In 2022, for the first time in more than 50 years, global equities and bonds both delivered negative returns, prompting many market experts to declare the death of the traditional “60/40 portfolio”. Even before 2022, the combination of historically low bond yields and robust equity returns had provoked investors to doubt the necessity of including bonds in their portfolios. However, apprehension about potential market volatility due to the global growth slowdown and the rise in bond yields following interest rate hikes has led investors to review the role of bonds once again in their portfolios.

Stepping away from the current market context, a broader question arises: should long-term bonds consistently hold a place in investment portfolios across the diverse cycles of the market?

In 1952, the Noble Laureate Harry Markowitz first introduced the concept of a 60/40 portfolio, a blend of 60% equity and 40% bonds, as a long-term investment strategy. Since then, the 60/40 portfolio model has served as a guiding principle for countless investors seeking to optimise returns while mitigating risk.

Stabilising Portfolio

As we're aware, equities possess the potential for robust returns, but they also carry the inherent risk of volatility and sharp corrections. In contrast, bonds can stabilise portfolios, particularly during periods of equity volatility. Let's look at some data to better understand this.

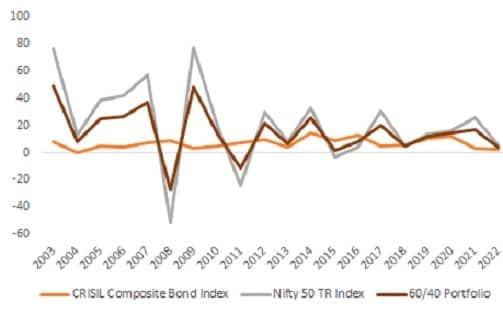

A glance at the data reveals that equities, represented by the Nifty 50 index, have yielded staggering returns exceeding 75% in select years but have also declined more than 50% as observed in 2008. Over the past two decades, equities have delivered an average annual return of 20.8%. On the other hand, bonds, represented by the Crisil Composite Bond Fund Index, have encountered only four instances of negative return within the same timeframe. Notably, the sole decline was a modest 0.33% dip observed in 2004. The historical average annual return for bonds stands at 6.8% over the last two decades. For a more precise measure of volatility, let's look at the standard deviation of calendar year returns. In the case of Nifty, the number is 29.6% while for Crisil Composite Bond Fund Index it is 3.7%

A 60/40 portfolio rebalanced annually has delivered average annual returns of a healthy 15.2% with a standard deviation of 17.6% with a max loss of 27% in 2008.

Calendar year returns of Equities, Bonds and 60/40 Portfolio

Protection During Downturns

Even for investors with a long-term horizon and the capacity to endure short-term volatility, allocating a portion of their portfolio to bonds can prove beneficial. Typically, after a significant market correction, equities often experience robust rebounds. However, in an unfortunate scenario where the need for funds coincides with a market downturn, investors might find themselves compelled to withdraw from equities at possibly the worst time. In such circumstances, bonds can prove to be a valuable cushion.

Regular Stream of Income

In addition to providing stability to the portfolio, bonds also generate a consistent stream of income. These fixed payments from bonds can provide investors with a reliable source of income throughout the investment. The predictable income can provide a sense of financial security and may specifically appeal to retirees and individuals who seek to cover living expenses or achieve other financial objectives.

Short-Term vs Long-Term Bonds

Let's now examine the comparison between short-term and long-term bonds. Typically, bonds maturing within 3-4 years are deemed short-term, while those maturing beyond 7 years are considered long-term. Due to the extended lending period, longer-term bonds offer higher yields and returns but are more influenced by changing interest rates. Falling rates raise long-term bond values, potentially leading to capital gains, while rising rates can decrease their value. The gain/loss in value is more pronounced for long-term bonds than short-term bonds.

Current Market Context

Over the last year or so, most global central banks have responded to elevated inflation by raising interest rates. Consequently, bond yields have surged. Even in India, the RBI has implemented a 2.5% increase in policy rates since May 2022. As a result, the yield on India's 10-year government bonds has climbed to approximately 7.2%, compared to the sub-6% levels observed in 2020. It appears that both the US Federal Reserve and the RBI might not pursue further rate hikes, implying that bond yields could have reached their peak. Moreover, the delayed impact of these rate hikes on global economic growth is yet to materialise. The potential global growth slowdown raises the prospect of volatility in global equities. In this prevailing scenario, characterised by attractive bond yields and expectations of impending market volatility, bonds could potentially stabilise portfolios. Furthermore, as and when we start seeing rate cuts we could see some capital appreciation in long-term bonds, however, that may still be a few months away.

In Conclusion

Although we have used the 60/40 portfolio as a reference, the precise allocation to bonds depends on multiple factors, including risk-return expectations, liquidity requirements, time horizon, tax considerations and specific restrictions/stipulations. However, bonds should be part of all investor portfolios irrespective of market cycles. Investors may look to adjust their bond allocations in response to the prevailing market environment.

Alekh Yadav is Head of Investment Products, Sanctum Wealth.