Debt investments are perhaps a lot more complicated today than in the past, says Harsh Gahlaut, Co-founder & CEO, FinEdge.

In an interview with MintGenie, Gahlaut insists that adhering to asset allocation is a must as understanding the relationship between risk and reward is a necessity.

Edited Excerpts:

Q. What percentage of people seeking your advice already have financial goals in mind?

A vast majority of people looking at investing, still approach it in an ad-hoc manner and without a clear purpose. Unfortunately, the top reasons driving investing are either quick returns or herd mentality. Less than five per cent of people approach us with clearly defined goals for investing, and another 10 per cent come to us with a generic goal like long-term wealth creation.

However, since Dreams into Action, DiA, our proprietary tech platform doesn’t permit ad hoc investments by design, all our clients necessarily end up setting clear goals before they begin their journey! These goal-setting conversations have been described as “life-changing” or “eye-opening” among other things because the shift from investing for returns to “investing with purpose” marks quite a dramatic change in perspective – one that usually automatically ends up curtailing several detrimental investing behaviours and vastly improving your chances of generating long term wealth.

Q. Do you think people must now rely more on debt investments after the recent global banking fiasco and recurring geopolitical tensions?

Firstly, the recent fiasco with SVB bank is unlikely to have a contagion effect that would spill over into the global markets; but even if it were to, we would certainly not advise investors to change their long-term, goal-based strategic asset allocation based on news and events.

Debt investments are perhaps a lot more complicated today than in the past. Adhering to asset allocation is a must. Understanding the relationship between risk and reward is a necessity.

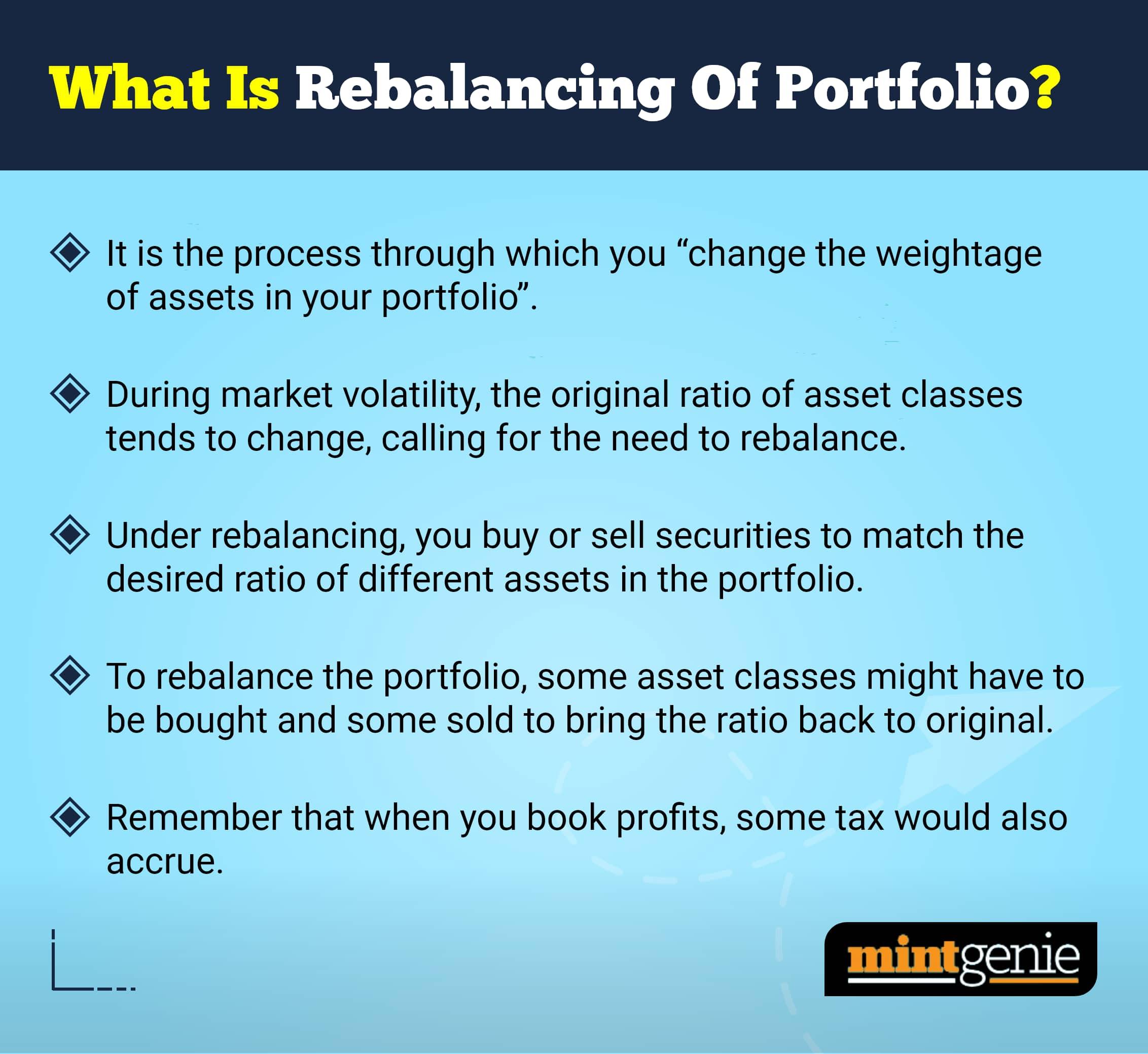

The government has thrown a spanner in the works by proposing a change in taxation for debt mutual funds. This perhaps is more important than any transitionary upheaval in global banking. In asset allocation, depending upon the exact requirement of the investor, all asset classes including real estate, gold, fixed deposits, Government Securities and debt mutual funds will play a role. Once again, it’s the purpose of investing which is more important than the product. Questions like how far is your goal or is the preservation of capital more important than returns will decide what your tactical asset allocation would look like.

Q. What steps do you advise people to take to maintain sound financial health?

Start with keeping an eye on your cash flows to ensure that they are adequately managed –

Balancing your lifestyle without compromising your important long-term goals is very important. Do not recklessly pile on the EMIs as that can have a cascading effect on your financial goals.

Whenever possible, save for your goals in advance and make retiring from high-cost debt a priority. Get a financial plan made for yourself and invest according to the goals that you define there, as moving away from ad hoc, returns-centric investing to goal-based investing can make a huge difference to your financial health. Not only will you be investing in the right places for the right reasons, but you’ll also be able to indulge in guilt-free spending knowing that your financial goals are on track.

Don’t fall into the trap of living above your means and trying to “Keep up with the Joneses”, as that can lead you down a vicious spiral of overspending and debt. Live within your means and keep stepping up your goal-based investments every time your income goes up.

Finally, enlist the help of a reputable financial advisor who can advise you on your investments. This simple move can make a huge difference to your financial health and safeguard you from a host of regrettable money decisions.

Q. Many investors look for tax-saving investment options at the very last minute. What is your view on this?

Like everything in life, procrastination is detrimental to your cause. A person who plans has the advantage not only of better managing their cash flows but also taking advantage of rupee cost averaging. We believe that a good investing practice is to ensure that “tax saving” is a subset of your overall investing strategy. For example, if you are investing monthly for your retirement goal, a smart thing to do would be to start a SIP in an ELSS fund.

You can meet two objectives with one investment. If you make tax-saving investments at the penultimate hour, these decisions are almost always regrettable! You’ll probably end up locking your money into a fruitless life insurance plan or tax saving fixed deposits, or investing in an ELSS without fully understanding the risks involved in equity investing.

Q. With so many mutual funds promising high returns and investing in the same market instruments, how do you suggest investors decide where to allocate their earnings?

Counterintuitively, the promise of high returns is a big red flag for us! We view sudden outperformance in a fund as a cautionary point, as that outperformance may have involved an inordinate amount of risk-taking or speculation. When it comes to fund selection, we view factors such as consistency of returns, trueness to label, the strength of the fund management team, the strength of the asset management company (AMC) and risk management framework as far more important than short-term outperformance.

For us, what’s most important is that an investment helps a client meets their goals; which means that if the goal is planned at a 12 per cent return, we are happy if the fund delivers a consistent 12 per cent return while managing risks adequately and absorbing shocks along the way!

Q. There are too many new fund offers (NFOs) in the market now. Should new-age investors enter them at such an early stage?

As a matter of principle, we do not recommend NFOs to clients unless there’s a very strong reason to do so – such as a completely new and promising investment theme from an AMC with a solid track record and a great fund management team.

For the best part, we suggest that investors should stick with solid, well-established funds that have a track record of navigating difficult market cycles instead of investing in NFOs with the fallacious belief that “low NAV is cheap” or “more units are better”. As a thumb rule, always choose an established fund within the same category over an NFO.