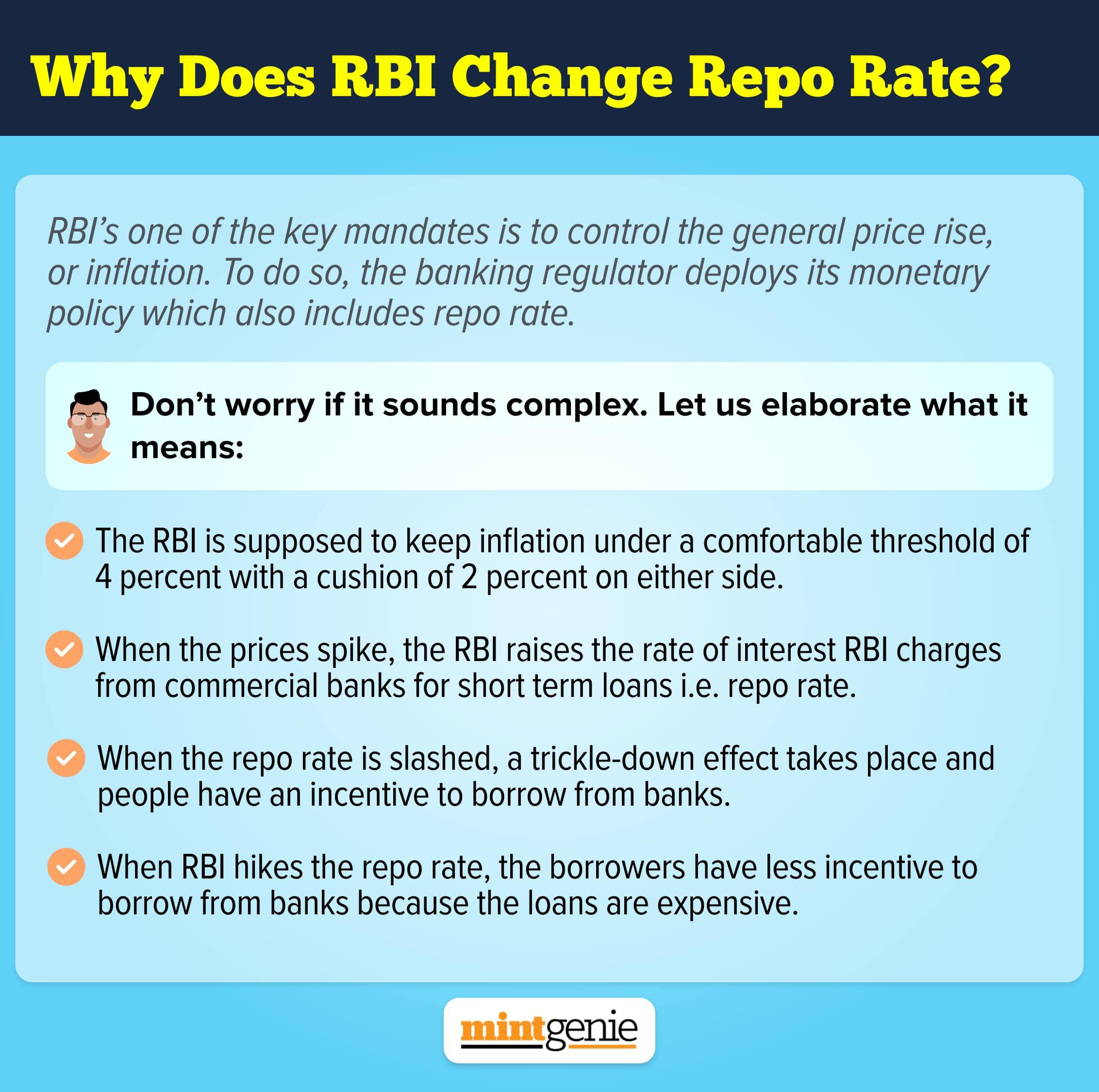

The rising interest rate regime is here. The Reserve Bank of India on Wednesday increased the repo rate by another 50 basis points after an out-of-cycle rate hike of 40 bps last month. The repo rate now stands at 4.90 per cent. The move aimed at squeezing the liquidity out of the system to curb inflation will impact your money in different ways. While it is positive for depositors, the borrowers will have to swallow the bitter pill. Moreover, more rate hike cannot be ruled out.

"While further rate hikes remain clearly on the table, with the reference to the revised repo rate of 4.9% remaining below the pre-pandemic level, the comment on the orderly completion of the government borrowing programme has served to cool the 10-year G-sec yield. We foresee further repo hikes of 35 bps and 25 bps, respectively, in the next two policies,” says Aditi Nayar, Chief Economist, ICRA.

It is time to re-calibrate your investments to optimise returns and minimise risks. MintGenie looks at various investment avenues:

1) Equity

The stock market has already factored in the rate hike, which is reflective in the way the markets have behaved over the last couple of months. The Nifty50 index is down 6% from the beginning of April and 12% from all-time high touched in October 2021 as on Tuesday’s closing. Rising interest rates and equity markets have an inverse relationship. When interest rates on safer instruments such as fixed deposits and small-savings schemes dwindle, people looking for high-yields tend to flock to the stock market. That is what panned out from April 2020 onwards. However, now that the trend is reversing, investors may move back to safer investment avenues. The inflows in equity mutual funds already fell 44% in April 2022. But, if you are a smart investor, you would do well creating an equity portfolio when the markets are on a downtrend. If you are already invested, avoid exiting your positions just because the market sentiment has turned negative. Deploy more either through mutual funds or direct stocks.

2) Debt

Rising interest rate regime is a boon for risk-averse investors. While banks take time to transmit higher interest rates to deposits, eventually it has to happen. Bank fixed deposits are the simplest and safest way to invest money for a fixed tenure. Then there are company fixed deposits by top rated NBFCs or housing finances companies which give slightly higher interest rates compared to bank FDs. One may also consider RBI Retail Direct platform which enables retail investors to directly invest in government securities. With interest rates rising, the g-sec rates will improve, going forward. Besides, one may go for debt mutual funds as well. In a rising interest rate scenario, investing in short-to-medium duration debt mutual fund schemes make sense.

3) Real Estate

If you are planning to buy a house for living, the rising interest rates should not bother you as most of the banks and housing finance companies have flexible interest rates which get adjusted with the overall interest rate scenario. Looking at it from homeownership point of view, one may go for it irrespective of the interest rate cycle. The real estate prices look set to go up.

However, if you are looking at it from investment purpose, it may not be a good idea because yields on house rentals are unattractive, hovering around just 2-3%. For example, in big cities, the average rent ranges between ₹25,000-30,000 per month for a flat costing around ₹1.5 crore. This gives a yield of around 2.4% annually. Even if we factor in the capital appreciation of the house, the returns may not match what you may otherwise earn on index funds. Considering the taxation and liquidity, equity mutual funds could be much better than real estate.

Rising interest rates call for a rebalancing of your portfolio. Diversify your investments to attract inflation-beating healthy returns.

Aprajita Sharma is a freelance journalist and a certified financial planner. She can be reached at @apri_sharma on Twitter and LinkedIn.