The third quarter earnings for the financial year 2022-23 (Q3FY23) are likely to be soft with slight margin improvement. While global growth concerns will continue to weigh on the performance, moderation in commodity prices is likely to help improve margins in Q3.

"We expect the Q3FY23 earnings season is likely to be a mixed bag. While the season will be led by sequential margin expansion driven by moderation in commodity prices and an uptick in credit growth, the export-oriented themes are likely to be laggards. We believe the broad-based earnings momentum which remained robust for multiple quarters is likely to take a brief pause in Q3FY23," said Axis Securities in an earnings preview note.

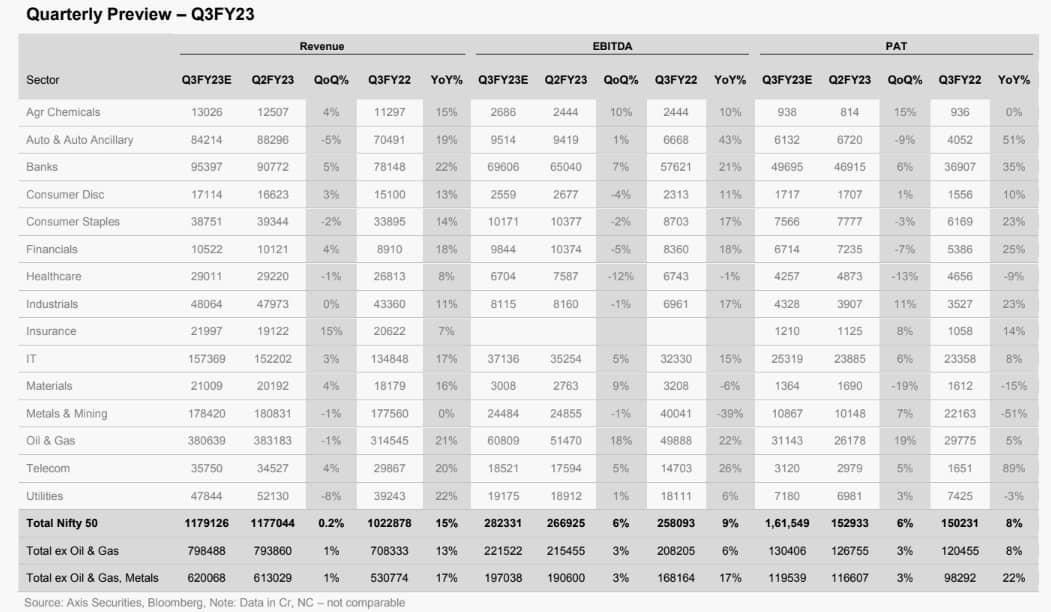

Corporate earnings growth this quarter would be led by BFSI, Auto and Technology. However, the aggregate performance of Nifty universe will be marred by a sharp drag from global commodities such as Metals and O&G, which are likely to report a YoY earnings decline. However, the recent commodity price correction will drive sequential margin expansion in Q4FY23E and FY24E.

Axis forecasts Nifty's profit to grow 8 percent in the third quarter. Meanwhile, Nifty's EBITDA and revenue are likely to rise 15 percent and 9 percent, respectively, in Q3, forecasted Axis. Furthermore, excluding Oil & Gas and Metals, Nifty's revenue/EBITDA/PAT are expected to grow by 17 percent/17 percent/22 percent, respectively, over the same period, it predicted.

"The Indian economy exhibited remarkable resilience in Q3FY23 and the RBI governor also highlighted a visible uptick in most of the high-frequency indicators over the last quarter. High-frequency indicators such as GST collection, power consumption, and E-way bills are pointing upwards on a sequential basis, indicating robust demand even after the festival season. GST collection stood at 1.48 lakh crore for Dec’22, which stood above pre-pandemic levels and remained above the 1 lakh crore mark for sixteen consecutive months – an impressive sign in terms of government tax collection and overall fiscal situation," noted the brokerage.

Keeping this in perspective, Axis believes the majority of the companies will likely report revenue growth in line with expectations, however, some pressure is likely to be visible on commodity producers and the export-oriented sectors.

In Q3FY23, Axis expects strong earnings growth for Automobiles, Banks, and Industrials while expecting earning contraction in the Metals, Cement, and Healthcare sectors on a YoY basis. Currently, it foresees FY23/24 Nifty EPS at 817/930 with a growth of 11 percent/14 percent, respectively, and will revise its numbers post the earnings season. It sees FY25 Nifty EPS at 1,049, up 13 percent YoY.

Another brokerage Motilal Oswal, however, has reduced its FY23E Nifty EPS by 2 percent to ₹820 (earlier: ₹837) largely led by a cut in O&G’s earnings estimates. It now expects the Nifty EPS to grow 13 percent/21 percent in FY23/FY24, respectively. Financials alone are likely to account for 70 percent of the incremental FY23E earnings growth for Nifty, it said. MOSL estimates Nifty FY25 EPS to be at ₹1,135 (+15 percent YoY).

Key Highlights for Q3FY23

Stable asset quality trend for the BFSI sector; earnings on track: As per Axis, the banking sector will continue to deliver robust numbers driven by the sequential improvement in the credit growth for the retail and SME segments. Moreover, the improvement in the asset quality trend is likely to continue for the quarter, which is likely to bring further confidence in the space, it said. It believes the BFSI sector continues to stand out in the current volatile environment and is likely to post encouraging numbers in the quarterly earnings with strong credit growth, stable NIM, and the benefit of loan re-pricing to aid margins.

Margin expansion for auto OEMs: The Indian automobile sector has seen a significant demand improvement with most categories witnessing encouraging traction on a YoY basis led by a weaker base, said Axis. However, on a QoQ basis, the sector may witness some contraction due to the seasonality factor, it said. Demand momentum in the CV segment is likely to sustain and Axis expects the CV cycle to maintain its momentum driven by the pickup in economic activities and the government’s focus on infrastructure and the opening of educational institutes. The margins are likely to improve sequentially as commodity prices are cooling off and volumes are improving, it added.

Rural demand key in the consumer sector: Consumer companies are expected to report a decent set of numbers, led by calibrated price hikes undertaken by companies to combat inflation, noted the brokerage. Management commentaries on the raw material trends and rural vs. urban demand remain the key monitorables during the quarter, it highlighted.

Cost pressure to ease in the cement sector: Sharp demand revival was seen during Nov/Dec’22. Axis believes the cement demand is likely to remain positive, led by the pick-up in the government projects related to infra and housing. Realization across the sector is likely to improve marginally while EBITDA/tonne is to improve on a sequential basis owing to lower operating costs, stated the brokerage.

Seasonally weak quarter for IT services: The IT services sector is expected to report moderate growth in Q3FY23, primarily on account of the seasonally weak quarter and slowing down growth momentum led by uncertainties in the US and UK, the brokerage said. Margins for most companies are likely to improve by 50-70bps, largely due to the attrition levels slowing down and the rupee depreciation, it added.

Weaker realization for metals: As per the brokerage, the steel sector realization is likely to decline on a QoQ basis led by price cuts and reset of contracts during the quarter. Profitability is to improve on a sequential basis on account of the lower raw material prices while the revenue for aluminium producers is expected to decline on a QoQ basis with the fall in aluminium prices during the quarter, it noted.

TOP PICKS

Axis has listed 9 stock picks for this earnings season. They include Cipla, Dalmia Bharat, APL Apollo Tubes, Ashok Leyland, Equitas SFB, Indian Hotels, Westlife Foodworld, Camlin fine Sciences and PNC Infra.