Late Rakesh Jhunjhunwala-backed Tata Group firm Titan Company has been an outperformer, giving positive returns to its investors for 4 straight months. Since July 2022, the stock has risen 40 percent as against a 12 percent rise in benchmark Nifty in this period. In a recent note, brokerage house Motilal Oswal (MOSL) said that it believes Titan will continue to be a standout performer and its medium-to-long-term outlook remains attractive. It sees the stock breaching the ₹3,000 mark in the next 1 year

Titan to breach ₹3000 mark in next 12 months, says Motilal Oswal

TL;DR.

In a recent note, brokerage house Motilal Oswal (MOSL) said that it believes Titan will continue to be a standout performer and its medium-to-long-term outlook remains attractive. It sees the stock breaching the ₹3,000 mark in the next 1 year.

The brokerage has a 'buy' call on the stock with a target price of ₹3,135, indicating an upside of 17 percent from the current market price.

"Titan has been the standout performer among all of its Consumer peers, in terms of revenue, earnings, as well as stock price performance over the past five years. For a company of its size, sales of ₹36,600 crore in FY23E and the 20 percent revenue and earnings CAGR is extremely impressive," noted the brokerage.

Stock Price Trend

In the 10 months of 2022, the stock has given positive returns in 5 and negative in the other 5 months. It surged the most in July, up 21 percent followed by in August, up 11 percent. Meanwhile, it shed the most in June, down 12 percent followed by in May, down 10 percent.

In 2022 YTD, the stock is up 7.5 percent whereas, in the last 1 year, it has added 9 percent.

Titan stock price trend

Business Update

Earlier this month, in a business update, the firm announced that its overall sales grew 18 percent year-on-year in the September quarter. The company has witnessed "healthy double-digit growth across most businesses," it said in a quarterly update. Titan added 105 stores in its retail network in the second quarter of the current fiscal.

"We continue to be optimistic and are visible in positive consumer sentiment across categories. During the September quarter, Titan's jewellery division, which contributes around 85 percent of its revenue, grew 18 percent YoY on a high base of Q2FY22 that had elements of pent-up demand and spillover purchases of a Covid-disrupted Q1FY22," it said. Its Watches & Wearables grew 20 percent YoY, clocking its highest quarterly revenue while the EyeCare business saw 7 percent YoY growth.

Factors to look out for

While the medium-to-long-term outlook for Titan is attractive, MOSL has highlighted some factors that need to be monitored closely in the near term.

a) Extremely high festive season base of the past two years – part of which was driven by unusual occurrences like travel and catering restrictions, leading to an extremely high share of Jewelry in the wedding budget. Its performance in Q3FY23 over an extraordinarily high base of growth in the preceding couple of years noted MOSL.

b) The global economic situation, which can result in a spike in gold prices spike and lead to a postponement in demand, especially on the adornment side.

c) A further increase in the import duty or other curbs on gold supplies, given the weak fiscal and BoP situation.

d) A delay in a recovery of the Studded segment (which is still not back to pre-COVID levels), can have an impact on margin and earnings growth.

e) Whether OCF growth will keep pace with the stellar pace of earnings growth going forward, which has not been the case for the past five years. Despite extremely strong growth in revenue and earnings over the past five years, performance on OCF and FCF have not been as impressive, with higher inventory days and other assets being the key factors behind the same, said MOSL.

While FY21 and FY22 may have been affected due to the immense volatility caused by the COVID-19 pandemic, these two line items will be key monitorables in the FY23 Balance Sheet and beyond, it added.

Positives

Impressive performance: The brokerage noted that the company maintained its strong growth trajectory (three-year Revenue/PAT CAGR at 20 percent/27 percent), even during the COVID-impacted period (FY20-FY22) – at a time when most Retail peers were struggling. This was especially commendable for a business that is predominantly a brick-and-mortar retailer and was achieved, despite a near washout in Q1FY21 due to the first COVID wave and much lower than usual sales in Q1FY22 due to the second wave, added the brokerage.

Long runway for the Jewelry segment: "In its May’22 analyst meet, the management aims to grow the Jewelry business by 2.5x over FY22-27, which we believe is achievable given Titan's lower share (less than 10 percent) in the Indian Jewelry market and its initiatives on various fronts to expand its footprint," explained the brokerage.

Targets for growth in other businesses are also aggressive: For Watches and Wearables, the company is targeting ₹10,000 crore in sales, with an EBIT margin of 18 percent in five years, which is a massive growth from its FY22 sales of ₹2,300 crore and an EBIT margin of 6 percent, MOSL pointed out. The targets for Eyewear, Ethnic Wear (Taneira), and international business are also aggressive, it added.

Outlook

As per the brokerage, Titan has a strong runway for growth, given its market share of sub-10 percent in the Indian Jewelry market and the continued struggles faced by its unorganized peers. Its medium-to-long-term earnings growth visibility is non-pareil among largecap consumer and Retail companies.

Despite the volatility in gold prices and COVIDled disruptions, earnings CAGR have been stellar at 24 percent for the past five years ending FY22, it informed. MOSL expects this trend to continue, with a 26 percent earnings CAGR over FY22-24.

"The stock trades at expensive multiples, but its long runway for profitable growth warrants a premium valuation. We maintain our Buy rating on the stock with a TP of INR3,135 (65x Sep’24 EPS)," it said.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

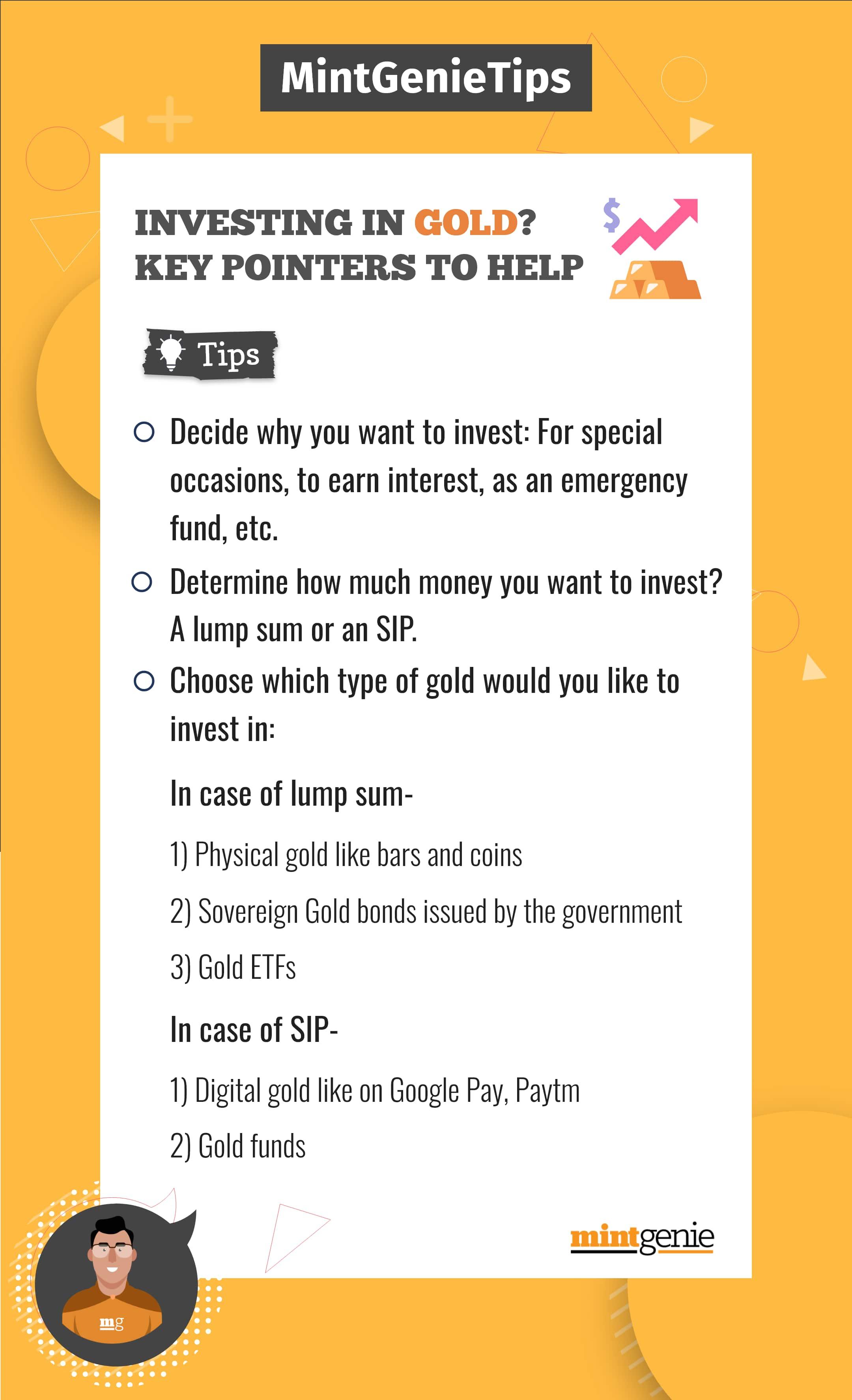

We explain here how to invest in gold

First Published: 27 Oct 2022, 12:45 PM IST