Car insurance is a vital financial safeguard for vehicle owners. It provides protection against financial losses due to accidents, theft, or damage to the insured (owner) vehicle. In exchange for regular premium payments, insurance companies offer coverage that varies based on policy types and individual needs.

In India, as per the Motor Vehicle Act, it is mandatory that all vehicles that are operated in public space must have car insurance. Without it, you can be fined ₹2,000 and/or imprisoned for 3 years for not having car insurance.

How much cover is sufficient? Well, it depends upon the current value of your car which means Insured Declared Value. IDV is the maximum amount that your car insurance company will reimburse (pay back) you in case your car gets stolen or damaged.

The premium amount depends upon various factors like the age of the year, model, etc. But, the car value depreciates every year which is why the IDV also decreases with every passing year.

What are the different types of car insurance?

There are 3 types of car insurance in India:

(a) Comprehensive Insurance - It means the policy will provide the coverage amount damages to your car (own damage cover) and third party liability (TP). This policy covers the risk for both the parties i.e., your own car and another person's.

(b) Third-Party Liability Insurance - It means the damages incurred by you to another person who is walking on pedestrian, people in another vehicle, etc. It also safeguards you from any legal liability and financial liability occurring due to your own car involvement in an accident.

(c) Pay as You Drive Insurance - This policy means that it allows you to pay a premium as per the kilometres driven. It is also known as ‘usage based car insurance’.

Ideally, one should consider taking their own car damage and third party liability i.e., Comprehensive Car Insurance, which covers both the risks.

The insurance company will provide you the claim if there is damage that occurs due to natural calamities, theft, riots, etc. But, the third party liability doesn’t cover it.

What does no-claim bonus (NCB) mean?

It means the insurance company provides you an incentive in the form of a discount for not making any claim. For first year, NCB provided is 20%; for second year, it is 25%; third year, 35%; fourth year, 45%; and fifth year, 50%.

For example, if you don’t make any claim in the 1st year, the insurer will provide you a 20% discount on your next year car insurance premium amount. The more you don’t claim, the amount of your premium keeps decreasing. But, if you make a claim, the NCB or discount percentage will be zero. It’s like a video game, if you fail in 5th level, you have to start from 1st level.

Every insurance company has some exclusions in their policy like wear and tear, depreciation, etc. But, to avail the benefit of exclusions, policyholders have the option of add-on. Following are the best add-on options you can opt for:

(a) Zero Depreciation - It means whenever you make a claim, the insurance company pays the amount. But, a part of it is given by you from your own pocket. It is the add-on feature on your base comprehensive policy. When added, it increases the premium amount by 15%. So, when you make a claim, you don’t have to worry about the huge bill.

(b) Engine Protection - It means the protection of your car engine from waterlogging. If you live in an area where the chances of waterlogging are high, you should definitely consider it an add-on in your policy.

(c) Voluntary Deductible (VD) - It is an amount that the policyholder agrees to pay ahead of submitting the insurance claim. It is determined by the policyholder based on their affordability. Higher the voluntary deductible, the lower the insurance premium and the higher the discount.

(d) Return to Invoice - It means you get the original value of the car at the time when you bought it along with registration cost and taxes, not the insured declared value. But, the amount will be given only when the car is stolen or lost. This cover is available for vehicles up to 3 years old.

Why does the insurance company reject a claim?

(a) Drink and Drive - When you’re driving the car in the influence of drugs or alcohol and meet with the accident, the insurance company will not provide you any claim.

(b) Delay in reporting - You are supposed to report an accident before the deadline. If you don’t give the report before the deadline, the chances are that your claim will get rejected.

(c) Owner Negligence - It means if you had parked your car in a no parking zone and somebody has stolen your car from there, the insurance company will not provide the claim as there is owner negligence.

(d) Fraudulent Claim - As the car insurance model works on ‘use it or lose it’, some policyholders voluntarily damage their car to get the benefit of a claim. But, if the insurance company finds that you’re misguiding them, the chances are that the claim will get rejected.

As per the recent update from IRDAI, it is compulsory that when you’re renewing your car insurance policy, you should have a valid Pollution Under Control Certificate.

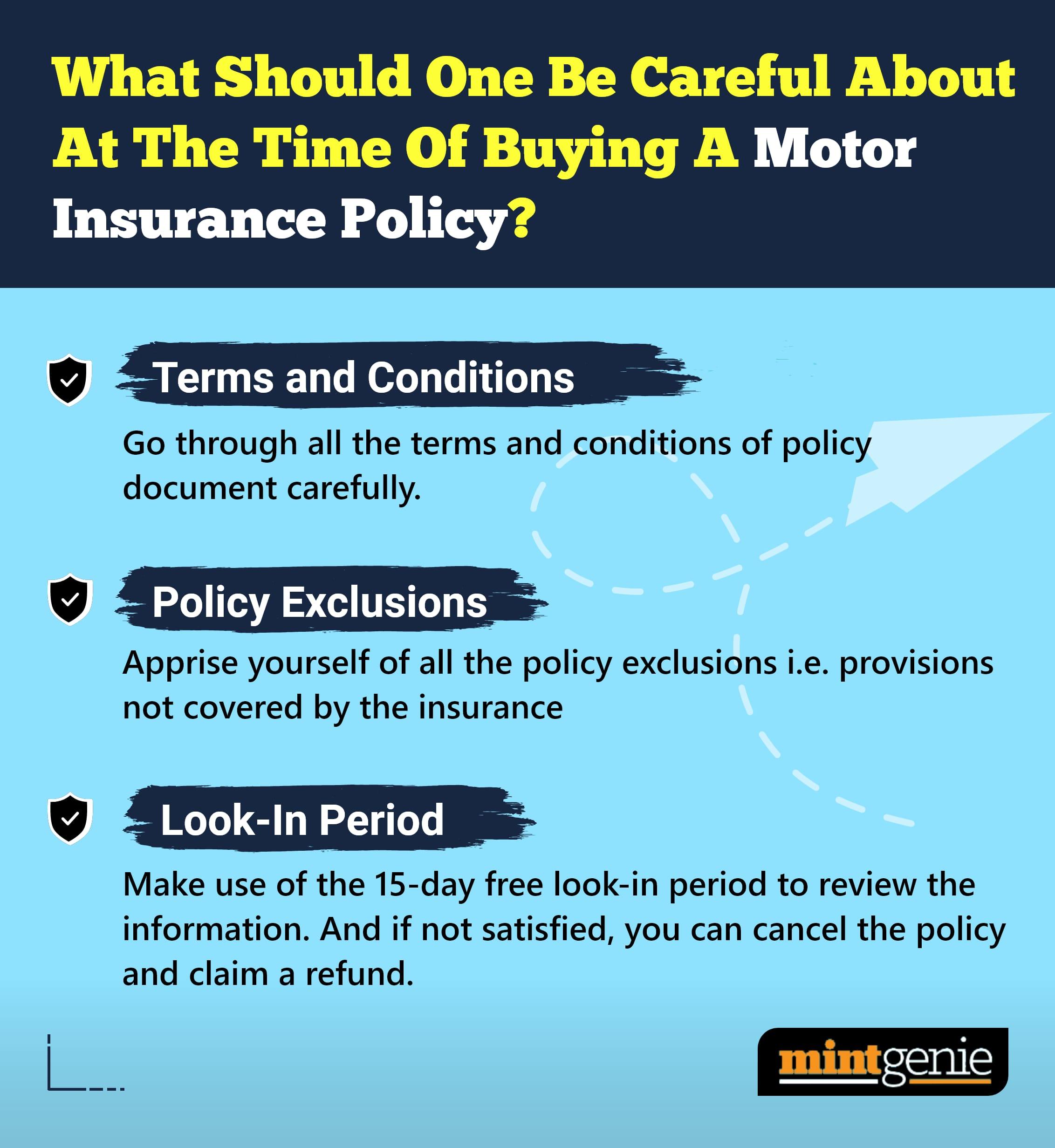

Read the policy very carefully and check what is covered in the policy and what is not covered. Also, read exclusions of add-ons (if chosen).

Car insurance is a vital protection that shields both drivers and vehicles from financial losses resulting from accidents, theft, or damage. It provides peace of mind, legal compliance, and financial security. Evaluating options, coverage levels, and premiums carefully ensures optimal coverage suited to individual needs.

Rohit Gyanchandani is Managing Director at Nandi Nivesh Private Limited