The Indian stock market has performed well despite volatility this year. The benchmark Nifty has advanced 5 percent in 2022 even as most global peers pared most gains of the previous year.

Indian market not overpriced; Asia remains most attractive among emerging economies, says Deutsche Bank

TL;DR.

The gains in the Indian market are mainly on the back of continued strong economic momentum, a report by Deutsche Bank (DB) stated, adding that thus, it is difficult to see the market as fundamentally overpriced.

The gains in the Indian market are mainly on the back of continued strong economic momentum, a report by Deutsche Bank (DB) stated, adding that thus, it is difficult to see the market as fundamentally overpriced.

According to Deutsche Bank, a strong growth in corporate profits is expected in 2023.

Asian markets

The investment banking company pointed out that among emerging economies, Asian markets remain the most attractive.

"Strong capital flows to “safe havens” caused marked declines in valuations in northern Asian markets, such as South Korea, Taiwan and China in 2022. The average drop in these markets was around 20 percent, a trend that has now been partially reversed. These markets may make a comeback when the macroeconomic environment and investor sentiment improves," it explained.

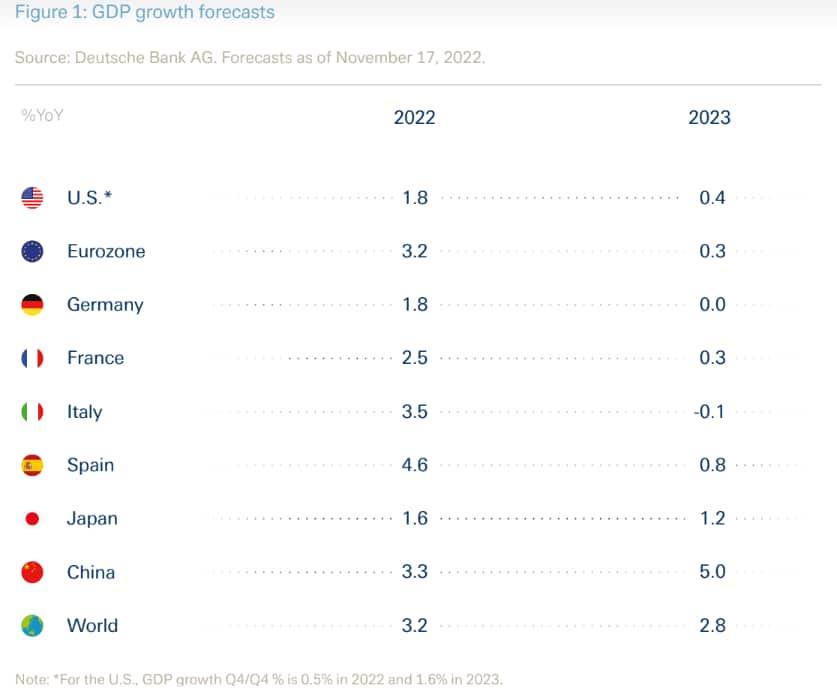

According to DB, India, Indonesia and China – three of the four most populous economies on earth with more than three billion inhabitants in total – could each see GDP grow by 5-6 percent in 2023. The developed economies of South Korea and Japan may also grow more rapidly than those of most other developed markets, it added.

The risks to growth in Asia in 2023 emanate primarily from increasing geopolitical tensions, especially in the Pacific, a potential reigniting of the Chinese real estate crisis, and from delays in rolling back the strict Covid-19 containment measures in China, said DB.

It further highlighted that India is currently expanding its manufacturing sector on a massive scale and launched a major infrastructure investment programme in early 2022 to encourage foreign company offshoots whereas the Japanese government is banking on comprehensive financial support to alleviate the energy crisis for its domestic businesses.

Source: DB report

Stock market strategy

2022 was a tough year for stock market investors. Despite the overall increase in corporate profits, stock prices came under pressure due to high geopolitical uncertainty, increasing inflation and a bond market sell-off, noted DB.

"The latter pushed real yields back into positive territory ending the era of TINA (There Is No Alternative) in which investors increased their stock allocations at the expense of bonds, driving equity valuations to near-record highs. After the yield moves of 2022, TINA has left the stage, though, and the market setting has flipped to TAPA (There Are Plenty of Alternatives), which has resulted in lower equity valuations. At the index level, the declines varied across stock market regions," it showcased.

For 2023, it said that stocks remain an essential component of a diversified portfolio. Decent overall price gains are expected in 2023, but with periods of perhaps substantial volatility, added DB.

It further added that revaluation for stock markets following the recent large interest rate hikes has now more or less ended. A high valuation phase due to very low-interest rates has been followed by a low valuation phase, and the stock markets are currently transitioning to a medium valuation phase for the years ahead. While this is no indication that 2023 will be a great year for stocks, it expects solid price increases in the single-digit percentage range.

Stocks, therefore, remain a particularly interesting asset class and essential components in a diversified portfolio, it added. Nonetheless, DB believes that short-term and even substantial price fluctuations could occur at any time during 2023 given investor caution, analysts’ continued overestimation of profits in some cases and the many political and economic risk factors. Market participants may continue to react strongly, even to less significant news, it cautioned.

It also said that although defensive sectors could continue to outperform over the medium term, valuations now look rich. Sectors that are more cyclical and value-oriented in nature appear attractive. Financials, materials (ex. chemicals) and energy stocks in particular are trading at depressed valuation levels on a historical comparison.

Investors wanting to position themselves more defensively may want to consider healthcare stocks, it advised. The sector offers above-average earnings growth supported by strong secular trends at a reasonable price, added DB.

Global markets

According to DB, in regional terms, one investor focus in 2023 could be Europe. Recent valuation discounts in this region have been disproportionately high, with economic and geopolitical risks already factored in, it said.

"Extensive fiscal programmes and high levels of savings should buoy private consumption, and expected stronger Chinese growth will be important to many European companies. The U.S. stock market will of course remain the focus, but its technology bias, and the resulting greater sensitivity to interest rate movements, may lead to greater investment risks, as could the expected weakening in the USD," noted the bank.

Global macro outlook

Weak economic momentum is expected to continue into early 2023, predicted DB. Both Europe and the U.S. are caught between a restrictive monetary policy that curbs both inflation and the economy and an expansive fiscal policy aimed at bolstering the economy and cushioning the effects of the current energy crisis, among other things, it noted.

For the Eurozone, this means that the ECB’s deposit rate is expected to increase to 3 percent during the course of the year, whereas Germany, for example, has planned fiscal measures equivalent to around 7.5 percent of its gross domestic product, stated DB. It is also expecting a mild recession overall in the Eurozone at the turn of the year. With recovery starting in the second quarter, economic growth for the full year 2023 is likely to be 0.3 percent, it said. The main risk factor remains energy, coupled with a possible shortage of gas in winter 2023/2024, added the bank.

Meanwhile, a soft landing is possible in the U.S. as well, with a marked economic slowdown so far not resulting in any significant increase in unemployment (and a still large number of unfilled vacancies), stated DB. Growing evidence of a slightly downward trend in inflation in the U.S. could see the Fed refocusing increasingly on economic growth, with further increases in the base rate likely to be smaller than in the recent past, it predicted.

However, it added that if inflation rates continue to decline and there is no need for robust Fed intervention, the U.S. economy could return to growth in the second half of 2023, finishing the year overall at +0.4 percent.

Also, economic momentum in China is likely to be much stronger next year and DB is expecting a growth of around 5 percent in 2023 after an estimated 3.3 percent this year.

Source: DB Report

First Published: 30 Dec 2022, 02:36 PM IST