Brokerage house HDFC Securities believes there are testing times ahead for Alkyl Amines Chemicals (AACL). It has downgraded the stock to 'sell' from 'reduce' with a target price of ₹2,100, indicating a downside of 15.5 percent from its current market price of ₹2,489.70 (as on July 19).

"The dumping of products by Chinese chemical manufacturers has resulted in a sharp correction in the prices of key products of the company. AACL has to pass on the benefit of falling raw material prices to its customers in the coming quarters in order to retain its market share. The agrochemical industry contributes 20 percent to the company’s topline. AACL is facing challenges, given the demand slowdown in the agrochemical industry. Demand headwinds and competition from Chinese manufacturers could result in a correction in per kg margins," explained the brokerage.

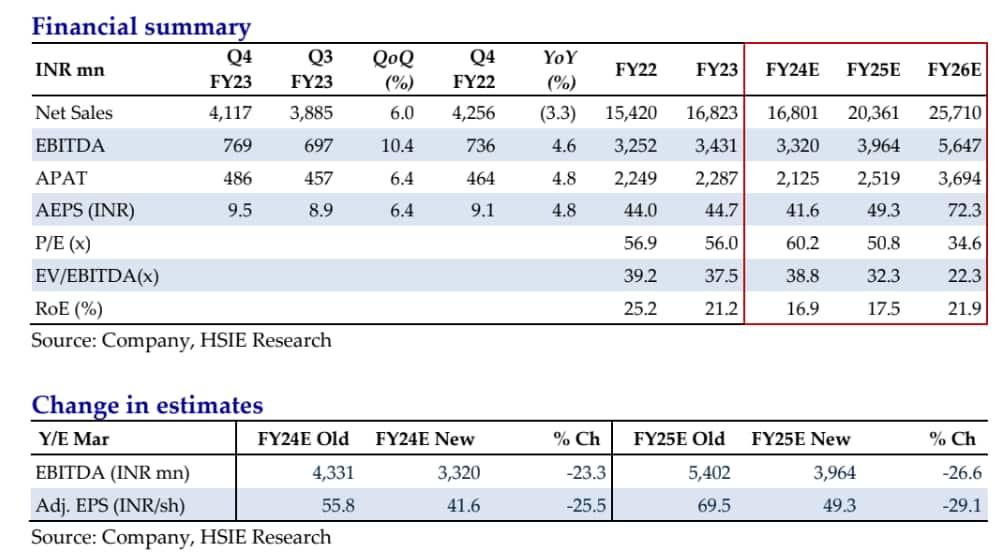

It also believes that the current valuation already factors in positives from potential volume growth, after 40 percent additional capacities of the aliphatic amines plant and ramp-up in utilisation of acetonitrile capacity. It expects an adjusted PAT CAGR of 5 percent over FY23-25E, led by an EBITDA CAGR of 8 percent over the same period. RoE and RoCE shall fall to 18 percent and 16 percent in FY25E from 21 percent and 19 percent in FY23, respectively, forecasted the brokerage.

Stock price trend

The stock has shed 7 percent in the last 1 year and 6.5 percent in 2023 YTD. It has declined nearly 9 percent in July so far, snapping its 3-month gaining streak. It rose 10 percent in June, 4.7 percent in May and 9.68 percent in April. However, the stock gave negative returns in the first 3 months of this calendar year as well. It lost 12.8 percent in March, 4.8 percent in Feb and 1.2 percent in Jan.

Reasons for downgrade

China: Chinese players have been dumping their products aggressively in India, at prices even lower than the cost price. This has put pressure on margins. In order to protect its margins, AACL focused on exporting its products to the US. Owing to this, the exports have increased to 23 percent in the sales mix in FY23 (vs 18 percent in FY22). The share of exports in overall revenue shall remain higher in the current year as well, noted the brokerage.

It further added that the management expects this pressure from Chinese dumping to ease in the next six months.

Input prices: Though input prices including that of ammonia, methanol and acetic acid have cooled down by about 35%, 15% and 64% YoY in Q1FY24, AACL has to pass on the benefit of falling prices to its customers as the company is facing intense competition from Chinese manufacturers. This will result in a fall in average per kg realisation and average per kg EBITDA, it stated.

Positives

Capex: The company had announced a Capex of INR ~2.5bn in Nov-22 to put up a capacity of 25-30kTPA at its existing facilities at Kurkumbh, Maharashtra, and Dahej, Gujarat, to manufacture five new products in the specialty chemicals and amine derivatives business, informed the brokerage. These products are largely import substitutes that cater mainly to the pharma and agrochemical industries. This Capex can generate incremental revenue of ₹600-800 crore at full utilisation, it estimates.

It also plans to spend ₹200 and 150 crore on Capex in FY24E and FY25E. The company is also looking to buy a land parcel in Gujarat, whose Capex will be announced once the company gets land allotment. Currently, the company has enough unutilised land at Kurkumbh and Dahej to support medium-term growth, added the brokerage.

Estimates

The brokerage cut its FY24/25 EPS estimates by 25.5/29.1% to ₹41.6/49.3 per share to account for reduced realisations across products, courtesy of a correction in raw material prices and to factor in increased dumping of products at aggressive prices by Chinese manufacturers.