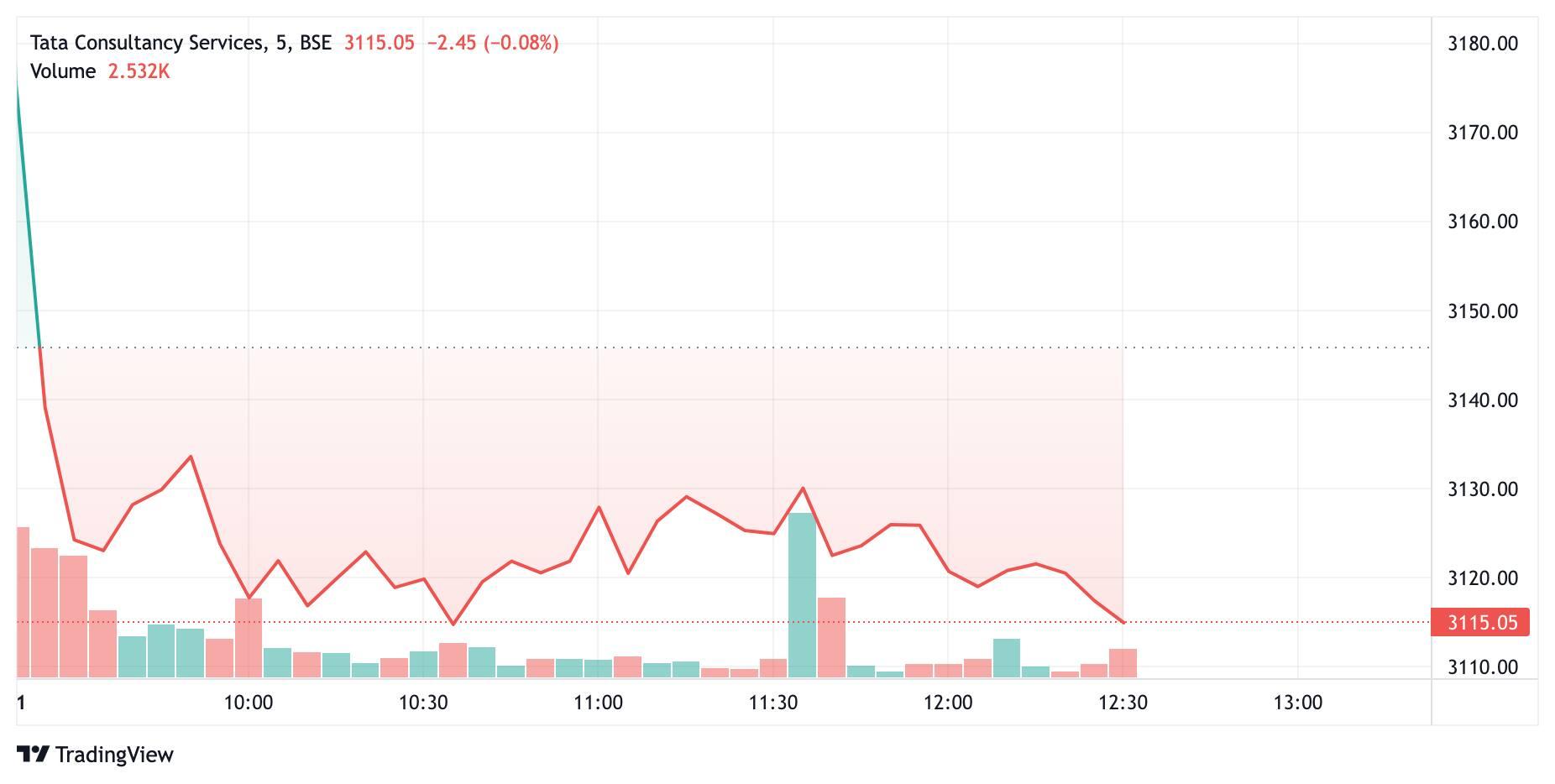

Shares of Tata Consultancy Services (TCS) fell almost 5 percent in trade on BSE on July 11 as investors sold shares of the IT major after the firm's June quarter net profit numbers came below market estimates.

The stock ended 4.64 percent lower at ₹3,113.25.

TCS on July 8 reported a 5% increase in its net profit at ₹9,478 crore for the June quarter of FY23 against a profit of ₹9,008 crore from the same quarter last year. The profit was down 4.5% sequentially from ₹9,926 crore recorded in the previous quarter ending March 2022.

TCS' revenue from operations for Q1FY23 came at ₹52,758 crore, up over 16% from ₹45,411 crore year-on-year (YoY), and a rise of about 4% quarter-on-quarter (QoQ).

Brokerages mixed

Brokerage firms have expressed their mixed views on TCS after the IT bellwether's Q1FY23 numbers.

JPMorgan has an 'underweight' call on TCS with a target price of ₹2,800, and as per CNBC-TV18, the brokerage firm said that the company's results and margin trajectory don't stand up to the burden of valuations.

JPMorgan termed TCS' Q1 prints as underwhelming and said it sees sustained margin pressure in FY23 from supply challenges.

"We expect revenue headwinds in the second half due to macro concerns and we see the company's margin below 25% for foreseeable future," CNBC-TV18 quoted JPMorgan saying so, adding, that the brokerage firm has cut TCS' margin estimates by 30 bps and earnings estimates by 2-3% over FY23-25.

Another brokerage firm Nomura has a 'reduce' call on TCS with a target price of ₹2,910. As per CNBC-TV18, Nomura said TCS is facing the brunt of weakening growth and margin headwinds.

Credit Suisse downgraded the stock to a 'neutral' from an 'overweight' and as per CNBC-TV18, the brokerage firm has cut TCS' FY23-25 EPS estimates by 3-10%.

Goldman Sachs, on the other hand, maintained a 'buy' call on TCS with a target price of ₹3,678. As per CNBC-TV18, Goldman Sachs said the company's Q1 was in-line as the focus on chasing demand remains intact. However, Goldman Sachs added that the company's order book and employee headcount slowed down sequentially, indicating a slowdown ahead.

Among the domestic brokerage firms, JM Financial has a 'hold' call on the stock and cut the target price to ₹3,600 from ₹3,760.

"Adverse cross-currency headwinds and a tad light Q1FY23 drive 2.3-3.3% cut in FY22-25E EPS. TCS’s mixed results are unlikely to reverse the street’s concerns about the sector’s growth impairment notwithstanding the relatively confident but watchful commentary," said JM Financial.

Kotak Securities has an 'add' call on the stock with a target price of ₹3,400.

"We do expect some moderation in IT spending in growth for a short period and expect normalization subsequently. As is always the case, TCS will comfortably outpace global IT spending. TCS’ business is well sorted. Its service line revenue mix between discretionary and run-the-business (RTB) services mirrors global IT spending," Kotak said.

"Its diversified presence across verticals, geographies and ability to drive transformation agenda (on costs as well as business transformation) is impressive. The supply side is better managed than its peers. The company is most likely to gain in vendor consolidation exercise. Our EPS estimates go down marginally for FY23E and remain unchanged for FY24E," the brokerage firm added.

Motilal Oswal Financial Services has a 'buy' call on the stock with a target price of ₹3,730.

"Increase in interest rates, slow economic growth, and elevated geopolitical tensions have impacted the macro environment and raised concerns over IT spending. Given TCS’ size, order book, and exposure to long-duration orders, and portfolio, it is well-positioned to withstand the weakening macro environment and ride on the anticipated industry growth," said Motilal Oswal.

"TCS has consistently maintained its market leadership position and shown best-in-class execution. It allows the company to maintain its industry-leading margin and demonstrate superior return ratios," the brokerage firm added.

According to a MintGenie poll and an average of 45 analysts has a ‘hold’ call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking firms and not of MintGenie.