There is no valid reason for you not to plan your retirement. After all, the money will be used to fund the golden years of your life. Many people complain about how they are lagging behind in terms of retirement planning. Most people attribute their delayed retirement planning to ignorance while others are blissfully unaware of how the depreciating value of money is gradually eating into their savings and fixed deposits. You may have started late saving for your retirement.

5 moves late starters can pursue to ensure a smooth retirement

TL;DR.

Planning for retirement may be difficult, especially, if you start out late. However, if you follow the fundamental rules of financial management, retirement planning may appear less daunting than expected.

Nevertheless, it is better to start late than never though it may be overwhelming considering how it is difficult to make up for the lost time. Also, increasing age poses new and unforeseen constraints when saving money to secure the future.

Assume that you are 35 years old, which means that you have 25 more years to save for your retirement. Though you started out late, you still have the benefit of having time on your side as opposed to many people riddled with debt and planning their retirement much later in their lives. With 25 more years to compound your investments, all you have to do is to start so as to secure enough by the time you have stopped working.

While it may sound easy, planning for retirement has never been easy, especially, for those new to personal finance or completely ignorant of the available investment opportunities. Also, many people tend to procrastinate when it comes to money decisions despite having a comfortable income. Delayed financial decisions can affect your financial situation and might cost you an opportunity to create the much-desired corpus.

Seeking a personal finance advisor’s intervention would do much good in helping you understand where you stand and your potential financial condition a few years from now. Before you rush in to plan your retirement, you must focus on certain aspects. These include:

Know your financial condition

Have you saved enough for your retirement? Which of your assets could serve as potential sources of income post-retirement depends on how much you have saved already and how much more you must save. To assess your financial condition, you must first check the balance amount in your

- Savings accounts

- Bank deposits including fixed and recurring deposits

- Pension plans running in your name

- Real estate investments such as shops, flats or house

- Gold purchases or investments

- Insurance policies such as health insurance, endowment plans, and more.

Know how much you need

Your idea of financial independence may be different from what your peers or friends think. This is why you must have your retirement plan instead of aping others. Knowing how much you will need after retirement or your potential expenses will help you decide which investment opportunities will provide you with the best returns.

For example, if you are looking to earn good returns, you might as well invest in equities though the risk involved is too high. Step up your investments with time to ease your journey towards your financial goals. Though many advise a 10 per cent annual step up, financial experts express how one must invest more to earn more in the long run. This also means putting your yearly bonuses and regular appraisals into the investments instead of wasting them on fancy gadgets or making unwarranted expenses.

You may also start by parking a part of your earnings in a retirement plan or in the government-sponsored National Pension Scheme (NPS) that allows investors to put their money in a bunch of options including both equities and debt. The risk-averse may opt for debt funds though they may not fetch returns unless held for a prolonged period, say for the next 20-25 years.

How much you save for retirement also depends a lot on your current lifestyle expenses. These expenses are set to rise with time, which means that you must save more to ensure the same lifestyle post-retirement too. This includes any outstanding loan(s) or medical expenses despite purchasing a health insurance policy.

Get rid of unnecessary expenses

Whoever said, “A penny saved is a penny earned” was not completely wrong. A few bucks saved here and there can get a long way in saving that extra amount and then investing it for future returns. This is especially true of millennials who rely on credit cards to make their purchases. Those looking for immediate gratification tend to forget that they have to repay the amount one way or the other. Also, delayed credit card repayment begets a penalty, thus, adding more to your expenses.

Every time you feel the urge to buy something you can do without, think of how you can use this money to grow your wealth in the future. For example, if you spend ₹1000 on a movie ticket and pizza dining every month, estimate how saving this money and investing this amount through regular systematic investment plans (SIPs) every month in an equity fund that earns roughly 12 per cent returns will help you amass a decent corpus after 25 years.

Monthly SIP: ₹1000

Estimated return rate: 12%

Investment tenure: 25 years

translates to

Invested amount: ₹3,00,000

Estimated returns: ₹15,97,635

The total value of the returns: ₹18,97,635

Spending is a chronic habit that has destroyed the scope of many to amass much-needed wealth. There are many ways in which you can curb your spending habits. All you must do is try to make a start; better if you can envision your possible future sans proper retirement savings.

Seek professional advice

The misplaced attitude of knowing well has done more harm than good to many people, especially, those who relied solely on tips on social media channels to decide their investments. You cannot arrange your investment portfolio without the assistance of a professional financial advisor. More than how much money you are willing to invest, the advisor will guide you on how much you must invest and where to invest with changing times and shifting financial goals.

Advisors do more than just screen through possible investment opportunities to park your earnings. They help you with ideas for developing the much-needed financial strategy. For example, many investors depend on government policies and investment options to create wealth. These include fixed and recurring deposits, buying National Savings Certificates (NSCs), post office deposits and low-cost pension schemes. While there is nothing wrong with these investments, will they help in gaining your intended retirement corpus?

Advisors help you choose among the numerous government policies and then decide on a proper mix of investments that include both equity-backed and government-backed policies. Also, the advisor will tell you which government policy to invest in depending on your investment tenure and the kinds of benefits you are probably looking for.

Many people are afraid of approaching advisors fearing the added expenses on their charges. What they do not realize is that these advisors charge for their expertise and experience. Financial advisors serve as an anchor to your investments by telling you when to start, stop and shuffle your investments as opposed to finfluencers involved in paid marketing of certain investment products that may do you no good in the long run.

The compounding effect

Have you ever wondered how your money grows? Of course, money does not grow on trees. It is the interest component that helps your investments grow. You earn interest on your investments so that the total amount (original investment + interest) serves as the new investment amount. You then earn interest on this new investment amount which is higher than the original investment. If the investment is of a recurring nature or something that involves regular infusion of money through SIPs, your investment amount grows along with the interest amount.

This way, you can work on your long-term investments to see your cash grow. What you need to keep the money growing is regular, sizeable investments from time to time and then earn your interest on them. A modest contribution, say ₹10,000 every month at 12 per cent returns for 25 years can grow into a sizeable corpus of ₹1,89,76,351.

Some companies combine investments with insurance, for example, unit-linked insurance plans (ULIPs), thus, allowing you to benefit from the insurance component while seeing your money grow with time. Though investments must not be combined with insurance with the latter occupying a separate and distinct space in your investment portfolio, investing in a ULIP for at least 20 years can help your money grow. However, you must be aware of associated expenses like management charges, switching charges, administrative charges and so on before putting your money in your choice of ULIP.

One way out is to buy a separate term insurance policy with an adequate insurance amount that would serve your loved one’s financial needs in your absence. Once you have bought a pure term insurance plan, you can move on to investing your money in other options such as SIP and lump sum investments in equities, a bit in debt funds, some emergency corpus into liquid funds, some gold investments and the remaining into real estate depending on what kind of house you are looking for.

With both insurance and investments to achieve your financial goals, you are not left with much to decide your retirement goals. All you must do is remain persistent towards your achievements to enable create the retirement corpus that you had planned at the beginning of your investing journey.

Save and invest

When it comes to dealing with money, nothing serves better than saving and investing it. It does not make sense if you just save your money for the interest on your savings account will do nothing to increase it. In fact, the depreciating value of money and the continued impact of inflation will only cause your savings to lose their value in the long run.

You cannot obviously start investing unless you have saved enough, which means the latter is a prerequisite to the former. One of the necessary requirements in planning your retirement corpus is to start saving immediately. Though this could be a challenging behaviour, given the rising costs of living and your responsibilities towards your family, saving is a must. You must cultivate the habit to save and invest first before deciding how much to spend. Spend only a percentage of what you make so that you do not regret losing out on your earnings during your investment journey.

The money you have today is definitely not enough for you to meet your survival needs tomorrow. This makes savings more critical. To ensure that your retirement plans are in place, you must continue to save and invest.

It is okay if you have started out late. What matters is that you have decided to take the first step to secure finances for your old age. It is your duty to ensure that your retirement is free of financial worries. This explains the need for you to start planning for your retirement now.

Whether you are salaried or self-employed, the basic tenets of saving and investment remain the same. This means that you can start investing at any age, irrespective of when you start. This also means that saving regularly will keep you in good stead as opposed to those who recommend fancy investments only to lose their money in the end. It also means that saving money is futile without you investing money as much as the latter is impossible without the former.

Your retirement is synonymous with a lack of access to regular income. It also implies that you would be planning to spend your time pursuing your hobbies and passions left unattended to date. However, this necessitates money which is possible only by planning and accumulating an adequate retirement corpus.

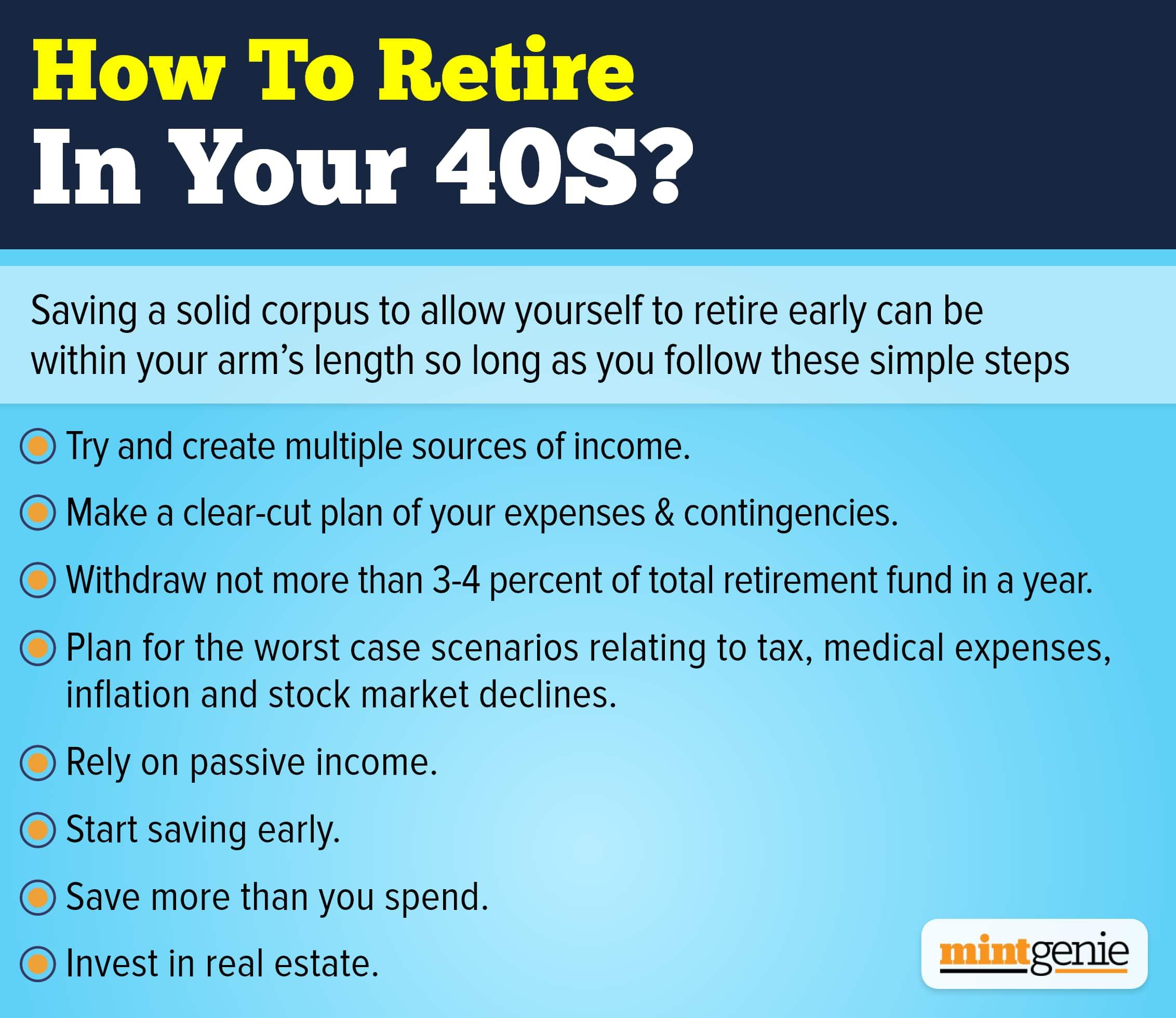

We explain how to retire in your 40s

First Published: 11 Nov 2022, 11:14 AM IST

Related Stories

personal finance

How to plan your investments for a regular income flow after retirement? Here are 3 steps

Abeer Ray