Kickstarting the fourth quarter earnings season, Tata Consultancy Services (TCS) will announce its March quarter earnings (Q4FY23) on April 12, 2023. Q4 is likely to be a weak quarter for the IT space. As per experts, worsening macro conditions and the recent banking crisis in US and Europe indicate a slowing down of tech spending by enterprises globally.

Earnings forecast

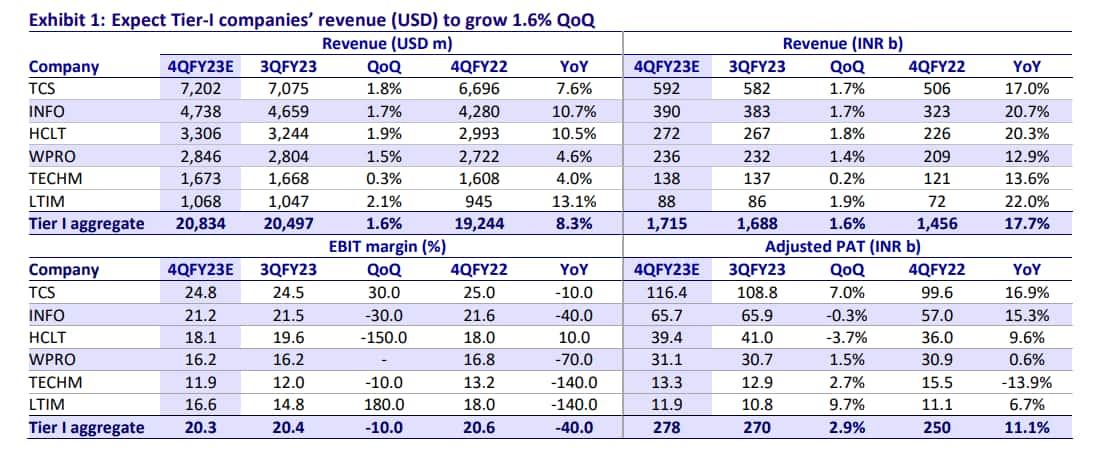

In an earnings preview report, brokerage house Motilal Oswal (MOSL), estimated dollar revenue for its IT services coverage universe to grow at 8.4 percent in the March quarter. Meanwhile, it sees EBIT and PAT (in rupee terms) to grow 15.9 percent and 11.2 percent YoY. respectively.

This implies, an FY23E dollar revenue growth of 10.6 percent while FY23E EBIT and PAT growth of 11.4 percent and 7.8 percent, respectively, noted the brokerage.

It further expects its IT services coverage universe to deliver a median revenue growth of 0.8 percent QoQ and 9.2 percent YoY in constant currency (CC) terms in Q4FY23. Major currencies have appreciated against the dollar which will provide tailwinds, it noted. EBIT and PAT are expected to grow by 1.2 percent and 3 percent QoQ, respectively, due to weak topline growth, it added.

"While the BFSI sector has been resilient for the last few quarters, recent industry developments have added to caution on its tech spending. Though the Indian IT services firms do not have meaningful exposure to the affected US regional banks, fears of a banking crisis could impact near-term IT spending by banks and will be the key monitorable during the 4Q management commentary. Apart from BFSI, Hi-Tech, Manufacturing and Retail may also report muted growth in 4Q. Clients have started to cut discretionary spends while increasing focus on cost efficiency. IT services companies are seeing a shift to cost optimization deals, along with increased vendor consolidation deals in the pipeline," it explained.

While the management indicated that the secular demand is still intact in certain verticals and service lines, it has suggested near-term caution among clients and some delays in decision-making, which might lead to project deferrals and pause in execution, the brokerage further pointed out.

Prefer Tier I over Tier II companies

The brokerage noted that with valuations correcting meaningfully over the last one year (IT services sector P/E at 21.6x, down 33 percent from the peak), it maintains a positive stance on the IT services sector, supported by a favorable medium to long-term demand outlook despite some near-term pain.

However, it also continues to prefer Tier-I (large-cap) players over their Tier-II (mid-cap) counterparts, given the former’s attractive valuations, increased traction in vendor consolidation, and diversified client portfolios.

Among Tier-I players, it likes TCS, HCL Tech, and Infosys.

According to MOSL, TCS remains best positioned to benefit from long-term structural tailwinds in tech services and should see a relative pick-up in growth, aided by clients’ focus on cost optimization and efficiencies.

Meanwhile, HCL Tech is one of the key beneficiaries of Cloud adoption at scale, given its expertise in IMS and it expects Infosys to deliver strong growth, backed by strong deal wins.

Among Tier-II players, it prefers Cyient and Zensar Tech.

A revival in the aerospace vertical with strong growth, ebbing challenges in verticals like railway, and strong growth with attractive valuations make Cyient a strong ‘buy’, it said. While on Zensar, it said a good margin recovery and the new CEO’s focus on execution (rather than strategic changes) should help it stabilize.

PAT

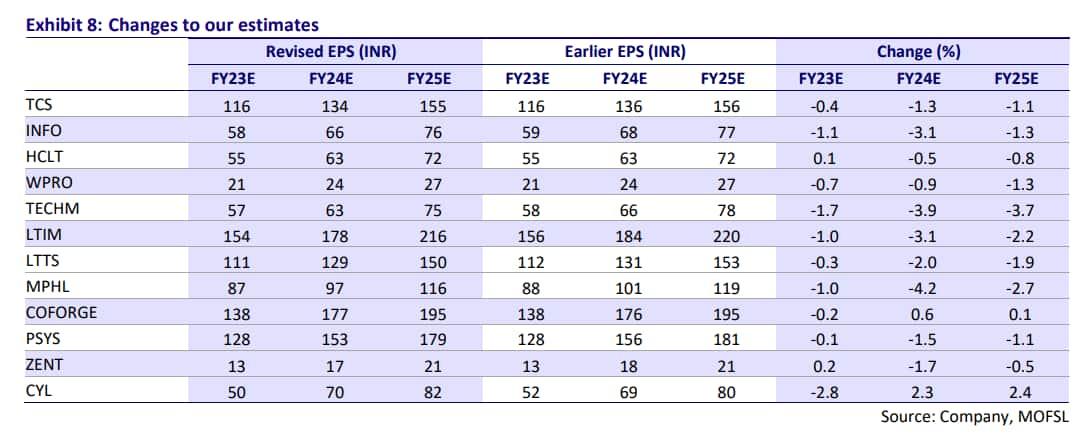

The brokerage expects its Tier-I IT coverage universe to post PAT growth of 2.9 percent QoQ and 11.1 percent YoY. LTI Mindtree is expected to report PAT growth of 9.7 percent QoQ due to a low base in Q3, whereas TCS should report a PAT growth of 7 percent, Wipro 1.5 percent, and Tech Mahindra 2.7 percent. Meanwhile, Infosys is likely to report a PAT degrowth of 0.3 percent and HCL Tech's PAT is also likely to fall by 3.7 percent.

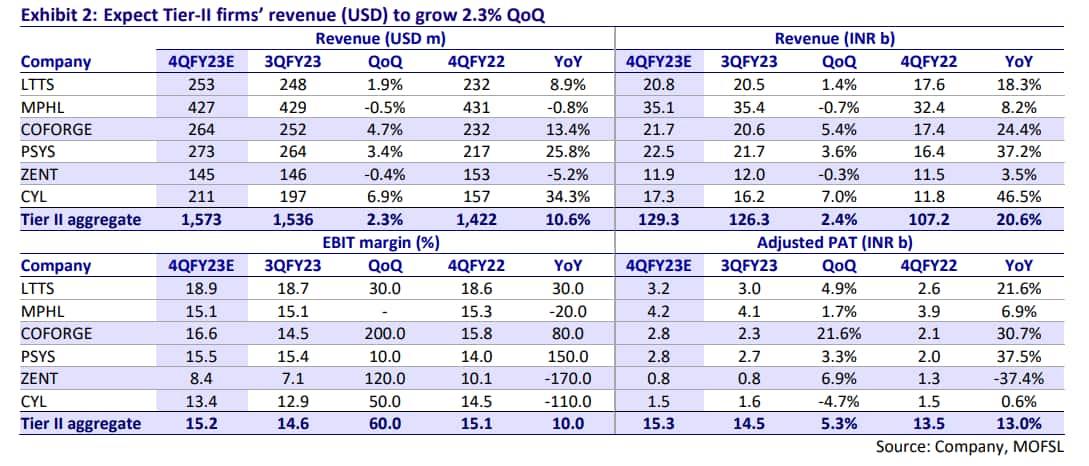

For Tier-II players, the brokerage sees PAT growth of 5.3 percent QoQ and 13 percent YoY, stronger than Tier-I firms, aided by healthy revenue growth and margin expansion.

Margins

As per the brokerage, Q4 margins will see some impact from growth moderation, especially for the Tier-I pack. However, easing supply pressure, cooling off attrition and improvements in utilization should aid margins, it added.

"Tier-I companies should post flat margins, with HCL Tech and LTIMindtree being the exceptions. The Tier-II pack will post a wider range of flat to 200 bps QoQ, led by Coforge and Zensar Tech with margin improvement of 200bps and 120bps QoQ, respectively. Considering the near-term softness in demand and elevated hiring last year, we expect net hiring to take a pause in 4Q. We also expect sub-contractor expenses to moderate, while the reduction in backfilling and retention should support margins," it said.

Topline growth

The brokerage also noted that Tier-I companies’ revenues should grow, albeit modestly, despite weak macro, with Tech Mahindra being the only exception. LTIMindtree will lead the pack with revenue growth of 1.6 percent QoQ CC, followed by TCS at 0.9 percent, it predicted.

Meanwhile, revenue growth for Infosys, HCL Tech and Wipro are likely to remain weak at around 0.5-0.6 percent each. HCL Tech is likely to report seasonal weakness in the software business but the service business will grow at around 3.6 percent QoQ, estimated MOSL.

Now, among Tier-II firms, it expects Cyient's topline to grow at 5.4 percent QoQ in CC, followed by Coforge and Persistent Systems with 3.3 percent and 3 percent QoQ CC revenue growth, respectively. However, Mphasis and Zensar could see a revenue decline of 1.1 percent and 0.8 percent QoQ in CC, it added.