QSR (quick service restaurants) space has witnessed strong correction in the last 6 months with most players giving negative returns continuously since October last year. But despite this recent correction, domestic brokerage house HDFC Securities does not believe this is a perfect 'fishing' time for this space.

QSR Stocks: Not the best time to buy, says HDFC Securities; initiates coverage with two ‘reduce’ calls

TL;DR.

HDFC Securities has initiated coverage on 3 QSR stocks, 2 with ‘reduce’ calls and one with ‘add’ and has upgraded its rating on Jubilant to 'add' from 'reduce' earlier.

"QSR, among the other consumer categories, has seen normalisation relatively late post-COVID (particularly dine-in); mobility and pent-up have boosted the growth metric over the last 15-18 months. It resulted in a sharp improvement in operating metrics (operating margin improved by 200-500 bps in 9MFY23 vs. 9MFY20). However, with the normalisation in demand, the impact of weak consumer sentiment, and raw material inflation, we believe the operating margin will see an impact in FY24 (may also not repeat in FY25 also with rising competition)," stated the brokerage. It suggests waiting before seeing the full impact of weak demand.

Amid this backdrop, HDFC Securities has initiated coverage on 3 QSR stocks, 2 with ‘reduce’ calls and one with ‘add’ and has upgraded its rating on Jubilant to 'add' from 'reduce' earlier.

The brokerage said that on a relative basis, it likes Jubilant (investing to further improve its competitiveness) and Westlife (pure play India QSR story) but would like to avoid Devyani and Sapphire due to potential slippages for the Pizza Hut story (particularly in weak demand).

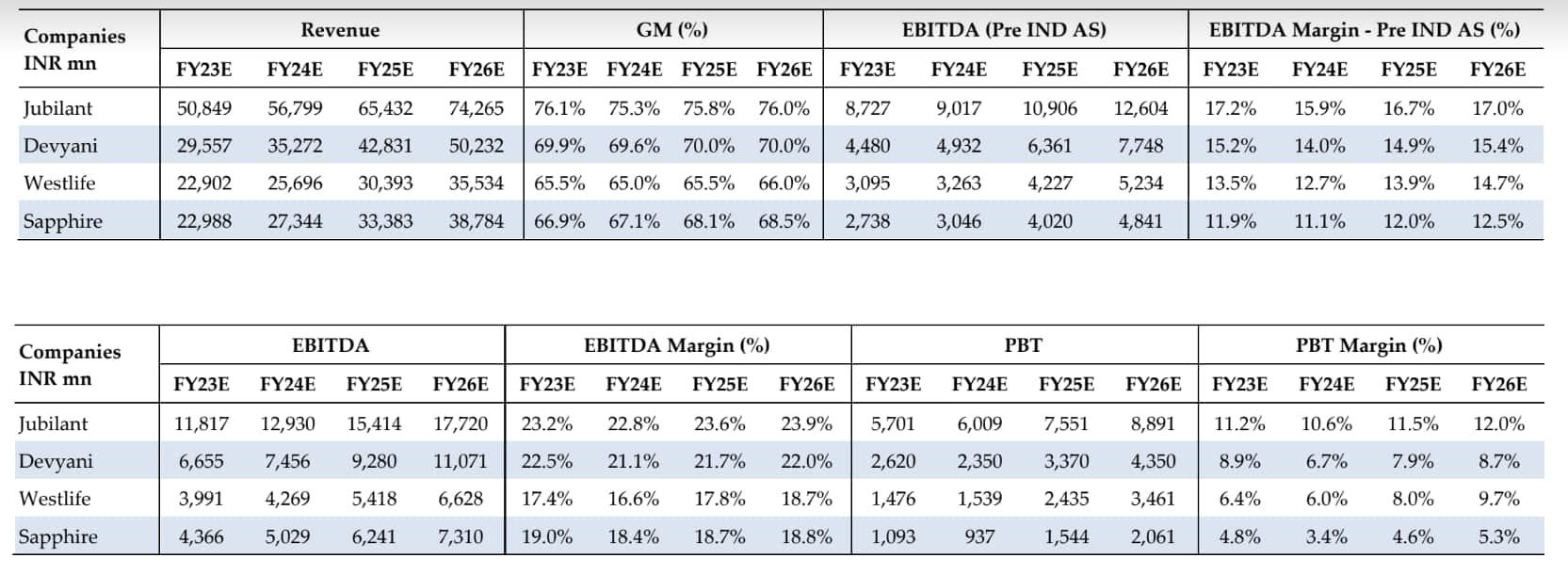

QSR Industry

The brokerage noted that the QSR industry saw a yearly addition of 125 stores in 2005-2010, which increased to 300 stores in 2010-2020 and 475 stores in 2020-2023E. It believes the yearly expansion can sustain 550 stores up to 2030E which will lead to store metrics of 6 stores per mn by 2030. Thus, most QSR players, HDFC estimated, will be able to grow their store units by over 10 percent over the next few years. It further added that the underlying SSSG (same-store sales growth) for most franchises is close to a mid-high single digit, offering overall revenue CAGR (compounded annual growth rate) in the mid-teens.

Why play QSR?

As per the brokerage, with India’s long-term growth and consumption theme, QSR is one of the best-fit stories.

"QSR provides a multi-year growth opportunity, particularly for countries like India where the population will always be in favour of such food alternatives. QSR is more of a macro story play that India’s fast-changing ecosystem (internet, mobile, young population, large population, rising hygiene preferences, etc.) will continue to support. However, the shift in consumption patterns (home/traditional food to eat-out/fast food alternatives) is quite slow in India vs. other countries (particularly in China). This is why, despite the global giants’ early entry in India (mid 90’s), the store network is still quite low. Therefore, QSR will be a multi-year growth potential market for global giants but we reckon that store expansion will be linear (8-10 percent store growth)," it said.

It further noted that QSR companies are focusing on aggressive store expansion and want to sustain the new store opening pace despite the weak consumer sentiment. HDFC Securities expects the new store additions to maintain growth ahead of their historical growth.

HDFC Securities also pointed out that the QSR sector has benefited as mobility resumed in the post-Covid period.

"Because of this one-time spur in demand, we have seen operating margins expanding sharply (even compared to pre-Covid). However, after seeing normalised growth, such categories/ companies have gone back to their normal margin range. QSR companies have also seen sharp margin improvement in 9MFY23 led by higher consumer mobility, focus on branded food and positive consumer sentiment," it stated.

HDFC Securities believes a large part of these tailwinds are now behind and raw material inflation will continue to impact gross margin but these companies are expected to see margin normalisation in FY24.

Overall long-term investment thesis

(1) QSR is more of a macro story play with India’s fast-changing ecosystem (internet, mobile, young population, large population, rising hygiene preferences, etc.) driving penetration.

(2) QSR store growth is sustainable at 10 percent with the industry expected to reach six stores per mn population by 2030 from three stores per mn currently.

(3) Long-term SSSG to sustain at mid-high single digit (most global QSRs achieved in the US in the long run).

(4) Earnings growth driven more by unit growth than margin expansion.

(5) Macro will remain favorable (sensitivity is high for QSR).

"QSR industry has multi-year growth potential and global QSR giants will be fit for the change in India’s rapid ecosystem. They have more right to win in India’s consumption metric with a rising consumer base, eating-out frequency, quicker delivery and value-for-money proposition. Thus, despite near-term challenges, we believe the long-term rich valuation will sustain QSR players," the brokerage explained.

Source: HDFC Sec

Stocks

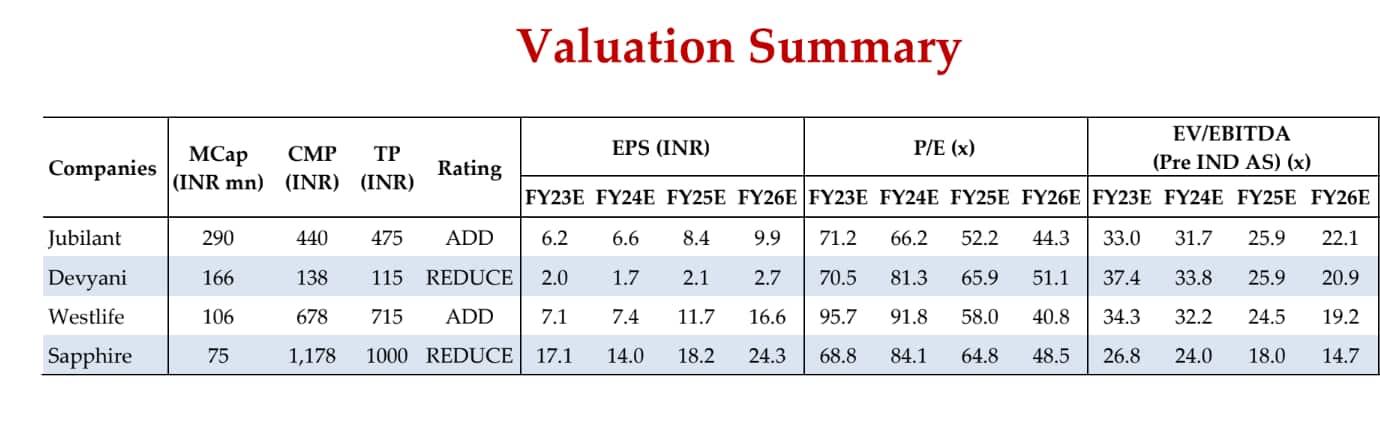

Jubilant FoodWorks: Even though the brokerage has upgraded the stock to ‘add’ from ‘reduce’, it does not see a very high upside of the stock. It has a target price of ₹475 for Jubilant, indicating an upside of 10 percent. The stock witnessed strong correction recently, giving negative returns continuously since October 2022. It has lost 5 percent in 2023 YTD but is down 20 percent since October.

"Jubilant has the best in class unit economics, consumer & store base, and delivery expertise among QSR peers. The company is stepping up its investments in dine-in along with strengthening its backend by setting up new commissaries in Bengaluru and Mumbai over the next 12-15 months. The company wants to remain aggressive in store expansion, particularly for Domino’s and Popeye’s," said the brokerage.

It estimates Domino’s store expansion of 250 stores each for FY24, FY25 and FY26 while overall store addition will be 277 in FY24, 312 in FY25 and 322 stores in FY26. It expects a 14 percent revenue CAGR during FY23-26E. With weak consumer sentiment, pressure on margin, and higher investments, it has cut EPS by 13 percent and 12 percent for FY24 and FY25.

"However, Jubilant, compared to its peers, has already seen a contraction in the margin in the last few quarters. Thus, we model lower contraction in FY24 as compared to its peers. The stock corrected by >30 percent in the last six months (despite it coming off of its peak) and normalised the valuation to some extent," it added.

Devyani International: The brokerage has initiated coverage with a ‘reduce’ call on the stock and a target price of ₹115, indicating a downside of 18 percent. The stock has also given negative returns for 6 straight months since October 2022. It is down 22 percent in 2023 YTD and 18 percent since October last year.

"With Yum’s sustained focus on expanding its store network in India since its entry, we believe healthy store expansion will continue over the next many years. We model an annual store addition for Devyani of around 225 stores during FY23-26. KFC is a long-term play as the chicken category has strong potential in India. We believe KFC will have a higher mix in Devyani’s store expansion. Devyani has taken various measures to improve Pizza Hut, but there are still several gaps vs. Domino's. The operating cost difference (due to different geographies), provides a 150-200bps margin difference despite having a similar gross margin. However, with the normalisation in demand, the impact of weak sentiment and high RM inflation, we believe margin pressure will be in FY24. High pent-up demand benefits have expanded the operating margin, which will be normalised over FY24 and FY25," said HDFC Securities.

Sapphire Foods: The brokerage has initiated coverage on the stock with a ‘reduce’ call and a target price of ₹1,000, indicating a downside of 14 percent. Sapphire has also been in the red for 6 consecutive months, down 20 percent since October 2020. It has lost 12 percent in 2023 YTD.

The brokerage pointed out that Sapphire has seen a sharp improvement in operating metrics (restaurant operating margin improved by >500bps in 9MFY23 vs. 9MFY20. With the normalisation in demand and the impact of weak consumer sentiment, it believes the operating margin will see an impact in FY24.

Westlife Foodworld: The brokerage has initiated coverage on the stock with an ‘add’ rating and a target price of ₹715, indicating an upside of just 7 percent. It is the only QSR stock that has not given consistent negative returns since October 2022. However, it is still down 15 percent in 2023 YTD.

"Westlife has a limited store/city network as compared to its peers as the business model is to extract more out of its store/city network. Thus, its revenue per store is significantly higher than others. McD has a relatively large format and dine-in focus its store and city expansion will be slower than others. However, Westlife’s store addition is expected to improve (35-40 stores per year) vs. the historical trend (25 stores per year), reflecting that the company is gradually becoming aggressive," explained HDFC Securities.

It further noted that the firm's profitability metric still has enough room to improve in the coming years. With better revenue per store, consistent new launches in the premium segment and higher McCafe addition, HDFC Securities believes there is scope for improvement. Westlife is a pure play QSR with no overhang of any turnaround and international business.

It has modeled a 17.8 percent and 18.7 percent margin for FY25 and FY26, respectively, for Westlife.

Valuation summary: HDFC Sec

First Published: 29 Mar 2023, 03:09 PM IST