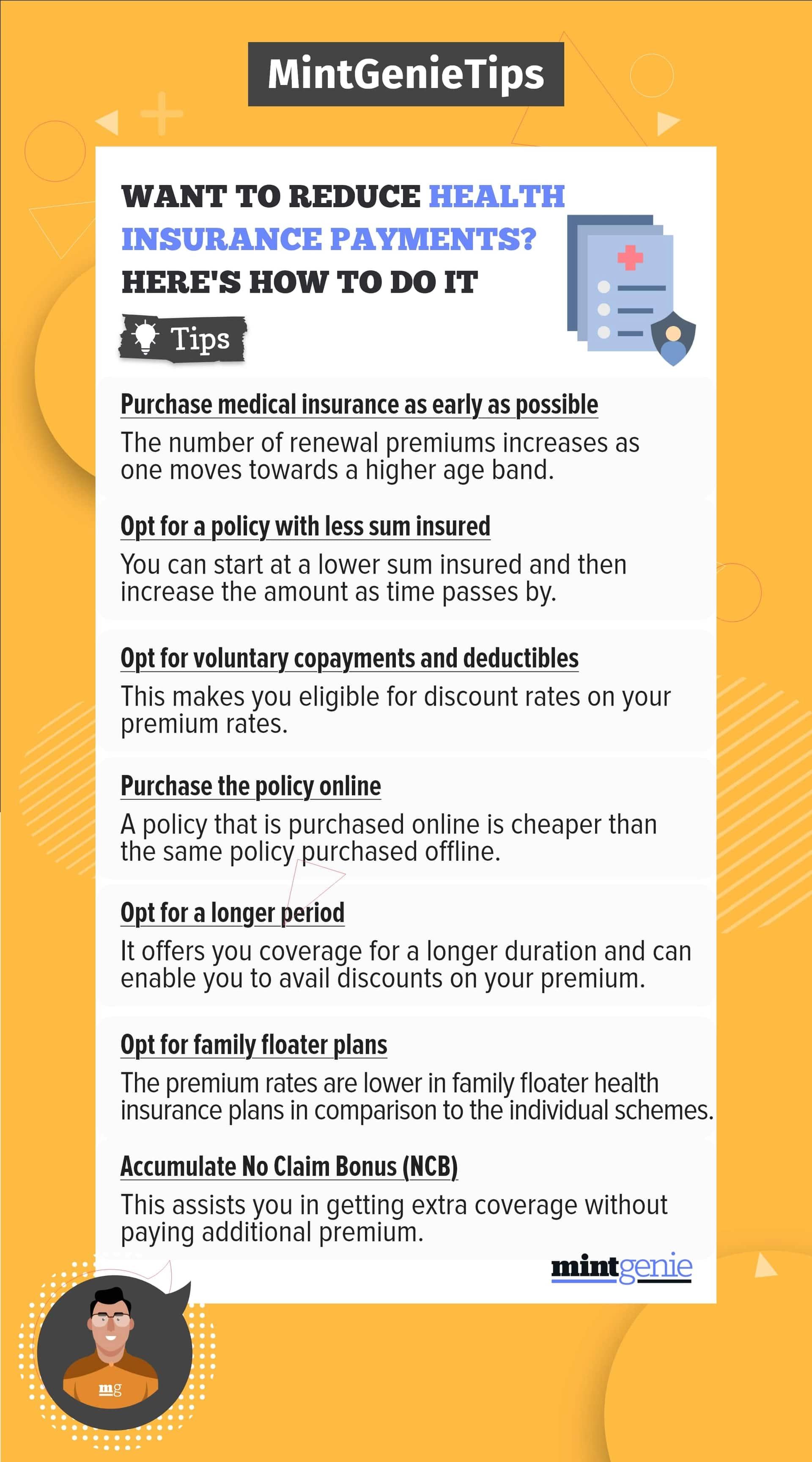

As the cost of medical treatment has risen significantly in the past few years, getting a medical insurance cover is, therefore, an indispensable part of an individual’s bouquet of investments.

Insurance companies reimburse the cost for hospitalisation and, for the outpatient department (OPD) also, any treatment of patients carried out at home is usually not covered.

What is domiciliary hospitalisation?

When a patient cannot be transported to a hospital owing to a variety of reasons – his poor health being one — the insurance company may reimburse the cost of treatment at his/her home just like a hospitalisation cover. This treatment of patients at home is also referred to as ‘domiciliary treatment’.

These expenses may get covered when the insurance policy offers this as an add-on cover. Alternatively, this could be covered as part of the main medical insurance policy for an extra premium.

How does it work?

It is important to note that domiciliary treatment cover requires a certificate from the treating doctor recommending this line of treatment.

A number of insurers offer this cover such as HDFC ERGO’s health insurance cover, Star Health Insurance and Tata AIG MediCare.

The domiciliary hospitalisation expenses by HDFC ERGO, for instance, are covered when it is prescribed by a certified healthcare practitioner, moving the patient to the hospital is impossible due to their poor health condition and the treating medical practitioner advises treatment at home since the rooms are not available in the hospital.

Should you opt for it?

It is important to note that domiciliary hospitalisation is not included in insurance policies by default.

So, it is recommended to check whether an insurance plan has this built-in feature. And if not, one can buy it as an add-on feature.

While evaluating the domiciliary hospitalisation benefit, one must consider a number of factors such as the sum insured, conditions to be fulfilled, waiting period, inclusions and exclusions.

So, it is incumbent upon policyholders to look for the treatments that are permissible under domiciliary hospitalisation and importantly — the extra premium, if any.

It is also vital to note that domiciliary hospitalisation does not cover asthma, tonsillitis, upper respiratory tract infection, bronchitis, gout, arthritis, and rheumatism, diabetes mellitus and diabetes insipidus, among others.

Getting an insurance cover for domiciliary hospitalisation is, therefore, highly recommended because it enables policyholders to avail timely treatment and also takes care of unanticipated medical emergencies at the same time.