Investing in equity can help you achieve the goal of long-term wealth creation. However, there’s no denying that the markets can be very volatile. Entering or exiting the market at the wrong time can be a costly mistake. Fortunately, there are financial products that can help you invest in equity without the burden of having to time the markets. One of them is Unit Linked Insurance Plan (ULIP).

A ULIP gives you many benefits, right from a life cover and market-linked investments to tax benefits and several insurers even offer free fund switching (enabling you to choose your kind of market investments and manage your market risks anytime). With the right investment strategy, you can maximize the benefits from your ULIP further and optimize the returns you earn over the policy term.

One of the most preferred strategies in this regard involves investing small sums in ULIPs systematically, over the tenure of the policy. Similarly, you can also withdraw your investment, also known as maturity benefit, at the end of the policy tenure periodically, instead of doing it all at once.

How does this strategy work?

Normally, when you invest in a fund or a scheme, you may park a lump sum of money at the outset. And at the end of the investment tenure, you may redeem your investments entirely, in one go.

The same goes for a ULIP too. You may pay a lump sum premium at the time of purchase and then withdraw your corpus entirely at maturity. But in this systematic investment technique, you need to pay your premiums regularly over several years.

Similarly, at maturity, you have the option to withdraw your corpus in instalments. This pattern of investing and liquidating your holdings methodically, at regular intervals, has many advantages.

Let’s take a closer look at some of the top benefits of this approach.

1. You can invest with more discipline

In this investment strategy, you need to invest your ULIP premium on a monthly, quarterly, semi-annual or annual basis. Whichever frequency of investments you choose, you need to do this regularly and on time. This helps you develop financial discipline over time.

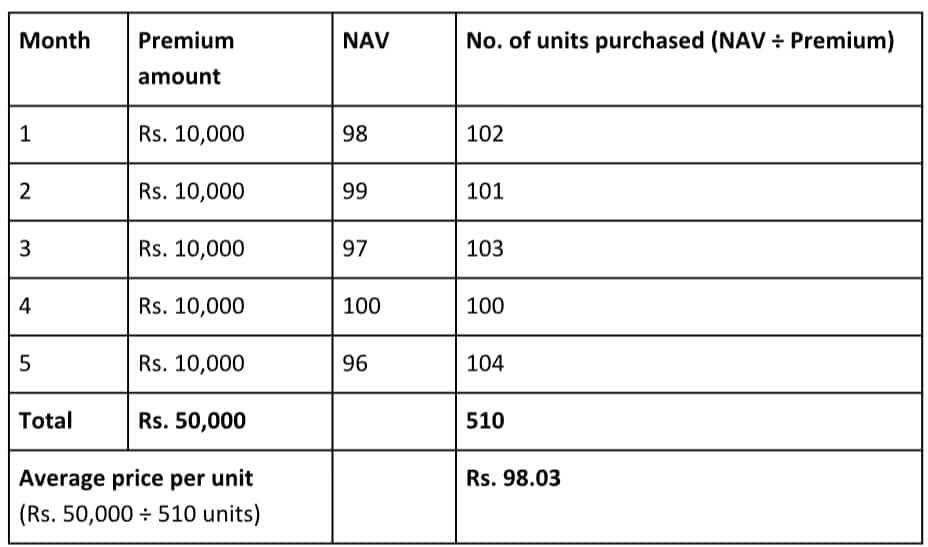

2. You benefit from rupee cost averaging

When you buy your ULIP with a lump sum premium, your investments will be made on the market price as of that date, whether higher or lower. However, when you follow the pattern of investing small sums periodically, you get the benefit of rupee cost averaging.

Here is an overview of how it works.

Hence, your overall investment cost reduces, thereby increasing your net returns.

3. Your redemption amount may increase

In this pattern of investing, you not only invest systematically but also withdraw your corpus in small amounts, over a given period after the policy matures. So, just like how your purchase price averages out, your redemption amount also averages out, which can further grow since the remaining amount is still invested in the market with an opportunity to grow.

4. You spend more time in the market

By increasing the frequency of investments, you spend more time in the market. This allows you to ride out short-term volatility. Additionally, it also means you don’t need to time the market before investing, which can be a very tricky thing to do.

5. Your family can manage their finances better

A ULIP is essentially a life cover. So, in case something untoward happens to you, the insurance provider will pay out the death benefits due under the plan to your nominee. In case of a lump sum payout, your family may find it tough to manage the funds if they are not familiar with personal financing strategies. But breaking down the benefits into

smaller and systematic payouts gives your family a regular source of income to rely on. And it makes the finances easier to manage.

6. Tax Efficient product

A ULIP can help you save tax under Section 10(10D) of the Income Tax Act 1961 and is one of the components under Section 80C with deductions up to ₹1.5 lakh, the benefits being subject to provisions stated therein. Additionally, returns on ULIPs with an annual premium of up to Rs. 2.5L is tax-exempt subject to the above provisions.

Summing up

The primary advantage of this form of investment is that it applies the benefit of systematic money transfer at the investment as well as the withdrawal phase.

As a result, you get to enjoy the associated benefits in both phases of your financial journey. If you too can benefit from any of the points outlined above, consider this investment technique for your ULIP.

But if you’re having trouble charting out a solid investment and withdrawal strategy, it is always a good idea to approach a financial expert for some hands-on guidance.

You can also pick different investment plans and diversify your portfolio, as it helps you achieve your life goals across different life stages.

(Sameer Joshi is Chief Agency Officer, Bajaj Allianz Life)

Disclaimer: The views expressed in this article are of the author, not MintGenie.