Brokerages cheered Titan after the Tata Group company posted better-than-expected results for the March quarter of FY23 (Q4FY23). The company's standalone net profit jumped 50 percent year-on-year (YoY) to ₹734 crore in the March quarter as against ₹491 crore in the year-ago period.

Meanwhile, its revenue from operations surged 33 percent to ₹9,704 crore for the quarter under review versus ₹7,276 crore in the year-ago period.

"The year gone by witnessed several firsts for Titan. The jewellery, watches and wearables, and eyecare achieved landmark milestones of annual consumer retail sales. After a satisfying performance across all the segments during FY23, we are well prepared and looking forward to an exciting FY24," said C K Venkataraman, MD, Titan.

However, with gold prices near an all-time high and inflation pinching customers’ pockets, demand volatility is here to stay, said Titan’s jewellery division CEO Ajoy Chawla.

“With gold prices spiking, there is some degree of nervousness in customers. The first half of April was dull, but the second half was fantastic. May and June promise to be good because of a lot of wedding dates,” he said in an analyst call after Q4 results.

The company's strong performance in the March quarter has earned positive ratings from most brokerages. Let's see what they have to say:

Prabhudas Lilladher

The brokerage is bullish on the stock with a target price of ₹2,992, indicating an upside of 13 percent. PL remains constructive on Titan post Q4 results given strong underlying demand trends in jewellery and scalability in wearables, eyewear and Taneira. The brokerage noted that the company's Q3 results were a miss on EBIDTA due to lower margins in watches, and eyewear and higher losses in emerging businesses. However, Titan is now focusing on volume-led growth in jewellery given rising competition while superior mix and scale which will help sustain margins, it added.

PL expects Titan to capitalise on long-term growth opportunities led by 1) jewellery segment gains due to network expansion, regional thrust and higher growth in sub-brands like Mia, Zoya and Caratlane 2) omni-channel strategy across jewellery, watches and eyewear 3) new growth drivers like Caratlane, Titan Eye+, Taneira and 4) strong growth in wearables with smartwatch volumes exceeding 1 million in FY23.

It believes Eyewear and CaratLane have reached critical mass with FY23 EBIT of ₹98 crore and ₹166 crore (96 percent and 177 percent growth) and will be key growth drivers in coming years. Titan is gradually emerging as a lifestyle play and that will help sustain premium valuations, it added.

Religare Broking

The brokerage has a ‘buy’ call on the stock with a target price of ₹3,147, indicating an upside of over 18 percent. Titan’s Q4FY23 topline performance was better than estimates driven by healthy consumer demand during the wedding season, said Religare.

It further stated that Titan has a strong foothold in the jewellery and wristwatches category with a wide range of product portfolios. It caters to a diversified range of customers which enables stability in growth for the company. Going ahead, the company aims to increase its market share by penetrating rural areas and continues to add more stores in the international market which will aid the topline growth, noted Religare. Financially, it estimates Titan's revenue/EBITDA/PAT to grow at a CAGR of 13.7 percent/23.2 percent/23.6 percent over FY23-25E.

Phillip Capital

The brokerage has a ‘buy’ call on the stock with a target price of ₹3,000, indicating an upside of 13 percent. As per the brokerage, long-term drivers for Titan remain intact including (1) increasing consumer shift to organised jewellery, as unorganised jewellers find it difficult to operate due to increasing cost of compliance in an industry where margins are wafer-thin, (2) aggression in the highly lucrative wedding jewellery market, (3) increasing traction on the revised gold exchange programme for Titan’s Golden Harvest Scheme (4) stringent cost efficiency program, and (5) network expansion in Tier 2/ Tier 3 and targeting market leadership in those markets.

However, PC has cut its FY24-25 EPS estimates by 6-10 percent for Titan to account for a) increased competitive intensity on the gold rate front b) diamond inventory gains no longer being available over FY24-25 and c) higher volatility in the gold price which will eventually lead to deferment of demand. The brokerage continues to remain cautiously optimistic about the stock as structural levers remain intact despite near-term concerns.

Motilal Oswal

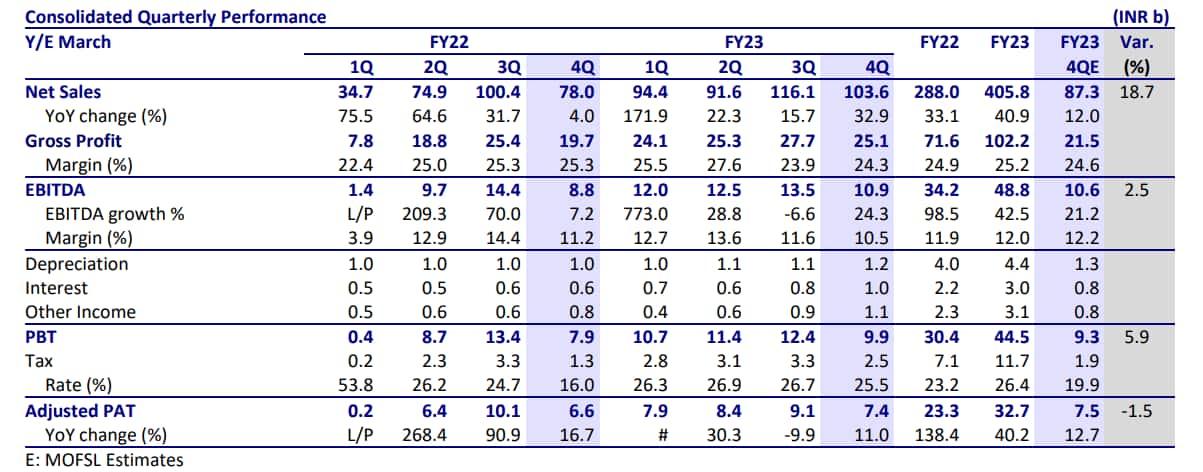

The brokerage has a ‘buy’ call on the stock with a target price of ₹3,080, indicating an upside of 16 percent. “Titan Company's Q4FY23 revenue was 19 percent ahead of our expectation; however, due to lower-than-expected margin, EBITDA and adjusted PAT came in line with estimates,” said MOSL. As per the brokerage, Titan boasts of an outstanding track record that surpasses its peers, with superior short-term growth prospects, and exceptional long-term growth potential, all of which justify its high valuations. “There are no material changes to our FY24 and FY25 forecasts,” informed the brokerage.

It also pointed out that Titan has been able to surmount two of the challenges on the back of a) exceptionally high wedding jewellery sales and b) the potential near-term impact of the gold price increase. It also said that Titan's outlook remains robust and it has ample opportunities for growth, given its market share of sub-10 percent in jewellery and the ongoing challenges faced by its unorganized and organized peers. Its medium-to-long-term earnings growth potential is unparalleled, added MOSL.