares of Indian Bank, which is up about 0.6 percent this year, all stocks of the Nifty PSU Bank index are in the red, with shares of Punjab and Sind Bank, Indian Overseas Bank, Central Bank of India, UCO Bank, Canara Bank and SBI down between 10-17 percent.

Why are PSU bank stocks falling?

While many analysts agree that the outlook for the PSU banking stocks is still positive for the medium to long term, two factors are playing against them at present.

One, after strong outperformance, some profit-booking was expected as the market sentiment remains weak due to uncertainty over the rate hikes and economic growth. Foreign portfolio investors (FPIs) have been strongly selling in the financial sector.

The second factor is the Adani-Hindenburg saga which has raised concerns that the PSU banks have significant exposure to the Adani Group which could turn out to be a matter of worry for the lenders, going ahead.

"The overall underperformance in PSU Bank is attributable mainly towards the Adani group-Hindenburg saga," said Rahul Malani, Deputy VP of Research at Sharekhan by BNP Paribas.

“The Street is fearing the worst-case scenario as per as Adani conglomerate’s debt exposure is concerned, which is not the ideal case as most of the banks' debt exposure to the Adani Group was secured by completed and cash-generating assets,” said Malani.

He expects volatility to continue in the PSU bank stocks in the near term, till some more clarity emerges and the situation normalises.

Anand James, Chief Market Strategist at Geojit Financial Services also highlighted that the broad market selloff and the fears of fallout from the Adani saga had kept the banking sector under pressure, especially the PSU banks.

He also added that FPIs have been strong sellers in financials. "They sold ₹6,701 crore worth of shares in the first half of January and ₹8,503 crore worth of shares in the second half, both being the largest sectoral outflows during these periods," said James.

However, the concern may be exaggerated. Many rating agencies and brokerage firms, including CLSA and Jefferies, do not see a material risk to Indian banks due to their exposure to the Adani Group debt which has doubled in the last three years.

Even though CLSA said that PSU banks do have material exposure (30 percent of group debt) to Adani Group, it added that this debt has not increased in the past three years. Most of the incremental funding to the group for new businesses and acquisitions has come via overseas sources.

Jefferies also said that Indian banks' exposure to the Adani Group is manageable and the group's debt accounts for 0.5 percent of total loans across the Indian banking sector.

Should investors buy, sell or hold PSU bank stocks?

Analysts do not see a material impact on PSU banks' health due to their exposure to the Adani Group.

As Malani explained, the banks have proactively disclosed their total exposure towards Adani Group in terms of fund-based, non-fund based and investment books.

"Currently, banks do not envisage any challenge in their ability to service obligations and have guided that their exposure is towards projects that have tangible assets and strong cash flows. On the positive side, these PSU banks do not have exposure towards loans against shares (LAS) of the group companies," said Malani.

He is of the view that investors should build staggered positions in PSU banks as the current valuation offers some margin of safety.

"We believe investors should use this volatility to build staggered positions in PSU banks as the margin of safety is emerging gradually at current valuations. We remain positive on the PSU banks as these banks do not have exposure towards LAS and have funded those projects which have strong tangible assets backed by strong cash flows with proper escrow mechanisms," said Malani.

The December quarter numbers of PSU banks have come stronger and the outlook has improved.

As per brokerage firm Motilal Oswal Financial Services, the earnings outlook for PSU banks has improved, led by a broad-based improvement across all parameters: margin, operating profitability, and credit cost.

"Capital ratios remained healthy to pursue growth opportunities. We saw a revival in growth as PSU banks reported strong sequential growth, particularly in the Corporate segment. We expect trends to remain healthy going forward as the pipeline remains strong across most banks," said Motilal Oswal.

"The SMA (special mention accounts) pool remains benign, which, coupled with limited slippages from the restructuring and ECLGS (emergency credit line guarantee scheme) book, augurs well for incremental slippages to remain controlled and will aid in a sustained reduction in credit cost. The margin outlook remains positive as MCLR re-pricing will likely offset the rising cost of deposits as competition to garner deposits intensifies further," Motilal Oswal said.

However, a higher valuation of PSU banking stocks remains a concern.

As per Motilal Oswal, PSU banks are trading at a P/B (price-to-book) ratio of 1 time, at a 24 percent premium to its historical average of 0.8 times.

So, risk-averse investors may wait for some more time to buy PSU banking stocks.

"Books have improved, with results either surprising or in line with expectations. However, a higher valuation has attracted selling, and it might require broad market sentiments to improve in order to fetch higher multiples; hence, it would be better to stay patient," said James.

Disclaimer: The views and recommendations given in this article are those of individual analysts and brokerage firms. These do not represent the views of MintGenie.