Brokerage house Elara Capital has initiated coverage on the ethnic wear segment. the brokerage believes that India Ethnic Wear, which forms 32 percent of the apparel market, seems tailored to grow, led by the branded segment.

A confluence of tailwinds including increased penetration in tier II/III cities, rising preference for brands (better quality/style), and improved spending ability given rising incomes – may lead to growth, noted the brokerage. It further informed that Branded Celebration Wear is set to post an 18-20 percent CAGR to ₹37,100 crore size in FY25 and Branded Bottom Wear 20.5 percent CAGR in FY20-25 to ₹24,300 crore size in FY25, as per Vedant Fashions’ (MANYAVAR) and Go Fashions (GOCOLORS).

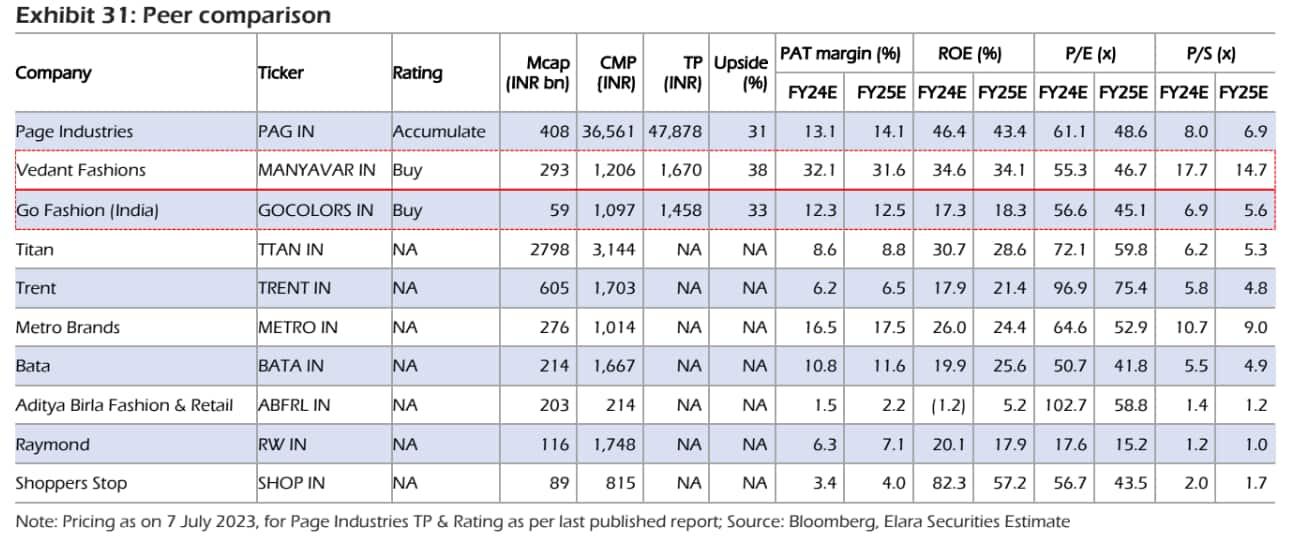

The brokerage expects that such high double-digit growth may offer brand pioneers, MANYAVAR and GOCOLORS a huge growth window in existing/new markets, led by brand recall.

Amid this backdrop, the brokerage has initiated coverage on both stocks with buy calls. It has a target price of ₹1,670 for Manyavar, indicating an almost 35 percent potential upside. Meanwhile, for Go Fashion, Elara has a target price of ₹1,458, implying a potential upside of around 29 percent.

Valuations

As per the brokerage, both stocks may be in a position to withstand increasing competition and maintain market leadership, led by aggressive store expansion, proven business models with healthy store dynamics, and robust supply chain networks.

It expects MANYAVAR’s/GOCOLORS' revenue CAGRs at 21.1 percent/25.7 percent in FY23-25E. Downside risks to its growth estimates are slower-than-expected store expansion, lower SSG, and adverse impact of competition on growth, cautioned the brokerage.

Industry Overview

Elara believes that the ethnic wear segment may add ₹60,000 crore in market size through FY20-25, 40 percent of which may be from Branded Celebration Wear. Also, Branded Bottomwear may add ₹6,910 crore in FY20-25 in market size. Thus, existing players – MANYAVAR/GOCOLORS and even new entrants have ample room to expand/create a niche, it stated.

It also pointed out that large conglomerates – Reliance Retail (Ambani Group), Aditya Birla and Fashion Retail (Aditya Birla Group), Titan/Trent (Tata Group), and Ethnix (Raymond Group) – are competing aggressively to gain a slice of India Retail. Ethnic Wear, being at a nascent stage, is an attractive domain with high, double-digit growth potential. Elara believes that a strong balance sheet (net debt free) as also an established supply chain network of more than a decade should fuel growth for brand pioneers against the intensifying competition.

Despite such major players entering the ethnic wear space, the brokerage has coverage on only 3 stocks. Apart from Manyavar and Go Fashios, it has an accumulate call on Page Industries with a target price of ₹47,878, indicating a potential upside of almost 31 percent.

Stocks

Vedant Fashions: The brokerage favors Manyavar given its market leadership, a wide portfolio of brands, superior profitability, and command of the supply chain. Expansion of other brands – Twamev, Mohey, and Manthan – may trigger the next leg of growth and boost profitability, it added. The brokerage expects MANYAVAR’s retail space to grow at 11.3 percent CAGR over FY23-25E.

It also sees MANYAVAR generating a free cash flow (FCF) of ₹1,290 crore cumulatively in FY23-25E, on higher operating cash flows and minimal capex led by franchise-driven expansion. MANYAVAR’s earnings CAGR maybe 21 percent in FY23-25E, as revenue growth percolates to its bottom line, it stated.

"MANYAVAR is well poised to leverage its strong brand recall and geographic presence by cross-selling Twamev/Mohey brands in its large flagship stores. Twamev caters to affluent clients in men’s celebration wear and Mohey to Women’s Celebration Wear. Manthan caters to a large online mass segment. Expect new brands to spike their revenue share 170bps in FY23-25E to reach 16.8 percent in FY25 cumulatively," said Elara. A robust supply chain, focus on design innovation, growth acceleration via penetration/channel expansion, and strong store economics – seem promising, it added.

Go Fashion: The brokerage expects GOCOLORS to withstand intensifying competition and maintain its market leadership, led by aggressive store expansion, a proven business model, and healthy store dynamics. It estimates FY23-25E revenue/PAT CAGRs of 25.7 percent/25.9 percent.

"GOCOLORS is net debt free, despite Corporation Owned Corporation Operated (COCO)-based exclusive brand outlet (EBO) expansion. Working capital days are improving, after worsening during COVID as the channel mix improves, tilting to EBO. It expects GOCOLORS to generate FCF of INR 3.5bn cumulatively in FY24E-25E. No leverage, strong FCF generation and robust store dynamics offer strength to the balance sheet despite COCO-based EBO expansion," it mentioned.

It sees GOCOLORS opening 120 stores each year over FY23-25E, at a 17.5 percent CAGR and FY24E/25E same-store-sales growth (SSSG) of 14 percent/12 percent.

The brokerage also pointed out that GOCOLORS operates at an EBITDA margin (post-IND-AS) of 31.9 percent, led by a 73 percent revenue share of EBO and 95 percent of sales on full price. With rapid EBO expansion in the near term, it expects the revenue share from EBOs to spike to 77.3 percent in FY25E. This may likely improve working capital days efficiency and sustain higher margins in an intensely competitive market, it said. In FY25E, Elara expects EBITDA margin to touch 32 percent and ROE to improve to 19 percent.

Stock Price Trends

While Manyavar has gained over 12 percent in the last 1 year, Go Fashion has advanced over 15 percent in the same period.

However, just in 2023 YTD, Manyavar is down 6 percent whereas Go Fashion has lost 5.6 percent. Both Manyavar and Go Fashion have given positive returns in 4 of the 7 months in the current calendar year.

Manyavar has gained the most in April this year, surging 11.6 percent while shedding the most in January, down 10.9 percent. Go, on the other hand, has rallied the most in March, up 9.5 percent and declined the most in January, down 13.3 percent.