It is widely believed that learning from others' mistakes is the best way of growing in life, instead of gaining knowledge from making mistakes. Money management is a skill that has to be dealt with carefully. In the case of a bit of mismanagement, the probability of being financially indebted might be the most likely situation.

Here are majorly five mistakes that individuals make while managing their personal finances which you must avoid before you start earning money:

Directly start investing

We must pay attention to the fact that the beginning of financial management starts from budgeting rather than from investing. But, the mistake many individuals usually make is they directly jump up to investing and might end up losing money. Now, you need to start personal financial management step by step by creating a budget for your expenses by writing down each payment in a month and tracking it down at every month's end.

Spending plan before saving plan

Many of you think that crafting a budget means planning expenses, which is the biggest mistake in financial life. The aim of budgeting is to start increasing the saving portion of your income, so focusing on saving rather than spending might be a better idea. Spend what you left instead of saving what is left at the end of the month.

Meeting debt with investments or savings

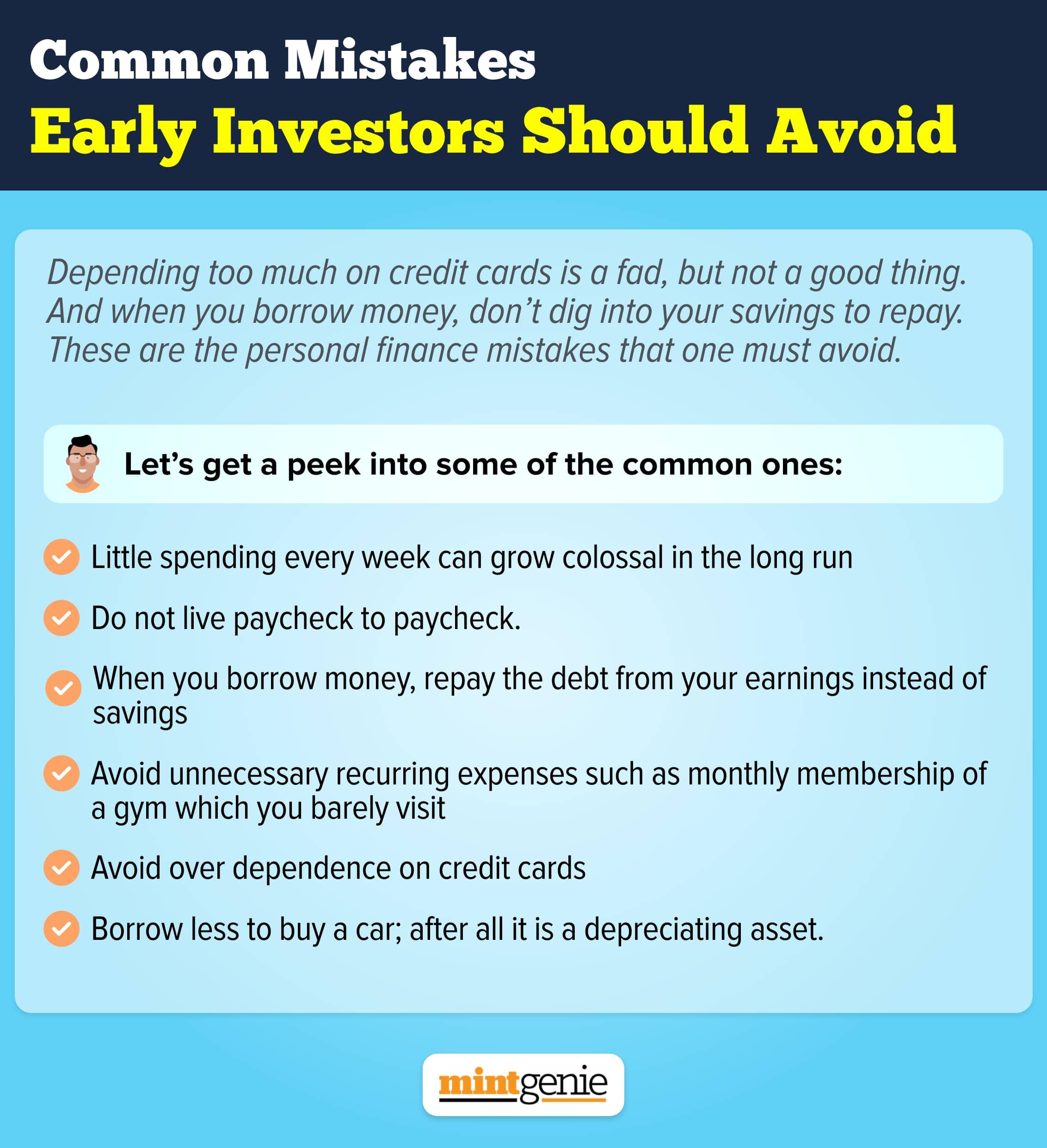

Many individuals might have a complaint of not having a single penny at the month end. You might have to pay EMI by utilising savings or investments in times of emergencies or financial crunch. Always remember that debt should not exceed 30% of your net income or any other ratio which is manageable during the financial crisis.

Buying liabilities

Rich are becoming richer, and the poor are becoming poor only because of the habit of spending. Rich people buy assets and earn passive income from the same. On the other hand, you might buy things to please society, not corresponding to the financial returns of such an expense. You should also start spending on what gives you returns, instead of living in the illusion of peace.

Not having an insurance plan

An insurance plan, whether for health or life, is a blessing not only for the financial stability at tough times but also for saving taxes. Various individuals consider insurance a waste of money as the covid-19 pandemic is proof that having health insurance will help you assist financially whenever it is required and motivate you to be healthy.

Buying insurance is not a waste of money, but it is a way of saving tax and protecting you and your family from uncertainties by letting the claim do their work in the case of sudden demise, health emergency, accident, etc.

Conclusion

Personal financial management is vital in moving towards a happy and peaceful life. Paying attention to money management and learning about the basics of money additionally will help you in mastering the personal finances. You can start by avoiding the above-mentioned mistakes and making reasonable financial decisions while sitting with your family.

Anushka Trivedi is a freelance financial content writer. She can be reached at anushkatrivedi.com