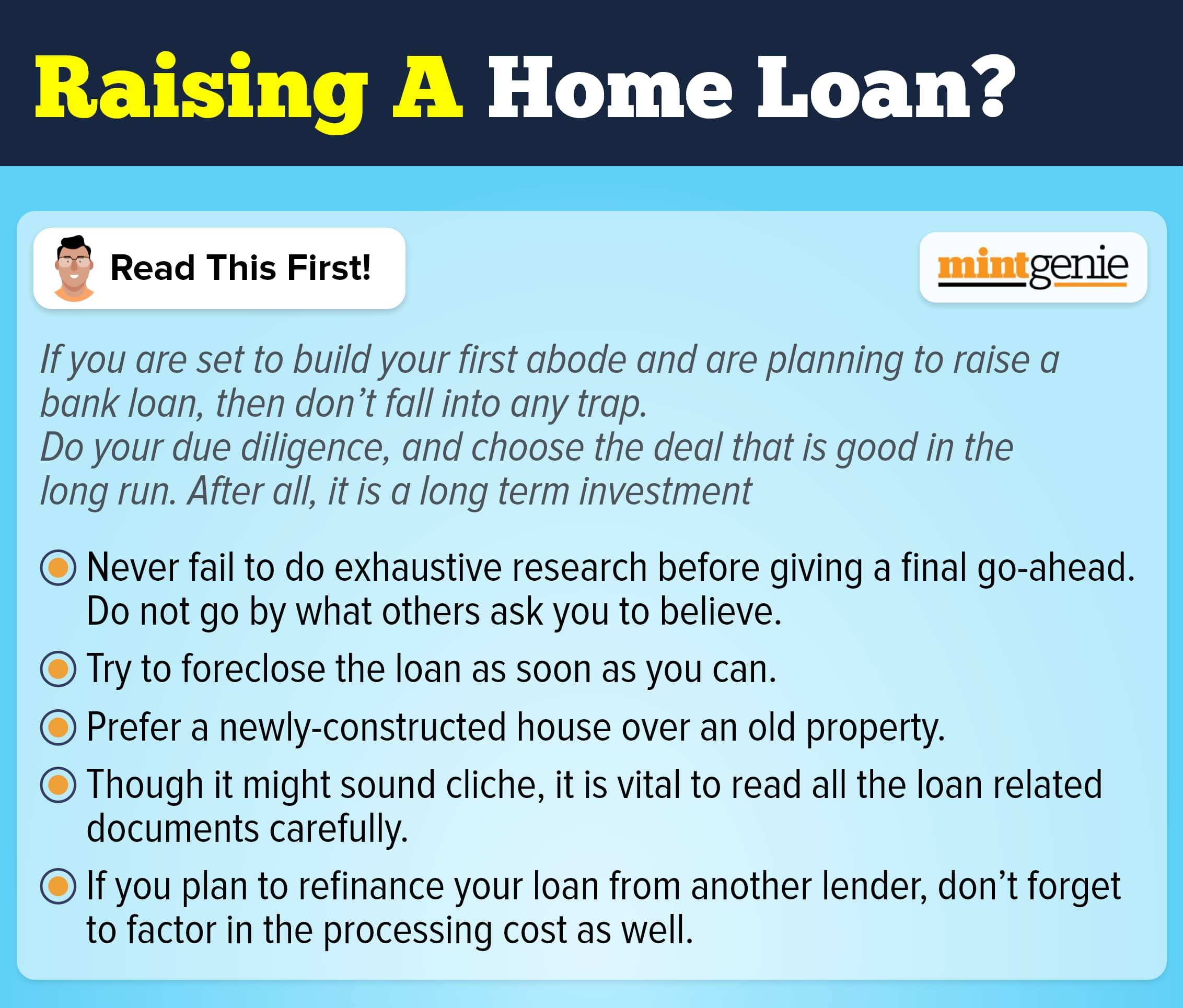

Having a financial goal and investment accordingly keep you disciplined in your investment strategy. It is the only way you can achieve your financial objective, through investment discipline. But, only being disciplined is not enough, you have to do tax planning also to make best use of your accumulated money at the end of the maturity period.

If you are investing in shares, bonds, mutual funds, ETFs or gold, you can transfer the sale proceeds to the Capital Gain Account Scheme (CAGS). By transferring the whole amount of sale from your investments, you do not have to pay tax on capital gains at the time of selling.

Will you be able to save both short and long term capital gains?

No, you can only save taxes when the sole purpose of long term investments. For your gains to be considered long-term, you must keep your listed traded shares and equity mutual funds for at least 12 months before selling them. Foreign and unlisted shares must be held for a minimum of 24 months before being sold then only it can be considered as long term investments.

While in the case of other than equity shares, like bonds, debt mutual funds, and gold and diamond jewellery, you need to hold these assets for 36 months to be considered as long term investments.

If you sell these securities before the above mentioned periods, you will not be able to avail the benefits of savings tax through CAGS.

Eligibility criteria

1. As it is not possible to just buy a house immediately after selling your investment. So, till you buy a house, you need to part your corpus in CAGS. However, you also have to follow a condition for withdrawing the money CAGS.

2. You have to buy a house within two years or construct a house within three years of selling your investments.

3. You should not own more than one residential house property at the time of selling your investments.

4. You cannot re-invest your sale proceeds on buying commercial properties.

5. You cannot sell your house that you bought by utilising your sale proceeds. You have to keep your residential property for at least three years. If you don’t satisfy the condition, your entire tax benefit would be reversed. Additionally, you have to pay penalty and interest on long term capital gains from the date of sale of your investments.

6. You need to park the whole sale proceeds from your investment in CAGS, not the long term capital gains only.

What if you hold investment jointly?

There are many couples who have a joint investment account, but it doesn’t affect your tax planning. Suppose you and your spouse are investing jointly, and you both are planning to buy a residential house property with the money you receive on maturity.

By planning your taxes in advance, you can save a significant amount of tax without facing any interference by the end of the income tax department. Tax planning plays an important role in managing your personal finances that you must consider before buying, selling, or parking your money.

Anushka Trivedi is a freelance financial content writer. She can be reached at anushkatrivedi.com