I am a 40-year-old wholesaler, who has traditionally invested in gold in the form of gold coins and biscuits. I recently came across new-age instruments to invest in gold such as Gold ETFs and SGBs. Can you please elaborate on the key differences between the two instruments and specifically highlight the risk associated with both.

Naveen Mohanty, Bhuvneshwar

Gold has been the trusted choice of investors across geographies and demographics. There are multiple reasons behind its popularity including (a) low risk, (b) use in jewellery making, (c) easily accessible, (d) simple purchasing process. However, there are certain drawbacks associated with physical gold too:

Safety: storing large amounts of physical gold in your house can cause a safety issue for you and for your family.

Liquidity: Physical gold cannot be liquidated at short notice, the process generally involves finding a suitable jewellery or lender and thereafter visiting their office in order to obtain cash. The process can take as long as 1 week.

Gold ETFs and SGB have been introduced to tackle all the pain points associated with physical gold and at the same time retain all the positive characteristics of physical gold.

Gold ETF

Gold ETFs are a subcategory of mutual funds which invest in gold exclusively. The mutual fund house has to hold gold, against which it issues mutual fund units to investors. As a result, your pain point associated with storing gold is eliminated in the case of Gold ETFs. Each unit of a Gold ETF represents a certain amount of gold. At the time of the launch of a Gold ETF (called - a new fund offer), the Gold ETF units are typically priced at ₹10 and represent a few milligrams of gold.

The aforementioned pricing structure allows investors to invest even minuscule amounts in gold through these units. The price of these units after issuance moves up or down depending on the market price of gold. In essence, your investment is tied up to the performance of gold as a commodity.

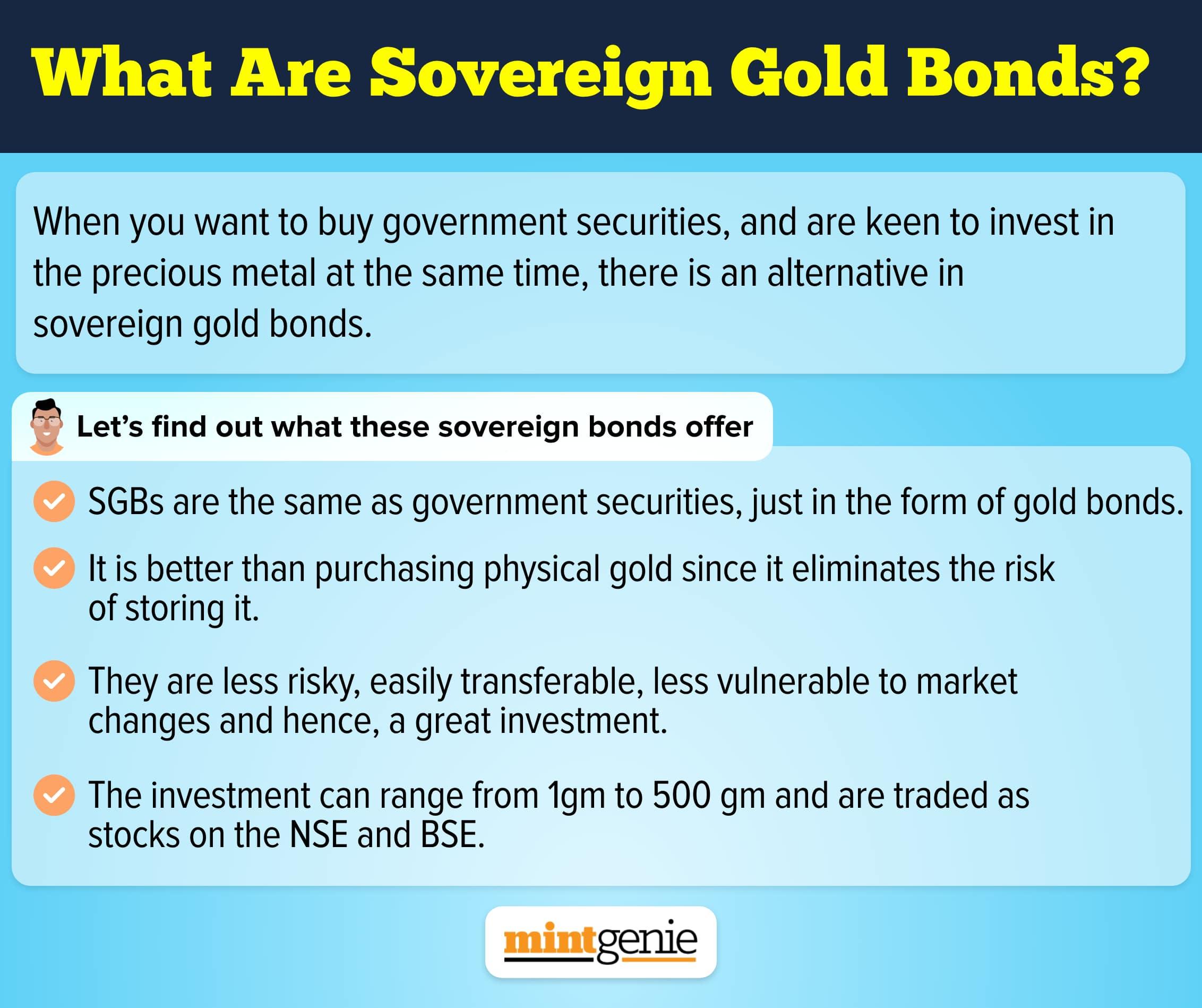

Sovereign Gold Bonds

The SGB scheme has been launched by the Reserve Bank of India (RBI) in order to reduce India’s import bill. India is one of the world’s largest importers of gold, and this import results in a loss of foreign exchange. Though many Indians purchase gold as an ornament/jewellery, many Indians also purchase gold as an investment product.

SGBs are government securities representing a certain amount of gold in grams. They serve as alternatives to holding actual gold. When you purchase SGBs your investment value is tied to the performance of gold as a commodity.

Key Differences

Though SGBs and Gold ETFs sound similar there are a few key differences between the two. We have enumerated the difference below:

Gains

In the case of Gold ETFs, the investor does not earn any kind of interest; their potential gain or loss is completely dependent on the price of gold. However, in the case of SGB, the investor earns an assured interest of 2.5% of the initial amount they invested in the SGB scheme.

Conversion

In the case of Gold ETFs, you can exchange your Gold ETF units for physical gold. However, please note that there is a minimum threshold prescribed by the mutual fund house below which it will not exchange your units for physical gold. Typically the mutual fund houses prescribe units equivalent to 1 kilogram of gold. In the case of SGBs, there is no option to convert SGB into physical gold.

Taxation

Gold ETFs are classified as debt mutual funds and are taxed accordingly. If you hold your Gold ETFs for a period of 3 years or more before selling them you will be required to pay long-term capital gains tax at the rate of 20% along with indexation benefits. In case you hold them for a period of less than 3 years, the capital gains you generate will be added to your income and will thereafter be taxed according to your income tax slab.

In the case of SGBs, you benefit from in two ways (a) capital appreciation - when the price of gold goes up and (b) interest income at the rate of 2.5% per year. In both the cases your gains/income from SGBs will be completely tax free.

Tenure

In case of SGBs the tenure of the scheme is 8 years, however, early encashment is allowed from 5th year onwards. Please note that if you are holding your SGBs in demat form you can sell them at any point of time on the stock exchange. Gold ETFs can only be held in demat form, they can be sold at any point of time.

Convenience

In case of Gold ETFs you will first require a demat and trading account to purchase the Gold ETF units. In case of SGB you are not necessarily required to hold them in demat form. You can hold SGBs in certificate form too.

Conclusion

If you are looking to purchase gold purely from an investment purpose, SGBs and Gold ETFs are two new-age instruments to invest in gold. Investing in either will take care of traditional pain points associated with storing physical gold - safety and liquidity.

However, if you are looking to invest in gold for the purposes of converting it into jewellery at a future date for the marriage of your kids, investing in physical gold makes more sense.

Kuvera is a free direct mutual fund investing platform.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.