If you are a regular mutual fund investor, you are likely to be already aware that the fund houses tend to offer two types of plans to its investors. The first one is a growth plan, while the other one is income distribution-cum-capital withdrawal plan (IDCW).

It is important to note that what is now popular as IDCW was earlier known as dividend plan until its name was changed w.e.f. April 1, 2021 to align with SEBI guidelines.

In some ways, these plans are similar to the types of fixed deposits where depositors have the options of cumulative and non-cumulative schemes.

In the former, interest on deposit gets added to the deposit amount and in the successive quarters, interest is accrued on the cumulative sum. On the other hand, in non-cumulative scheme — interest is paid out at regular intervals to the depositors.

Growth & IDCW plans

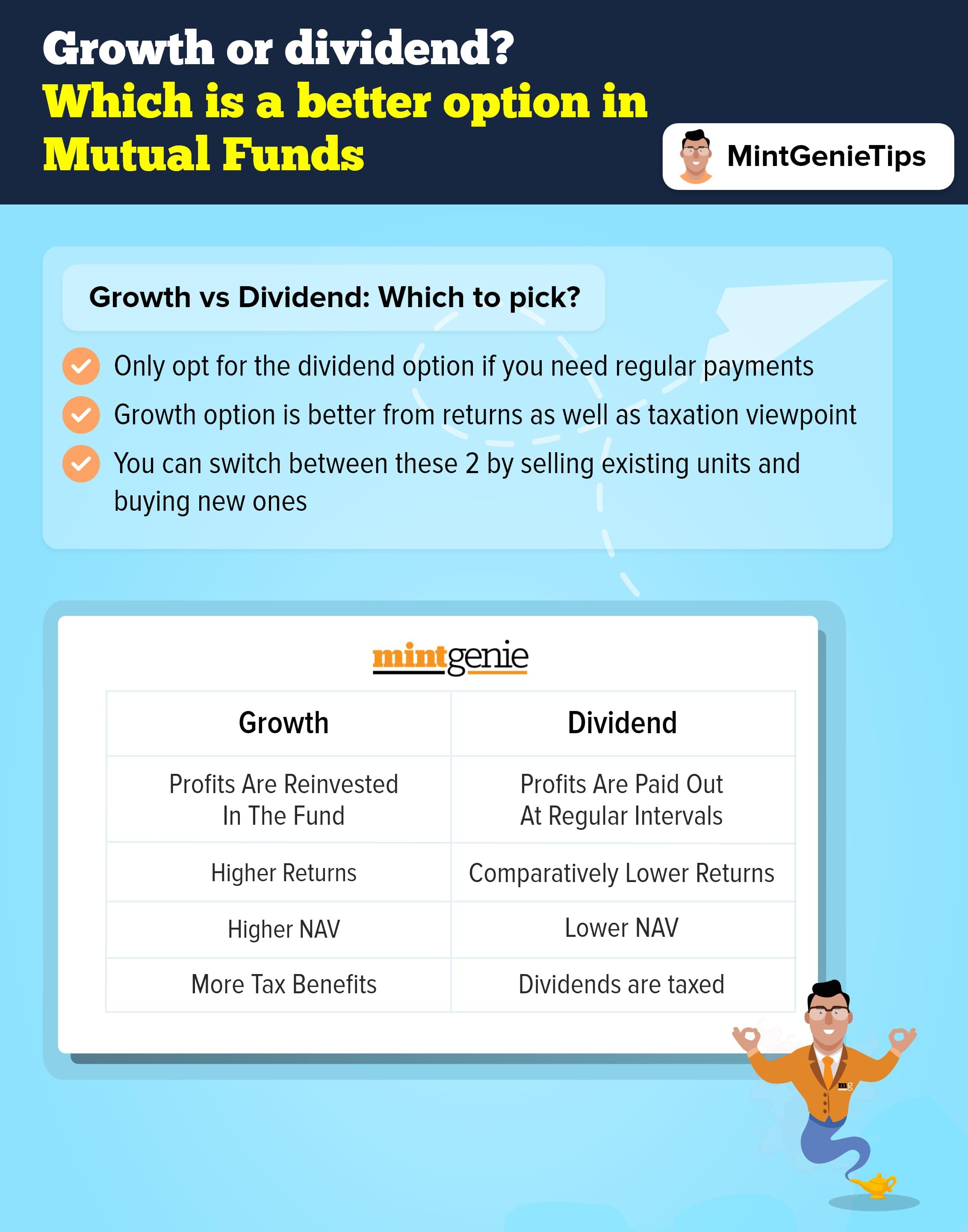

Mutual fund houses offer two options to the investors in most of its schemes – the first one is to buy a growth plan while the second is IDCW. In case of Income Distribution cum Capital Withdrawal (IDCW) plan, whatever income is earned on the mutual fund is distributed, leading to the withdrawal of capital.

Conversely, in the growth plan, your dividend income gets added to the net asset value (NAV), thus increasing your overall portfolio. Financial advisors often tell investors to choose growth option since it allows the fund house to keep ploughing back returns, thus helping to capitalise on the power of compounding.

"Growth plan enables investors to reap the fruits of compounding whereas IDCW deprives them of the same. Unless you have a plan to sell your fund units in near future, one should prefer a growth scheme," says Deepak Aggarwal, a Delhi-based financial advisor.

Let us understand this with the help of an example.

Suppose you own fund units worth ₹one lakh with one fund house. As a result of dividend distribution on some of the stocks the scheme holds, there is a dividend income of ₹7,000. Now, if this is a growth plan, this amount will be ploughed back to the scheme, thus adding to the overall value of your units from ₹1 lakh to ₹1.07 lakh.

On the other hand, in case of IDCW, the dividend amounting to ₹7,000 is distributed and the leftover sum i.e., ₹one lakh will stay invested in the fund scheme.

In the first scenario, you will get the benefit of compounding as the overall invested sum will keep increasing. In the second scenario, this options will be missing.

Which one is better?

Most mutual funds give the option of choosing between growth plan and income distribution cum capital withdrawal plan. In the growth plan, the NAV keeps growing because of reinvestments. Under this plan, in case investors are looking for an income on a regular basis, they have to sell some of the fund units.

Under the IDCW plan, the fund house pays some portion of the gains to the unitholders.

The timing is usually decided by the AMC. After the payout, the fund’s net asset value drops by the amount distributed. But investors must be aware of the fact that the amount paid out is liable to income tax since it amounts to withdrawing money from the fund.

To summarise, there is no specific benefit in either of the two categories barring the benefit of compounding in case of IDCW plan.

And as experts advice that investors are recommended to choose growth plan and sell some of the units as and when they need money instead of receiving proceeds at irregular intervals regardless of their financial need during that time.