Major domestic brokerage houses are bullish on the auto ancillary company Endurance Technologies after the firm posted better than expected numbers in the March quarter (Q4FY22). The stock has lost over 30 percent in the past 6 months and is down around 7 percent in the last 1 year.

Why brokerages are bullish on Endurance Technologies despite a 30% correction in last 6 months

TL;DR.

According to a report by Axis Securities, Endurance Tech reported a strong Q4FY22 performance primarily led by strong aftermarket sales, the addition of new products and improved realisations.

According to a report by Axis Securities, Endurance Tech reported a strong Q4FY22 performance primarily led by strong aftermarket sales, the addition of new products and improved realisations.

It stated that the firm's consolidated revenue stood at ₹2,079 crore versus the brokerage's estimate of ₹1,804 cr, up 10 percent QoQ. Meanwhile, EBIDTA came in at ₹257 crore as against Axis' estimate of ₹183 crore, up 27 percent QoQ. Meanwhile, its Q4 net profit was ₹136 crore. In comparison, the brokerage had an estimate of ₹71 crore.

Endurance Tech stock price trend

Axis noted that the improvement in earning numbers in the March quarter was due to positive operating leverage and cost savings exercises undertaken by the company supported by higher realisations.

The brokerage maintained a 'buy' rating on the stock with a target at ₹1,580 per share, indicating an upside of 27 percent for the stock.

Meanwhile, other brokerages like LKP Securities, Kotak Securities, and Choice Broking also have bullish views on the stock and expect an upside of between 10-26 percent in the stock.

LKP believes that a health order book remains the key. The standalone business has won orders worth ₹740 crore in FY22. In European operations, the company won orders worth EUR71.2 million mainly from Porsche, VW, Stellantis and New Holland during the year gone by, LKP pointed out.

"The quarterly and yearly numbers of Endurance were slightly subdued due to chip shortage and higher RM costs, but we believe the company will continue to outperform the industry led by (1) expectations of improvement in 2W demand over FY23 (after two dismal years), led by strong underlying trends for scooterization and premiumization (2) addition of new and value-added products, (3) ramp-up in EV products and (5) increasing share of aftermarkets and exports," highlighted the brokerage.

It added that the strength in Endurance’s business franchisee and experienced management should help the stock to continue commanding premium valuation multiples in comparison to most domestic

auto ancillary companies. There are only a handful of high-quality, large-scale, multi-product auto component suppliers and considering Endurance’s size and strong market share in its operating segments, the stock should command a premium to its domestic peers, said LKP. It has a 'buy' call on the stock with a target at ₹1,637, indicating an upside of 26 percent.

Meanwhile, Kotak Securities noted that while the near-term may remain challenging given supply-chain constraints and cost pressures, especially in EU operations, however, it expects the company to outperform the domestic two-wheeler industry mainly led by new order wins across product segments. Stock price correction by 30 percent over the past six months provides a good opportunity to enter this name, it added. It has a target price of ₹1,320 for the stock, indicating an upside of around 10 percent.

Further, Choice broking believed that Endurance's growth story depends upon an increase in two-wheeler component content, new orders, pick up in orders from H2-FY23E from existing global OEM clients, and introduction of new product Driveshaft and BMS, and finally, demand for alloy wheels.

Choice also sees the firm's performance to be muted in the near term due to the semiconductor shortage impacting the offtake by OEMs and higher RM and energy costs impacting the European performance. However, it believes going forward pick-up in domestic two-wheeler demand and easing out of semiconductors will help Endurance to achieve healthy earning growth over FY23-24. It has a target price of ₹1,406 and recommends 'add' rating for the stock.

"Endurance offers strong management, a diverse revenue profile, improved technological content, increased wallet share of customers, and financial discipline. The share of EV/Hybrid technology is expected to increase in the near future as the demand in Europe shifts towards less polluting vehicles to reduce carbon footprint," said Axis. In this backdrop, it estimates consolidated Revenue/EBITDA/PAT to deliver a CAGR of 14 percent/25 percent/29 percent over FY22-24E.

Recovery in the underlying 2W demand, improvement in the EU business from Q2FY23E, and the possibility of new product technology are potential catalysts for the stock, Axis added.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

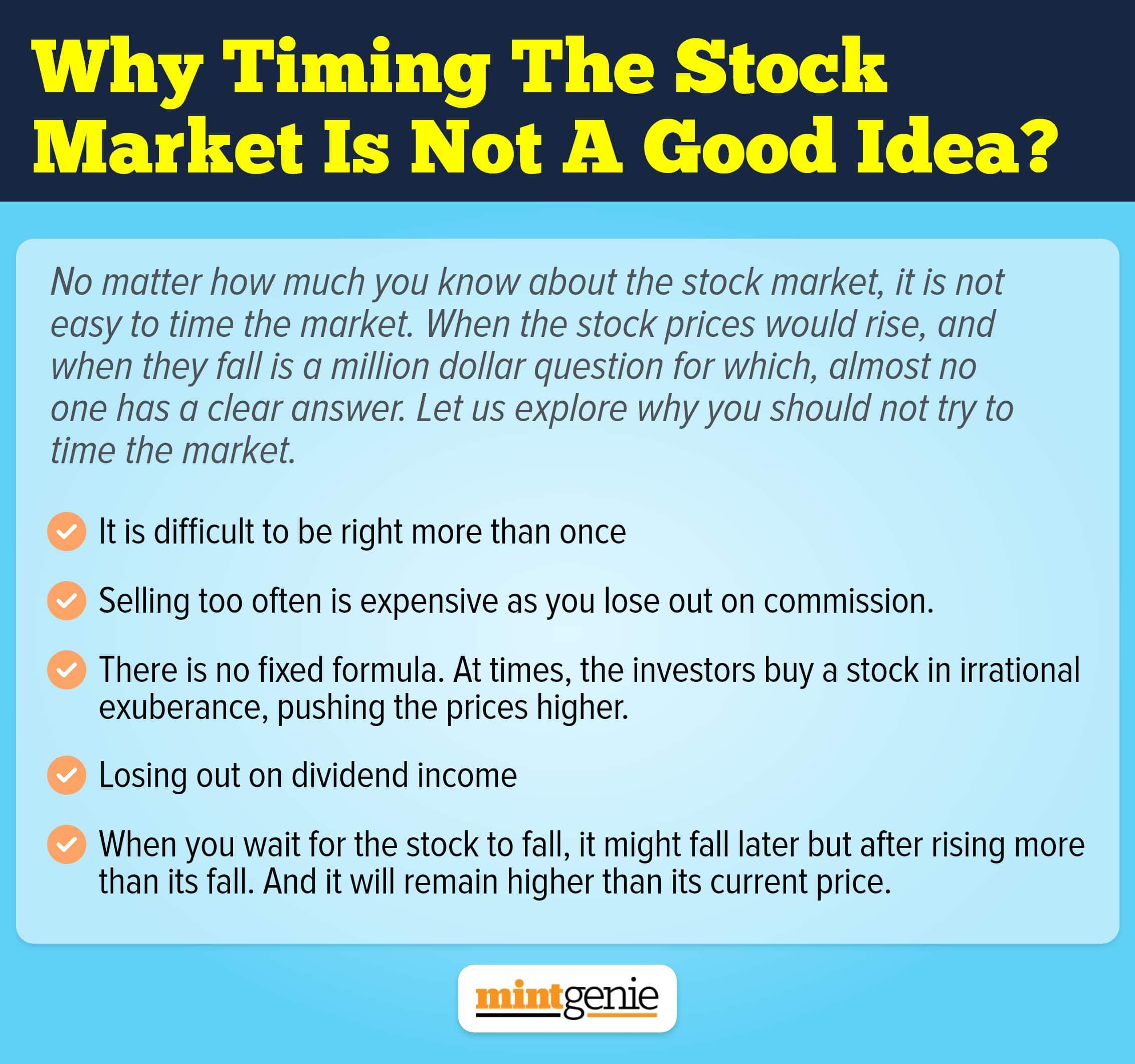

We explain why timing the stock market is not a good idea.

First Published: 24 May 2022, 01:24 PM IST

Related Stories

Explain Like I am 5

personal finance

Mutual fund investors not-so-keen for equity schemes, April data shows

Team MintGenie