As summer approaches and the temperature rises more than anticipated, stocks of air conditioner (AC) companies will be in focus amid rising demand for ACs. The India Meteorological Department (IMD) has also forecasted a strong summer, with 'above normal' temperatures across most parts of the country this year. This would be a boon for the AC industry, which traditionally does well during the summer months on the back of a surge in sales.

Voltas vs Blue Star: Which is a better AC stock for long term?

TL;DR.

As summer approaches, let's find out which between Voltas and Blue Star, presents better investment opportunities for the long term.

According to a report by brokerage house PhillipCapital, a rise in AC prices led to a fall in their volumes in the months of January and February but as the summer season began earlier than anticipated their volume increased in March amid stronger consumer mood.

With these stocks in focus, let's find out which between Voltas and Blue Star, presents better investment opportunities for the long term.

Stock Price Trend

While Blue Star has risen 28 percent in the last 1 year; this period has not been the best for Voltas. The stock has shed 37 percent in 1 year.

In 2023 YTD as well, Blue Star has emerged as a better performer, up 23 percent this year so far. Voltas, on the other hand, is also in the green, but up just 3 percent in 2023 till date.

This year, Blue Star has given positive returns in 3 of the 4 months. It has gained 6.8 percent in April so far after a 4 percent decline in March. Meanwhile, it surged 17 percent in February and 2.5 percent in January.

The trend remains the same for Voltas as well, advancing in 3 of 4 months this year but the quantum of the increase is less than that of Blue Star. In April, Voltas is up 0.6 percent so far after an 8.3 percent decline in March. In Jan and Feb, Voltas rose 11 percent and 0.3 percent, respectively.

Blue Star has given multi-bagger returns in the last 3 years. From its COVID-low of ₹408.90 (March 2020), Blue Star has skyrocketed over 260 percent to currently trade at ₹1,473.85 (as on April 13, 2023).

Voltas, on the other hand, has surged nearly 85 percent from its COVID low of ₹448.75, hit in March 2020, to currently trade at ₹823.50.

Blue Star hit its 52-wee high of ₹1,535.50, in March 2023 and its 52-week low of ₹860 in July 2022.

Meanwhile, Voltas hit its 52-week high of ₹1,317 in April 2022 and recently hit its 52-wee low of ₹737 in January this year.

About the firms

Blue Star Ltd is an Indian multinational home appliances company, headquartered in Mumbai. It specializes in air conditioning, commercial refrigeration and MEP (mechanical, electrical, plumbing and firefighting). It is the country's second-largest homegrown player in the air conditioning space. It was founded in 1943 by Mohan T Advani. Blue Star has a presence in 18 countries in the Middle East, Africa, SAARC and ASEAN regions. Blue Star has three Joint Ventures in Oman, Qatar and Malaysia. The company has subsidiaries in UAE, Qatar and India.

Voltas Limited is an Indian multinational home appliances and consumer electronics company headquartered in Mumbai. It designs, develops, manufactures and sells products including air conditioners, air coolers, refrigerators, washing machines, dishwashers, microwaves, air purifiers, and water dispensers. The company was incorporated on 6 September 1954 in Mumbai, as a collaboration between Tata Sons and Volkart Brothers.

Earnings

In the December quarter, Blue Star reported a 22.79 percent rise in consolidated net profit at ₹58.41 crore versus ₹47.57 crore in the same quarter last year. Its consolidated revenue from operations during the quarter under review was also up 18.7 percent to ₹1,788.2 crore as against ₹1,506.22 crore in the year-ago period.

"This is the fifth consecutive quarter of good performance, and we expect to maintain the growth momentum in the coming quarters as well," Blue Star Vice Chairman & Managing Director Vir S Advani said. Going ahead, Advani noted, "We will continue to stay focused on rejigging our product portfolio in line with customer preferences, deepening our distribution penetration in the domestic market and expansion of our footprint in international geographies."

In the December quarter, Voltas reported a consolidated net loss of ₹110.49 crore on account of provisioning made on overseas projects. The Tata Group firm had posted a consolidated net profit of ₹96.56 crore in the October-December quarter last fiscal. Its revenue from operations rose 11.82 percent to ₹2,005.61 crore in Q3FY23 as against ₹1,793.59 crore in the year-ago period.

"The profit was impacted due to provision of ₹137 crore (exceptional item) made on overseas projects," Voltas said in its earning statement.

Which is a better stock for the long term?

Vinit Bolinjkar, Head of Research - Ventura Securities believes Blue Star is better positioned compared to Voltas.

"Blue Star commissioned a new plant at Sri City. The timely start of operations at this plant was crucial for Blue Star, as it prevented the company from facing production constraints at its Himachal factory. The Sri City plant's strategic location near ports could also provide cost savings for Blue Star by reducing its working capital requirements. With the new plant in place, Blue Star is now well-positioned to serve its customers and meet their increasing demand," explained Bolinjkar. He also informed that management has targets to reach 15 percent market share by FY25 from the current 13.5 percent.

Blue Star’s MD Thiagarajan said. “Blue Star will look at investing in a compressor plant when we cross 1.5 million unit sales. Next year, we will cross one million and in another two to three years we should be there.” Blue Star trades at 55.2x TTM P/E, noted the market expert.

Meanwhile, for Voltas, he stated that the firm anticipates continued stiff competition in the room air conditioner (RAC) segment over the near term as peers appear to be aggressively chasing market share at the cost of margins. Consequently, management has ruled out a revival to double-digit EBIT margins in the near-to-medium term, he added. Voltas trades at 77x TTM P/E.

Khadija Mantri, Associate VP Research Analyst at Sharekhan by BNP Paribas also likes Blue Star over Voltas

"We like Blue Star given its strong performance in the last few years. Blue Star has a strong and growing market share of 13.25 percent in the room air conditioners (RAC) industry. The company hopes to increase its market share to 15 percent by FY25 by boosting penetration through its affordable and affordable premium range and broadening its distribution network. The company’s new RAC plant in Sri City would provide cost optimisation and reduce its inventory days. Thus, higher operating leverage based on the increase in volumes, backward integration in ACs as well as commercial refrigerators and exports shall lead to improvement in margins going forward," she rationaled.

On the contrary, Suman Bannerjee, CIO, Hedonova prefers Voltas over Blue Star.

According to Bannerjee, Voltas is growing faster than Blue Star in terms of revenue and profits and is trading at a lower valuation than Blue Star. Both companies experienced a significant drop in revenue due to the pandemic and lockdowns, but they were able to recover around 80-85 percent of pre-pandemic revenue on the back of strong demand for commercial products from the pharma and infrastructure industry.

He further pointed out that Voltas' revenue grew at a CAGR of 4.8 percent over the last five years, while Blue Star's revenue fell at a negative CAGR of 0.4 percent. He also added that Voltas' net profit grew at a CAGR of 1.8 percent over the last 5 years, while Blue Star's net profit saw a negative CAGR of 4.3 percent during the same period. Both companies' margins have been logging lower margins every passing year. Overall, Voltas seems to be a better pick for the long term, he said.

Nirav Karkera, Head of Research at Fisdom believes both Blue Star and Voltas have their unique strengths and challenges

Blue Star has emerged as a standout performer in the industry, displaying impressive revenue growth, maintaining its leadership position, and showcasing a forward-thinking approach toward innovation and operational excellence. On the other hand, Voltas has faced some challenges in recent quarters, including a decline in PAT and EBITDA, intensified competition, and rising input costs, he stated.

However, Voltas has a strong legacy of innovation with a robust product pipeline and distribution channel, which makes it well-equipped to overcome challenges and retain leadership, added the expert.

He further mentioned that while both operate in the same space and are largely driven by similar factors, the distinction in terms of business verticals and product mix contributes to a unique outlook for both stocks. While Blue Star can easily be expected to sustainably continue the growth trajectory, Voltas is well-positioned to stage a turnaround and recover a lot of lost grounds, said Karkera.

Karkera on Blue Star

Blue Star has emerged as a standout performer in the industry, displaying impressive revenue growth across segments. Blue Star witnessed a remarkable increase of 15 percent in Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) and a noteworthy 23 percent growth in Profit After Tax (PAT). The Blue Star stock has outpaced most close peers by returning over 20 percent in the last one year. It maintains leadership in Conventional and Inverter Ducted Air Conditioning Systems.

The company's mechanical projects and commercial air conditioning system segments have witnessed robust growth, and its foray into the railway electrification business has yielded significant orders. The overall order inflow and order book is growing at a fast pace as well.

Blue Star has sustained its growth momentum for the fifth consecutive quarter and looks committed to maintaining this trend in the coming quarters. The company's strategic focus on revamping its product portfolio, introducing new product categories, and expanding in domestic and international markets exemplifies its forward-thinking approach. Furthermore, Blue Star's investments in research and development capabilities and initiatives to mitigate supply chain risks and improve profitability demonstrate its commitment to innovation and operational excellence. Considering its unique positioning, the company holds strong promise.

Karkera on Voltas

The company's impressive product pipeline and robust distribution channel are expected to generate strong demand for its premium, higher-star-rated products. The margin has been under meaningful pressure for some time but the management seems committed to easing the same. The company is expected to work on margin expansion through value engineering and improved terms with suppliers.

However, amidst the promising outlook, there are challenges on the horizon. Intensifying competition from both domestic and international players poses a formidable threat to Voltas' market share while rising input costs cast a shadow over their short-term profitability. As Voltas faces these headwinds, strategic maneuvers will be crucial in navigating the competitive landscape and maintaining its leadership position.

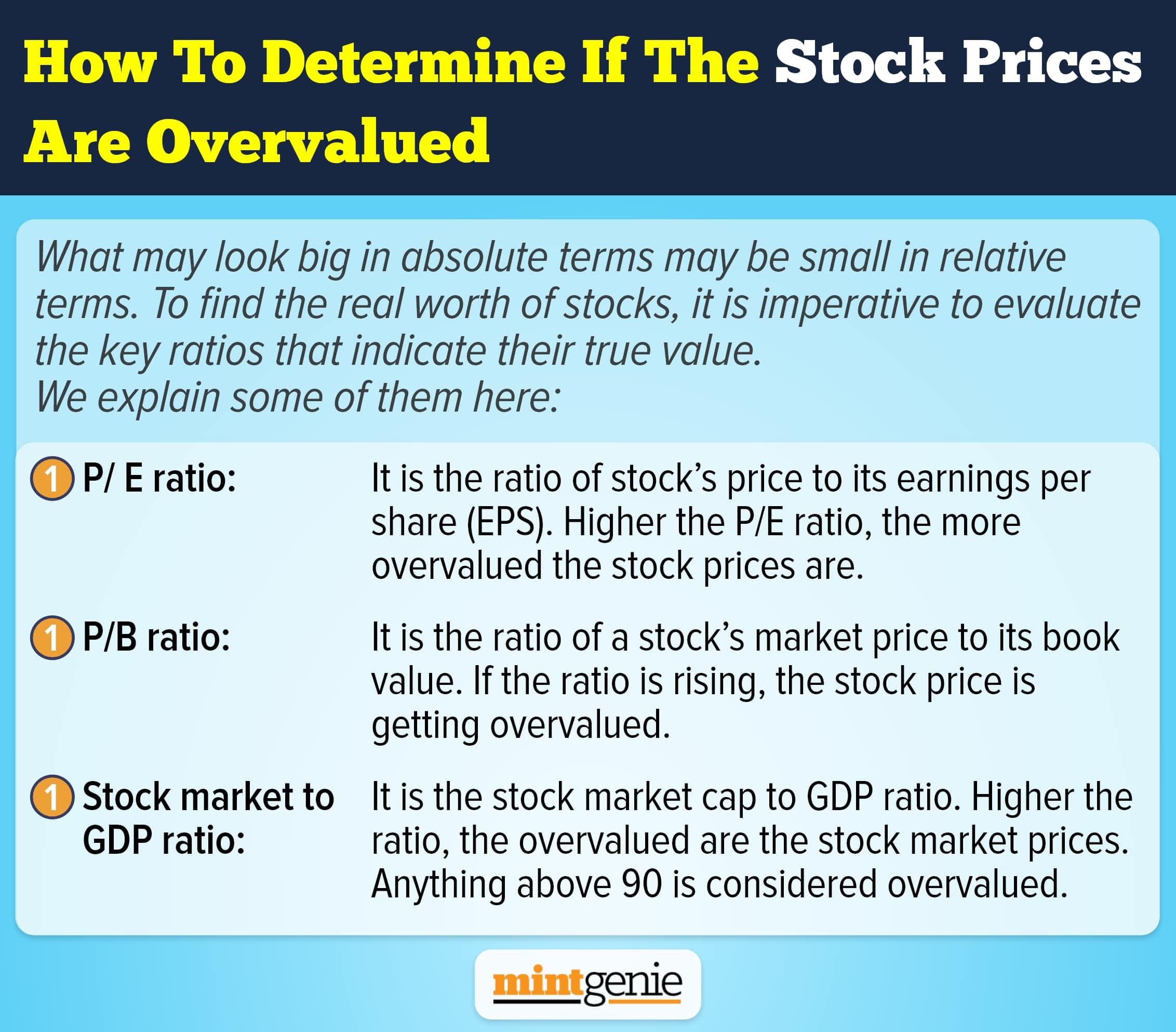

How to determine if the stock prices are overvalued.

First Published: 14 Apr 2023, 01:30 PM IST