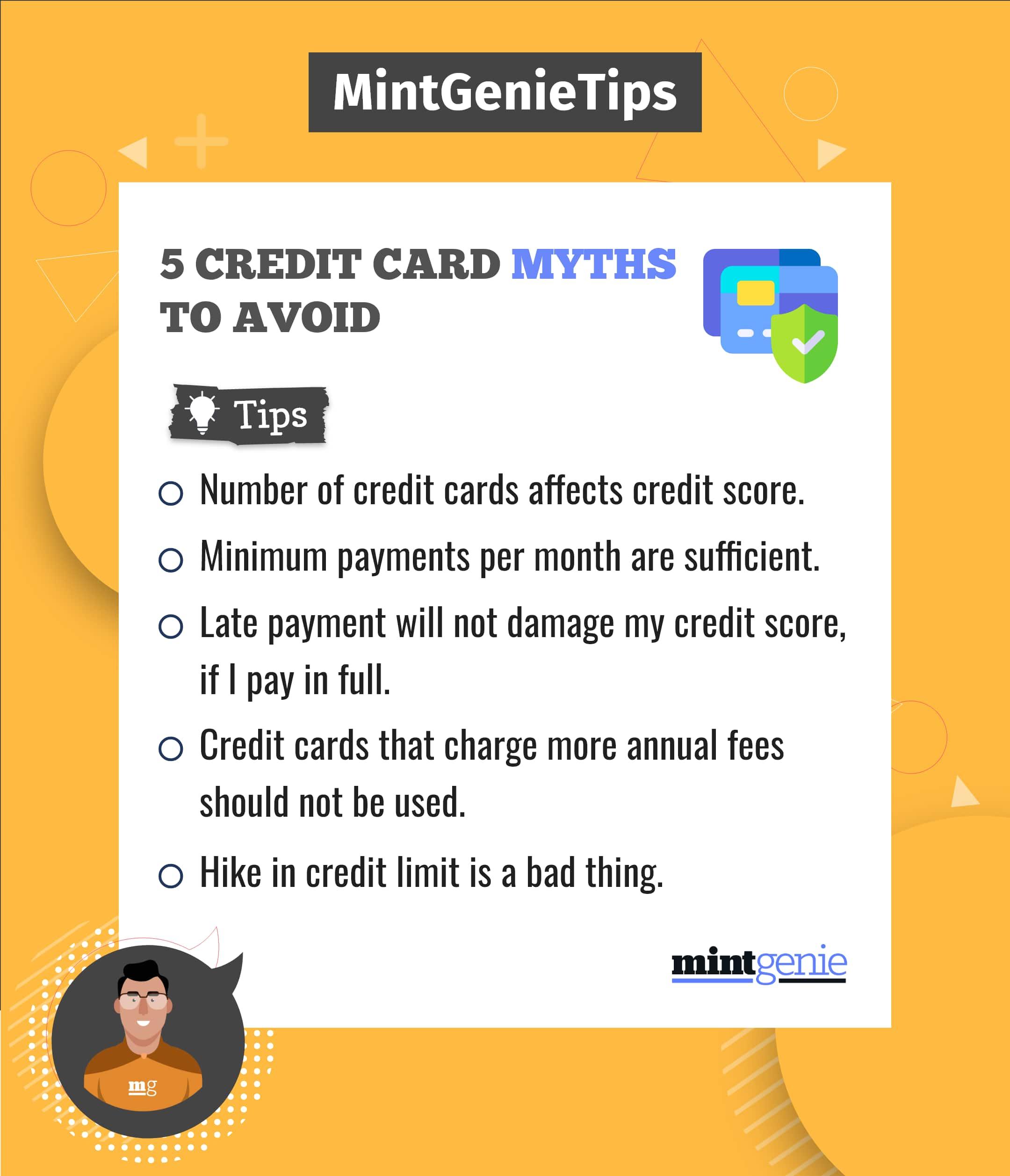

The concept of card network portability has generated excitement in the Indian financial system.

Portability is a word associated with mobile networks where a customer can change their mobile network while retaining their phone number. The Reserve Bank of India's (RBI's) new draft guidelines have extended this concept to allow people to switch between the five major card networks in India: Visa, MasterCard, RuPay, Amex, and Diners.

While mobile portability kept the phone number intact with a change in SIM card, card portability will keep the Primary Account Number intact and change the card number as per the network.

Key points from the draft circular ‘Arrangements with Card Networks for issue of Debit, Credit and Prepaid Cards’, effective October 1, 2023:

1. Issuers (banks and non-banking entities) are not allowed to have agreements or arrangements that restrict them from working with other card networks.

2. Issuers are required to issue cards to their customers from multiple card networks.

3. Issuers must provide the portability option to eligible existing customers, either during card issuance or upon customer request.

The RBI is accepting comments and feedback on this circular until August 4th, 2023.

These highlights will be made available to customers through either amending existing agreements or during the renewal process. Issuers can also enter into new agreements with the card network to ensure compliance.

Technically, card issuers need to be prepared for working with multiple bins, which is a challenge as it requires certification and operational readiness. However, if the card issuer has several tie-ups, then it won't be too difficult.

What happens to an ongoing chargeback?

As chargeback arises from a past transaction, there will be no significant impact on the card portability for the customer. The customer can raise a dispute anytime for a transaction within 120 days from the transaction’s date. The disputed transaction will pass through the old network’s protocols and process of dispute, chargeback, pre-arbitration and so on.

So, the card issuer will now deal with two different networks for a single customer. The disputed transaction will be handled as per the rules of the previous card network while any transactional dispute arising after card port will be handled as per the new network guidelines.

For example:

Mr. A has an ongoing transaction dispute with his card issuer with his Visa powered credit card and has just ported it to RuPay. So, technically, his Visa card is now revoked, and he will be issued a new credit card under the RuPay network. This means whatever dispute he had ongoing before the new card issuance comes under Visa’s purview. So, even if the said dispute progresses towards pre-arbitration or arbitration stage, it is still Visa chargeback protocol.

On the other hand, when it comes to gauging partnerships, there could be a whole new dynamic shift. No more the perception of owning a partnership-specific privileged card. Instead, card issuers and networks will have to compete to offer the best deals to retain customers. On the customer side, they will have the availability of options that can be a mix of lifestyle, travel, food and entertainment suited to their lifestyle.

On the UPI side, this circular is advantageous for increasing the acceptance of RuPay, which is the only native card network for credit card payments through UPI. Although the draft circular has caused some excitement, it remains to be seen how people will respond to this initiative and what types of cards will be curated to stay ahead of the competition.

The author, Praveen Krishna Dev, is Co-founder & CEO, Backspace Tech.