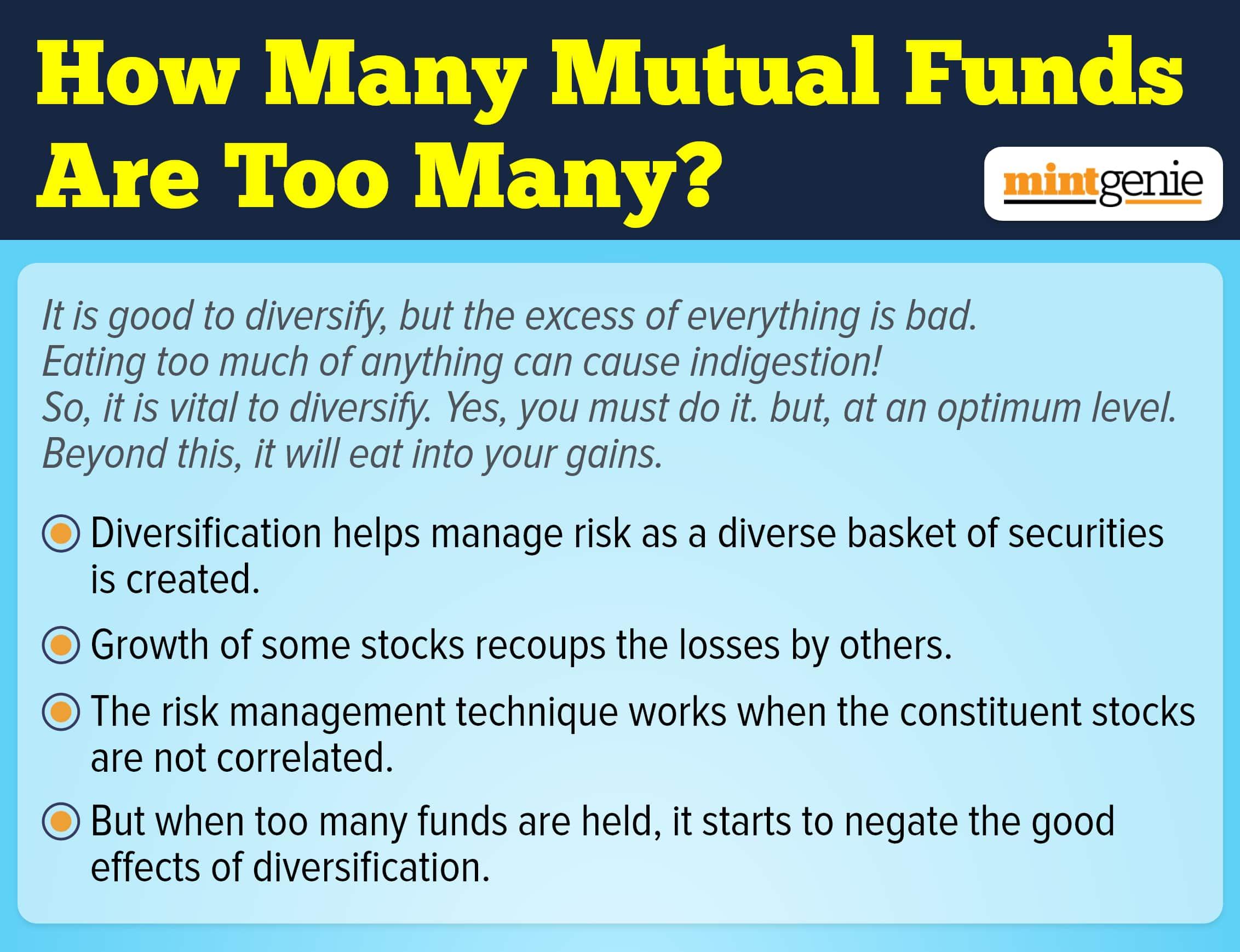

So much is said and written about earnings from mutual funds that it prompts many wannabe investors to invest in them. What irks them is the inability to decide how much money to park in them. Like many other investments, mutual funds are also money-making options that are tied to financial goals.

Apart, mutual fund performance is tied to market performance, thus, prompting us to decide our financial goals accordingly. This also means that you must set the target first, and decide for how long you wish to stay invested and at what interest rates.

Muthukrishnan, Chennai-based Certified Financial Planner says, “Before beginning to invest, the following should be in place for any investor:

- Emergency fund

- Term insurance

- Medical cover

- No debt other than a home loan

Once these hygiene factors are in place, efforts should be made to invest not less than 10 pecent of income in index funds or equity funds. To accelerate wealth creation, the percentage of income invested should be 20 percent or more. The minimum investment tenure for equity should not be less than 10 years.”

Calculating your investments

The web has eased the returns calculation process. This means that investors can easily use the online calculator or web applications such as excel and Google spreadsheets to learn how the returns over a period affect the value of investments with time. Also, investors must know that the market does not deliver fixed return rates, which means that they must be prepared for rate fluctuations in the event of market volatility. Consider the average rate of returns based on estimates and previous years’ returns, especially, for these capital-market linked products.

Once you have assessed how much money you must invest to reach your financial goals within the stipulated period, you must put in a bit of a higher amount to make up for the shortfalls during sudden market crashes. Though the market is bound to rise subsequently, the unforeseen volatility can eat into your returns, thus, delaying your idea of achieving the much-desired corpus. However, if you are averse to taking risks or prefer being a conservative investor, you must consider the pros and cons of trimming your returns in the long run.

An individual investor Saurav Srivastava, CFA Charter holder, FRM Certified, CBAP & CSM Certified says, “We should focus on the target corpus number. And if we see actual return rates have turned out to be lower than the assumed return rates taken while planning the investment. Then we need to increase our investment to make up for the shortfall. For example, I had assumed 15 per cent returns while planning for a SIP to fund the education of my daughter. I see that markets have been returning 12-13 per cent returns in the last few years due to various reasons. I should increase my SIP amount accordingly to invest more such that even with the lowered return I can hit the required corpus to fund my daughter’s education.”

The increased investment must be done to make good for the loss in capital appreciation by pouring some more money into investments off and on.

How do you define financial goals?

We may invest in the same markets, but that does not imply that we all have the same financial goals. A lot depends on how much you earn, your responsibilities, when you want to retire, your lifestyle expenses, and the retirement fund anticipated. This underscores the need to save and invest more to ensure maximum corpus and a comfortable lifestyle ahead, especially, during the post-retirement phase. Exercising prudence while allocating investments is a must to minimize the risk involved and maximise the earnings as output.

Once you are aware of your financial goals, you may proceed to invest in a lump sum or through systematic investment plans (SIPs) done monthly, quarterly, half-yearly or annually depending on your resources. To date, many mutual fund houses have launched fund offers that accept lower SIPs too, thus, easing the investment process. However, such a low SIP value must not deter you from making big investments. Remember “Money earns money; wealth begets wealth.”

Value your money

Investments depend on how you view them in the light of both the present and the future. Choose from among the feasible options. Avoid those that you do not understand. Taking unwarranted risks may backfire. Abide by the famous adage every time you take a step ahead to invest, “When money realizes that it is in good hands, it wants to stay and multiply in those hands.” The financial goal must be an ideal amount which will allow you maximum investment and earn optimum returns.