Shares of Gulf Oil Lubricant India, India's 2nd-largest lubricant company after Castrol, are likely to surge 96 percent in the next 2 years, brokerage house Ventura Securities forecasted in its recent report.

The brokerage has initiated coverage on the stock with a target price of ₹813, indicating the aforementioned upside potential.

"At the CMP of INR 408, Gulf Oil's valuation at 0.3X FY26 PEG is one of the lowest among global peers and has the highest RoIC (36.4 percent FY26) along with the best domestic revenue growth potential. This makes it a significantly attractive business with a substantial margin of safety. Recently, the company initiated a buyback program, and the superlative prospective FCF (free cash flow) generation augurs well for more buybacks/enhanced dividend payouts. It is pertinent to mention that its current dividend yield of 1.23 percent also makes it a lucrative proposition," rationaled the brokerage.

Stock Price Trend

The stock has been completely flat in the last 1 year and is down 2 percent in 2023 YTD, despite giving positive returns in 3 of the 5 months so far of the current calendar year. The stock has advanced 1.8 percent in May so far after a 0.88 percent gain in April. However, it fell 2.5 percent and 4.2 percent in March and Feb, respectively. In Jan, the stock was up 2.4 percent.

Since hitting its all-time high of ₹1,025 in November 2017, the stock has been on a continuous downward trend and has lost around 60 percent of its investor wealth so far.

Earnings

In the December quarter, the company's net profit was up 7 percent YoY to ₹62.63 crore as against ₹58.63 crore in the year-ago period. Meanwhile, its revenue rose 30 percent YoY to ₹781.10 cr as against ₹601.82 in the same quarter last year.

Commenting on the performance, Ravi Chawla, Managing Director & CEO, Gulf Oil Lubricants India, said, “The continued all-round growth we have achieved in Q3, where the company has crossed ₹90 cr quarterly EBITDA mark for the first time in an environment of continued cost pressures for some of its key inputs and depreciating INR is due to the excellent team efforts and strong brand and business model that we have in place. We have delivered 3-4x of the market growth rate in volumes when demand conditions from segments related to rural like agri and 2W Oils were subdued.”

Investment Rationale

- Ventura noted that Gulf Oil has impressively gained market share and demonstrated resilience during the tumultuous past three years. It believes that the demand for lubricants is expected to surge due to the pick-up in the commercial vehicle (CV) cycle, improving freight movement on national highways, rising industrial output, and increasing sales of utility vehicles (UVs). These factors are expected to drive strong demand for lubricants from the B2B segment, which is responsible for generating 35-40 percent of Gulf Oil's lubricant & oil volumes, explained Ventura.

- Additionally, the brokerage stated that Guld Oil is proactively expanding its dealer network in new geographies to enhance the scope of its B2C lubricant business, which generates 60-65 percent of its lubricant and oil volumes at better margins compared to its B2B business.

- Overall, Gulf Oil's strategic efforts are expected to positively impact its market share and financial performance, further solidifying its position as a leading player in the Indian lubricant industry, it added.

- Along with its impressive growth in the lubricant industry, the company is also making strides in its battery business.

- By FY28E, the company is targeting a revenue of ₹200 cr, which represents a remarkable 2.3x increase over FY23 revenue, noted the report. The company plans to achieve this ambitious target mainly through cross-selling via its existing lubricant dealer network.

- Moreover, its launch of EV fluids is proving to be a smart move, as the company is reaping benefits from the high-growth EV market, said Ventura.

- Furthermore, the recent acquisitions of Indra Renewable Technologies and “ElectreeFi” have opened new doors for growth in the rapidly evolving EV charging space and its related ecosystem, it added.

Estimates

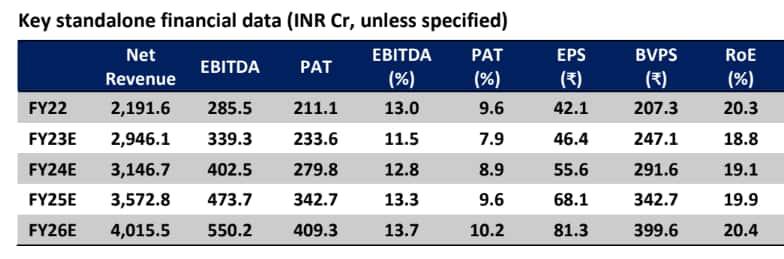

Over FY23-26E, Gulf Oil's lubricant & oil volumes are estimated to grow at a CAGR of 11 percent, while the company’s VRLA battery volumes are expected to grow at a CAGR of 20 percent, forecasted the brokerage.

It estimates the company’s revenue, EBITDA and PAT are expected to grow at a CAGR of 10.9 percent, 17.5 percent and 20.6 percent, respectively. Meanwhile, its EBITDA and PAT margins are expected to improve by 219bps to 13.7 percent and 226bps to 10.2 percent, it added.

Net cash balance sheet, industry-leading revenue growth, margin expansion and lower capex requirement is expected to generate strong FCF in the coming years. As a result, return ratios – RoE and RoIC – are expected to improve by 157bps to 20.4 percent and 773bps to 36.4 percent, respectively, further predicted Ventura.

"The company is in the high growth phase and the steep valuation discount of >30 percent to Castrol is unwarranted. We believe that as this growth story emanates, the valuation discount will narrow," said the brokerage.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.