Sun Pharma and Cipla have made their mark in a highly competitive pharma market with their affordable medicines and strong distribution network.

Sun Pharma vs Cipla: Which is a better pharma bet for long term?

TL;DR.

Even as the Nifty Pharma index gave negative returns in the last 1 year, down over 8 percent, both stocks gave double-digit positive returns during the period.

While the pharma sector performed extraordinarily well during the COVID period, 2022 saw a lull. On the back of fears of COVID re-emerging, the pharma space is buzzing again with the sector likely to perform well in 2023.

However, between Cipla and Sun Pharma, what should one bet on for long-term investment? Let's find out.

Stock price trend

Even as the Nifty Pharma index gave negative returns in the last 1 year, down over 8 percent, both stocks gave double-digit positive returns during the period.

In the last 1 year, Cipla rose 17 percent whereas Sun Pharma advanced 21 percent. In December, however, both Sun Pharma and Cipla gave negative returns, down around 5 percent each.

Looking at long-term returns, both Sun Pharma and Cipla gave multi-bagger returns in the past 3 years. While Cipla soared 132 percent, Sun Pharma rallied 128 percent. Meanwhile, in the last 5 years, both Cipla and Sun Pharma advanced around 75 percent each.

About the firms

Sun Pharma is the largest pharmaceutical company in India, with a market share of 8.2 percent. It is also the fourth largest specialty generic pharmaceutical company globally with a diversified portfolio of over 2,000 products.

The company’s product portfolio includes generics, branded generics, specialty, over-the-counter (OTC)/consumer healthcare products, antiretrovirals (ARVs), active pharmaceutical ingredients (APIs) and intermediates. Its portfolio of specialty products and branded generics is available across 100 countries. The company operates manufacturing sites across 6 continents.

Cipla is the third-largest pharmaceutical company in India. It is actively engaged in the business of manufacturing and distributing medicines. The company boasts a portfolio of more than 1,500 products in 65 therapeutic areas across active pharmaceutical ingredients (APIs), generics, and over-the-counter consumer products. Its product portfolio spans complex generics, as well as drugs in the respiratory, anti-retroviral, urology, cardiology, anti-infective and central nervous system (CNS). The company's geographical segments include India, the United States, South Africa and the rest of the world. The company has a network of manufacturing, trading and other incidental operations in India and international markets. The company has approximately 46 manufacturing sites.

Cipla stock price trend

Earnings

In the September quarter, Sun Pharma reported a quarterly net profit of ₹2,262.2 crore, up 10.5 percent from the year earlier. Earnings before interest, tax, depreciation and amortization (Ebitda) rose 12.4 percent to ₹2,956.5 crore during the period. Meanwhile, its revenue jumped 13.8 percent YoY to ₹10,952 crore.

Cipla, on the other hand, reported a 10.9 percent year-on-year (YoY) rise in its September quarter consolidated net profit at ₹788.9 crore while its total revenue from operations increased 5.57 percent on year to ₹5,828.54 crore. Its EBITDA stood at ₹1,303 crore during the quarter and consolidated margins came in at 22.3 percent.

Overall, the revenue for Cipla has grown at a compound annual growth rate (CAGR) of 5.8 percent against 1.8 percent for Sun Pharma in the last five years. In terms of operating profit margin, Sun Pharma is leading with a five-year average of 17.5 percent, whereas for Cipla, it is 16.7 percent. The five-year average net profit margin for Sun Pharma stands at 9.3 percent whereas it is 7.4 percent for Cipla.

Which is a better stock?

Vinod Nair, Head of Research at Geojit Financial Services, has picked Sun Pharma over Cipla.

“Given its higher market share, superior profitability margins, strong balance sheet and competitive advantage of specialty pharma, we prefer Sun pharma over Cipla,” he said.

Nair stated that Cipla’s India business will continue to witness strong growth momentum, driven by the launch of prescription brands across chronic therapies, robust order flow from rural towns in the trade generics business, and portfolio expansion in wellness categories.

Upcoming product launches in the US business, market share gains in key therapeutic areas in the SAGA market, and the management’s continued focus on cost optimisation measures auger well for the company’s performance in the future. Revenue concentration of 45 percent in domestic markets will shield the company from global uncertainties, he added.

However, talking about Sun Pharma, he noted that with a continued focus on R&D spend and development of complex products, the management of Sun Pharma expects to gain momentum in the coming quarters. Increased sales from the company’s specialty business and expected approval for its product pipeline (93 ANDAs and 13 NDAs) should support the company’s topline growth in the near-term, Nair pointed out. Going ahead, he expects Sun Pharma’s revenue to grow at a CAGR of 13.1 percent in FY24E vs Cipla at 6.5 percent while maintaining its premium margins.

Meanwhile, Vinit Bolinjkar - Head of Research at Ventura Securities, prefers Cipla over Sun Pharma.

"Sun trades at 15.3x FY25 EV/EBITDA whereas Cipla is trading at 12x FY25 EV/EBITDA which gives us a valuation comfort when compared with Sun pharma, hence we prefer Cipla over Sun Pharma," he said.

As per the market expert, Sun pharma’s sales in the domestic market are continuously increasing coupled with strong growth in their specialty segment, however, recently its facility in Halol got an import alert from USFDA. This means that all the shipments from this facility to the US would be stopped. Halol facility accounted for around 10 percent of US revenue and 3 percent of the company’s consolidated revenue in FY22, informed Bolinjkar. Despite this, Sun pharma’s revenue/EBITDA are expected to grow at a CAGR of 11.6 percent/14 percent to ₹53,774/10,397 crore in FY25, he predicted.

On the other hand, adjusting for Covid-led sales, Cipla's domestic business grew by 15 percent and branded generics are expected to grow ahead of the market as it will face lower competition for the next two years at least. Cipla’s revenue/EBITDA in FY25 are expected to be ₹26,521/6,993 crore, which indicates a CAGR of 6.8 percent/15.4 percent over FY22, forecasted Bolinjkar.

Sun Pharma stock price trend

Outlook for Pharma in 2023

After proving tenacity in the most challenging of circumstances and seizing the enormous opportunities presented by the pandemic, pharma stocks witnessed a decline in 2022. However, now, the valuations have moderated and stand comfortable, noted Nair of Geojit. Companies are now shifting their focus onto spaces of their expertise, away from Covid-related products, he added.

"While price erosion in the US continues to haunt domestic companies, declining raw material prices, currency depreciation and falling freight costs provide comfort to the companies. We continue to be bullish on the branded market due to its steady growth, and cautious on the developed-market generic segment due to high competition and regulatory concerns in the US. We remain optimistic on the sector owing to new launches, strong pipeline, increased R&D and superior product portfolio which are expected to aid earnings going ahead," said the expert.

Meanwhile, Bolinjkar stated that despite geopolitical issues, India continued to supply medicines to over 200 countries, living up to its reputation as the ‘pharmacy of the world’. The sector also faced challenges this year, however, as the industry expands its footprint around the world, it will need to continuously invest in upgrading manufacturing standards to keep its promise of being a high-quality, reliable supplier of medicines to the world, he highlighted.

Bolinjkar also informed that according to a recent EY FICCI report, as there has been a growing consensus over providing new innovative therapies to patients, the Indian pharmaceutical market is estimated to touch $130 billion in value by the end of 2030. Meanwhile, the global market size of pharmaceutical products is estimated to cross over the $1 trillion mark in 2023.

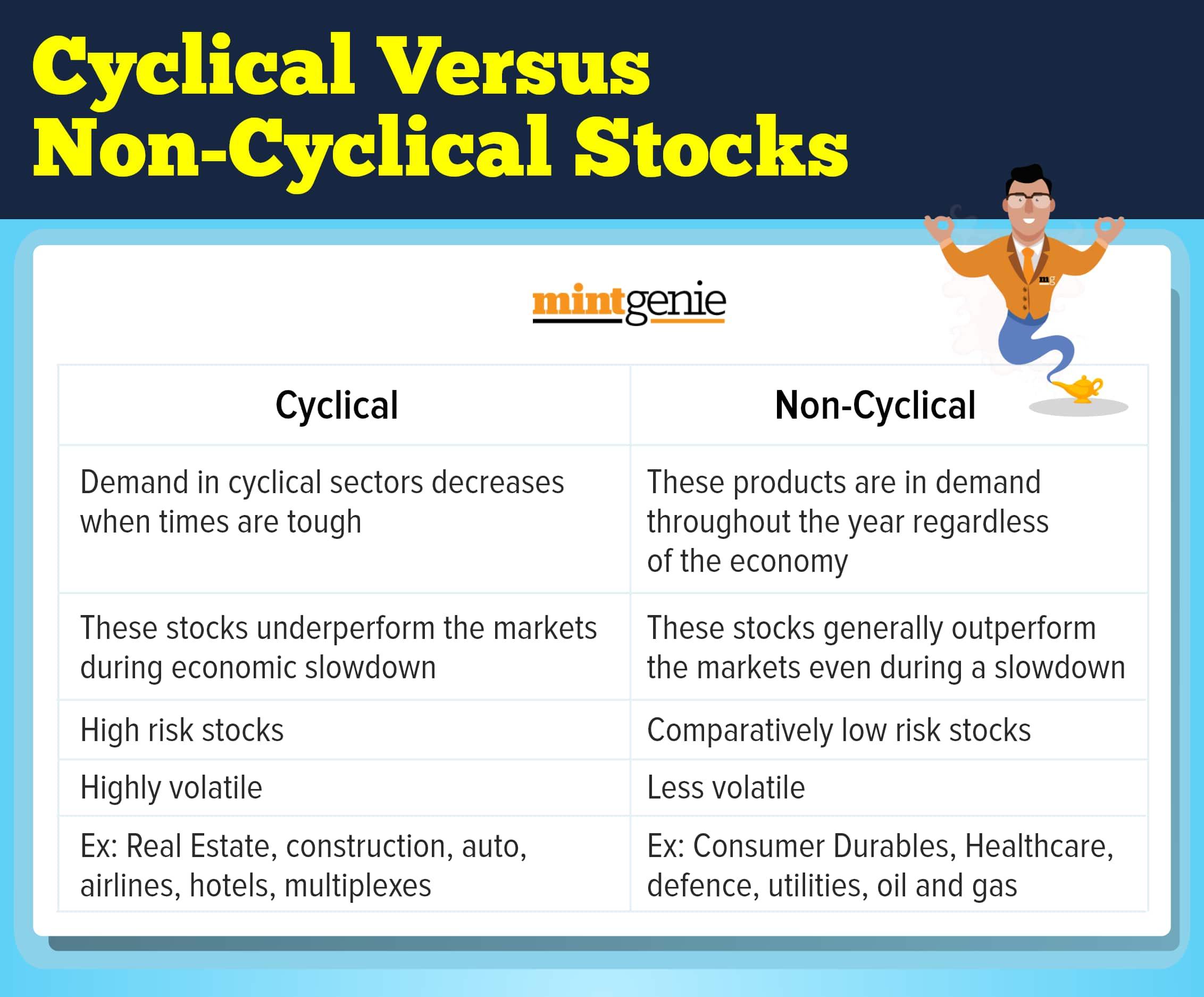

Cyclical vs non-cyclical

First Published: 06 Jan 2023, 01:25 PM IST