For the quarter ended December, Zee Entertainment Enterprises Ltd's consolidated net profit fell by 92% on a year-on-year basis to ₹24.32 crore from ₹298.98 crore, due to rising content costs and investments in its OTT platform.

The company's total income for October-December was slightly lower at ₹2,127.23 crore as against ₹2,130.44 crore in the corresponding quarter.

The challenging macroeconomic environment is still having an effect on the media organisation's operating performance, the company stated in an exchange filing on Monday, February 13.

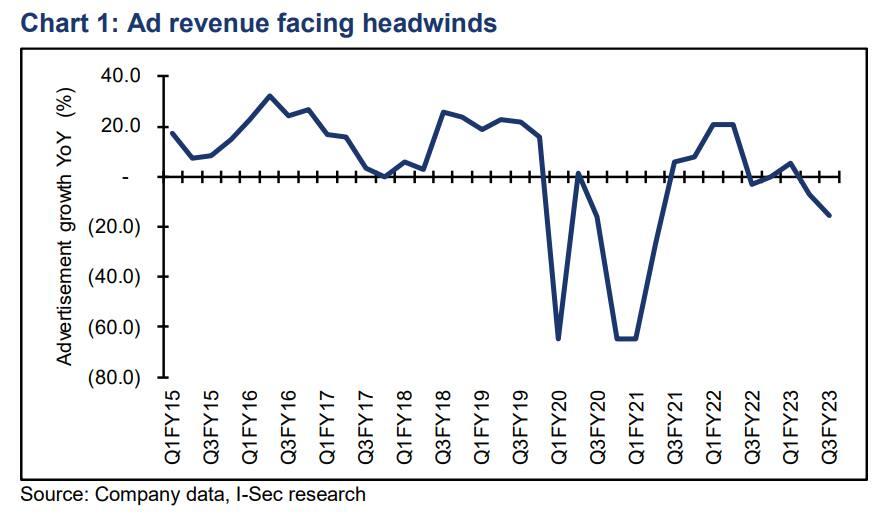

The company's revenue from advertisement fell 15.62% at ₹1,063.82 crore in Q3FY23. It was ₹1,260.80 crore in the same quarter a year ago. The company's total expenses rose by 10.03% to ₹1,871.81 crore during Q3FY23.

Brokerage Nuvama Wealth Management Ltd in its report stated that it expects the company to reap the benefits once ad-spends revive in Q4FY23 estimates (E).

The brokerage said that it liked the fact that Zee5 recorded its highest-ever daily active users (DAUs), which reflected persistence.

Another element the brokerage was delighted to see was that Zee Music Company’s Hindi movies acquisition share improved to 50% (from 42% in FY22), and it is the second-largest music label with 92 million subscribers on YouTube.

"50+ shows and movies (including six originals) were released on ZEE5 during Q3. The company continues to gain network shares in the south cluster and further strengthen its position. Strong usage seen in the digital business with higher engagement evident in an increase in monthly active users (MAU)/DAU and watch minutes," added the brokerage.

However, the brokerage was disappointed with October-December's fall in profit after taxes (PAT) due to exceptional items pertaining to revenue recognition of Siti Networks Ltd, impairment of non-convertible debentures (NCDs) from Zee Learn, merger-related costs, and provision for Debt Service Reserve Account (DSRA).

When the cash flow available to pay off debt is insufficient, the debt service reserve account (DSRA) is utilised to make repayments on the loan.

The brokerage retains 'buy' rating on the stock and reduces the target price by 12% at ₹325.

Brokerage ICICI Securities Ltd in its report said that the company's Q3FY23 revenue was muted on account of subdued demand environment as fast-moving consumer goods (FMCG) companies kept ad-spends under control to counter raw material inflation.

"As the company continued to invest in content creation, earnings before interest, taxes, depreciation, and amortization (EBITDA) declined 29.5% on year. Multiple one-offs and exceptional items impacted net profit (down 92% on year). We have cut our earnings estimates by around 14% for FY24E and our target price by nearly 15%. We maintain 'hold' rating on the stock.

Further, the brokerage believes that the merger with Sony is likely to be the most important focus area for investors in the near term.

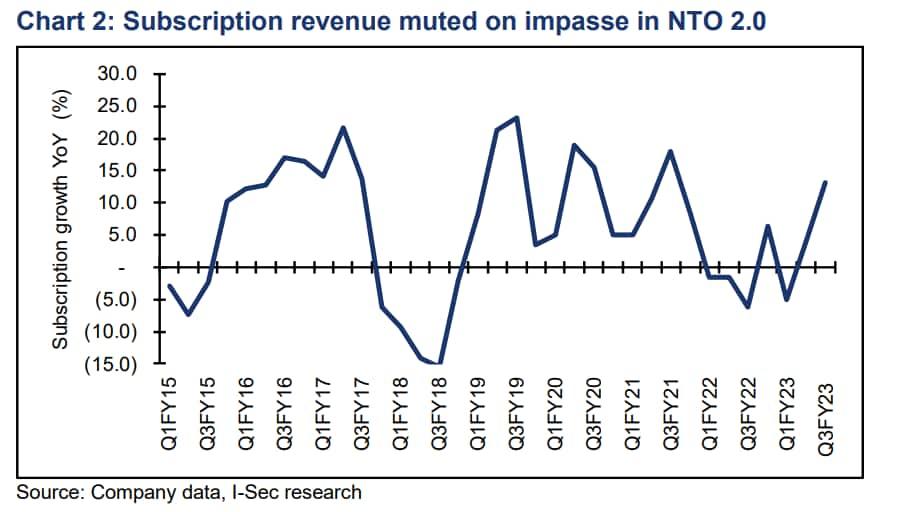

According to the brokerage report, the overall ad revenue was down 15.6% year-on-year (YoY) to ₹1,060 crore with domestic ad revenue declining 15.8% YoY to ₹1,019 crore. Subscription revenue rose 13.2% YoY to ₹890 crore. Domestic subscription revenue grew 11.2% YoY while international revenue grew 30.7% YoY. Subscription revenue was aided by organic growth in ZEE5 and ₹49 crore from SITI network.

Kotak Institutional Equities Ltd brokerage expects core business outlook to improve marginally in FY2024.

"TV Adex could grow in DD (off a low base), as inflation eases and advertisers increase ad budgets and the ongoing new tariff order (NTO) 2.0 implementation drives HSD growth in domestic subscription revenues. This, along with merger synergies of Rs6-6.5 bn over 12-18 months and more efficient capital allocation, could augur well. A one-time write-off of inventory (if any) can reduce movie amortisation expenses, boosting EBITDA by about Rs3-4 bn/year," said the brokerage in its report.

The brokerage has recommended 'add' rating for the stock, and reduced the fair value to ₹255 from ₹300.