The US Federal Reserve is likely to raise its benchmark interest rate by 25 basis points to the 5.25-5.50 percent range in its July 26 meet. This has been one of the most aggressive rate hiking campaigns in history by the US Federal Reserve, which started well over a year ago. However, the Street expects it to be the last increase of the current tightening cycle. But with rates at peak, the famous 60/40 portfolio no longer seems to be the best strategy. So what is? Global brokerage house Morgan Stanley answers.

The 60/40 portfolio strategy may no longer work, says MS; here's what it suggests now

TL;DR.

With interest rates at peak, the famous 60/40 portfolio no longer seems to be the best strategy. So what is? Global brokerage house Morgan Stanley answers.

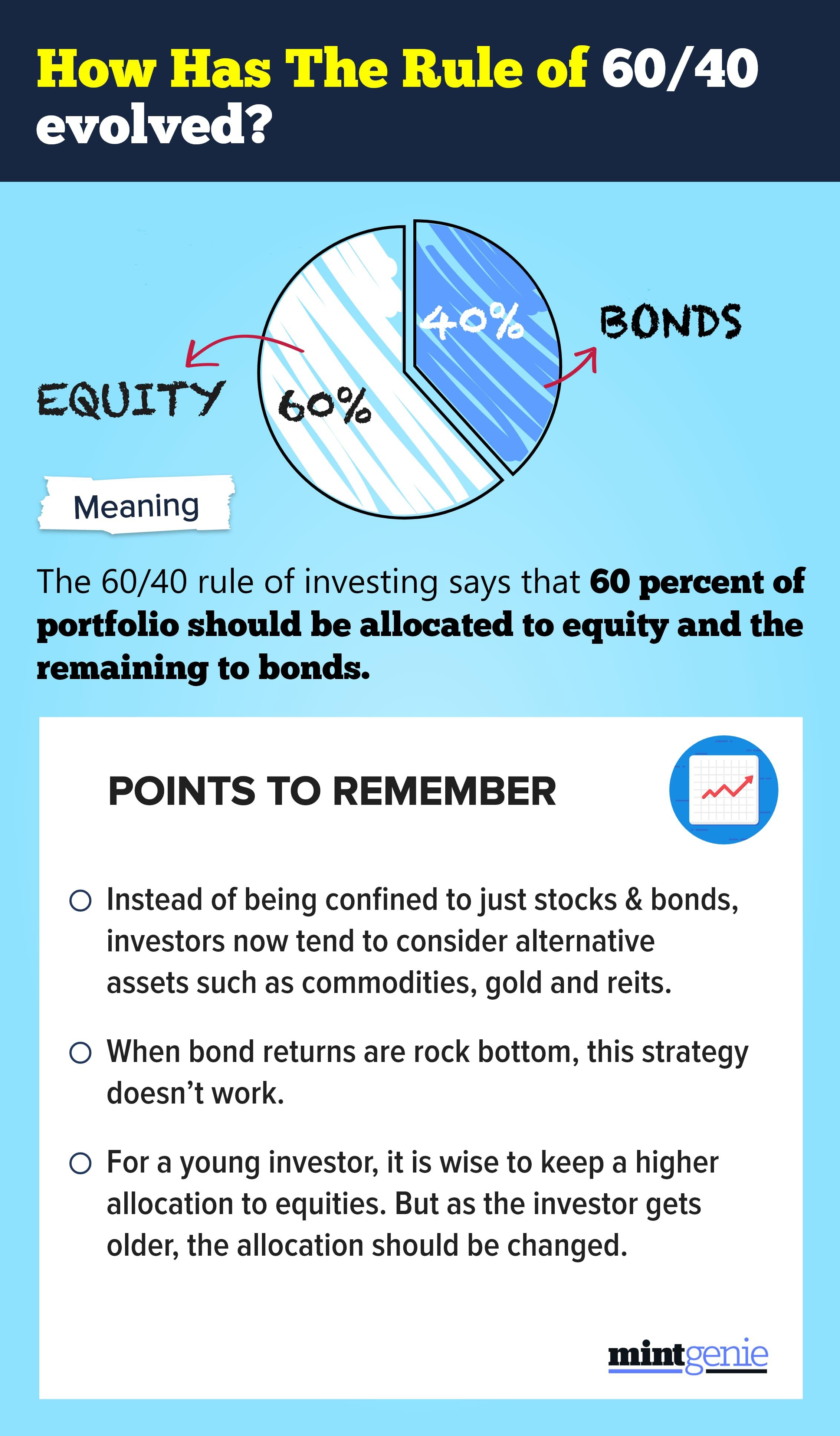

First, let us revise the 60/40 rule of investing. It is a tried and tested portfolio allocation formula which says that a balanced portfolio comprises 60 percent of equity and the remaining 40 percent of bonds. This is based on the premise that in the long run, equity gives a higher return while bonds add a stable income to the portfolio.

What changed?

The recent report by Morgan Stanley pointed out that over the past 40 years, since 1980, interest rates have declined, meaning bond prices have generally increased. Now that this 40-year trend of declining interest rates has ended—and rather abruptly— investors are struggling to find ways to create an efficient portfolio with more stable returns.

"It appears that bonds may no longer provide the portfolio ballast that they have for the past decade and the traditional 60/40 portfolio might no longer work as expected," warned the brokerage.

The pandemic changed everything and today it has once again triggered the same age-old debate about the most efficient balance of risks in a portfolio of stocks and bonds, and what might be the volatility of returns in the future. Is a passive 60/40 portfolio the optimal solution as many investors thought was the case for many, many years? Or is there something better?

Despite the concern, the brokerage noted that investors cannot ignore the fact that the 60/40 portfolio worked pretty well for 40 years.

In other words, holding bonds passively lowered the beta, or risk, of the portfolio. But is this still true?

As per the brokerage, the direction of interest rates in the near- and longer-term future provides critical information. If interest rates do not trend lower, but shuttle sideways in a limited range, or even drift higher, then the traditional passive 60/40 portfolio is suboptimal, it stated. The solution is an actively balanced portfolio that seeks to reduce the volatility of returns, it highlighted.

It further explained that the advantage of stabilising return volatility is that it allows an investor to compound returns more predictably into the future. MS believes the key to compounding returns is by investing in a balanced strategy that has demonstrated the ability to control risk.

Objective of 60/40 portfolio

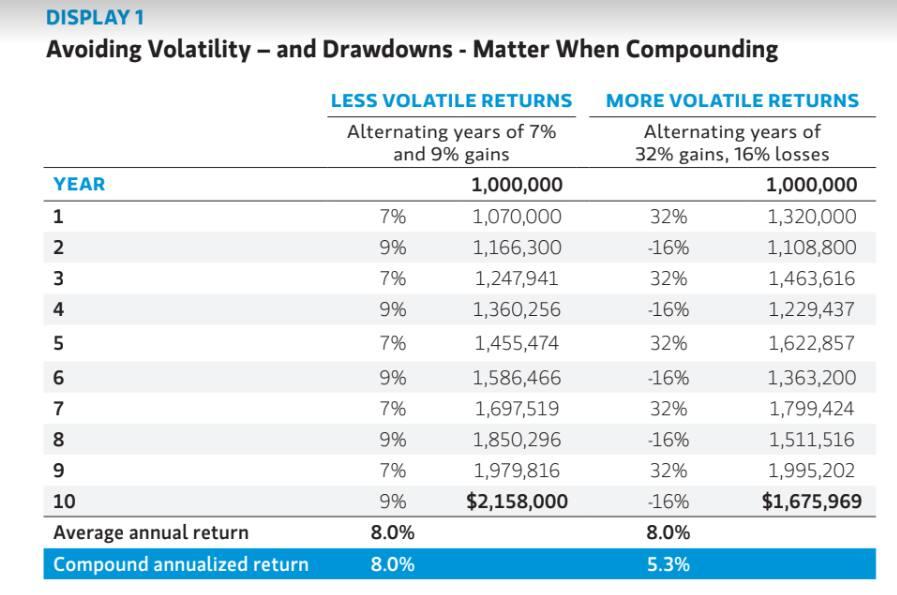

Morgan Stanley also noted that the objective of the 60/40 portfolio was to reduce the volatility of returns over a long-term investment horizon by balancing the risks between the equities and bonds an investor held in a portfolio. The overriding goal was to try to minimise downside risk, or drawdowns, and participate in the upside—and the importance of avoiding drawdowns cannot be overemphasised, added the brokerage.

"Drawdowns are those moments in volatile markets that every investor has been through when their portfolio is losing money “on paper” to the point where the fear becomes palpable and they can’t take it anymore. The ability to withstand drawdowns in some ways represents an investor’s risk tolerance. During severe drawdowns (think the GFC of 2008-09) some investors sell near a market bottom, which is generally the worst time to sell. This is a real risk, and the issue with significant drawdowns “on paper” or otherwise is the simple math involved; if an investor loses 50 percent of their portfolio in an extreme drawdown their portfolio now has to earn 100 percent just to get back to even," it explained.

It believes that when balancing the risks in a portfolio, with fewer and less extreme drawdowns, an investor has a better chance of compounding returns in a stable and predictable manner.

Source: Morgan stanley

Why 60/40 worked?

The brokerage informed that the 60/40 portfolio worked well for investors from 1982 to 2021. Broadly speaking, holding bonds lowered the beta of the portfolio, but what really made the 60/40 allocation work was that the bonds generated positive returns in 36 out of 40 years.

The down years for bonds were:

• 1994, which was the worst all-time

year until 2022 (-2.9 percent)

• 2013, during the “taper tantrum” (-2.0 percent)

• 2018, where bonds were essentially flat (0.0 percent) but generated negative return after fees.

• 2021 (-1.5 percent)

On average, the brokerage noted that bonds returned roughly 7.6 percent a year from 1982 to 2021, and during those down years for bonds in 1994, 2013, 2018, and 2021, equities returned around 7.3 percent, on average, meaning that holding stocks and bonds in a 60/40 portfolio worked out reasonably well. All told, bonds compensated investors quite nicely for equity risk and lowered the volatility of returns for the overall portfolio. To be crystal clear, the driving force of the success of the 60/40 portfolio was the consistency of bond returns, highlighted MS.

Will bonds continue their historical string of positive returns?

If 2022 is any indication of the future, maybe not, as bonds were down -13.0 percent, which made 2022 a particularly bad year because equities were down too, something that hadn’t happened since 1994, noted the brokerage. Equities and bonds generally had a low correlation, meaning they did not move synchronously, and that was the essential selling point of that traditional 60/40 portfolio. But the burden of future success for bonds is in the interest rate cycle because history shows that roughly 85 percent of bond returns were attributable to movements in interest rates, explained the brokerage.

To reiterate, since rates trended lower from 1982 to 2021, bond returns were typically positive. But if interest rates trend sideways in a range into the future then bonds will not be the steady hedge to equities they once were, invalidating a 60/40 balance. If rates drift higher, then bonds become even more circumspect as a hedge that provides stable returns when matched against equities. As a result. the beta, the risk factor of the 60/40 portfolio, is likely to increase, mentioned the brokerage.

What's the solution?

To start with, MS believes the solution is active management, not passively investing in a portfolio and watching in frustration as it does not do what it was expected to do—and unable to do anything about it. More specifically, the solution is to adopt actively managed strategies that pair the risks of assets held in a portfolio against each other in order to help reduce the volatility, it stated.

As per the brokerage, this is an alternative beta strategy, compared to a strategy that relies on historical bond returns during a time when interest rates are trending lower.

"In other words, an investor needs to be more concerned about how a manager is balancing the risks in one’s portfolio through asset allocation decisions with the objective of reducing the volatility of returns. This brings us right back to where we started: reducing return volatility, limiting the risk of significant drawdowns and helping to stabilise returns so they are more predictable and can compound over time. This can be achieved by balancing the risks in the portfolio but also providing a framework and the discipline to control risk," it explained.

Overall, the brokerage believes that the start of a secularly changing investment environment is already underway, an environment in which static 60/40 allocation strategies will be suboptimal. It does not believe that bonds can provide portfolio ballast in the near and longer-term future. Furthermore, they can no longer be expected to have a low correlation to equities and to help reduce the risk.

To manage ongoing market volatility and minimise potential participation in those severe drawdowns that can erode the ability to compound effectively, the brokerage suggests that investors will need an active volatility manager.

Usually the strategy of 60/40 doesn't work when the bond returns are rock bottom.

First Published: 21 Jul 2023, 09:13 AM IST

Topics to follow

Related Stories

Explain Like I am 5

personal finance

What is a roll-down strategy followed by debt funds? All you want to know

Team MintGeniepersonal finance

Should you tweak your investing strategy based on inflation? MintGenie explains

Team MintGenie