Q1. I am a single woman, with two dependent children. What is the best way to protect my family?

Like most parents, your primary concerns must be to provide for the everyday needs of the family, invest for the children’s education, and to be prepared financially to meet unexpected emergencies. A financial advisor begins by fully understanding your needs and concerns before chalking out a financial plan that is tailored to what you want to achieve.

There are a lot of moving parts in our financial lives. No financial plan can possibly predict every event or outcome. However, having a clear plan after careful thought makes it easier for you to take detours where you must, without getting lost and missing the destination.

Engage a financial planner. Answer all the questions the expert asks you. Do not hesitate to share all your concerns about finance. The outcome will be a financial plan that will be key to your family’s protection and prosperity.

Q2. What is risk tolerance? Why is it important to know that before I invest?

Risk appetite or risk tolerance is a measure of how much of a risk or loss an investor is willing to take when they invest in various portfolios. For example, a product may promise excellent returns if everything goes well, but you may lose your investment if things go wrong. Are you willing to take that risk? Maybe your risk appetite is just sufficient to put in a fraction of your money in this product?

Risk analysis considers the investor’s age, investment goals, income, and comfort level. It enables an investor to objectively assess one’s own risk appetite.

An investor with a high-risk appetite (and who has good knowledge of the money market) can invest in higher-risk investments such as equities and exchange traded funds (ETFs), in order to maximize returns over a shorter time, despite the risk. An investor with a moderate risk appetite or tolerance may instead opt for a mix of stocks and bonds, thus settling for moderate returns at moderate risk. A conservative investor with a low-risk appetite is best advised to invest heavily in bonds, that offer low returns but are regarded as the safest.

According to the guidelines issued by the Association of Mutual Funds in India (AMFI), every mutual fund announcement is expected to display its riskometer—a graphical representation of the risk a mutual fund carries. It displays five levels of risk—low, moderately low, moderate, moderately high, and high.

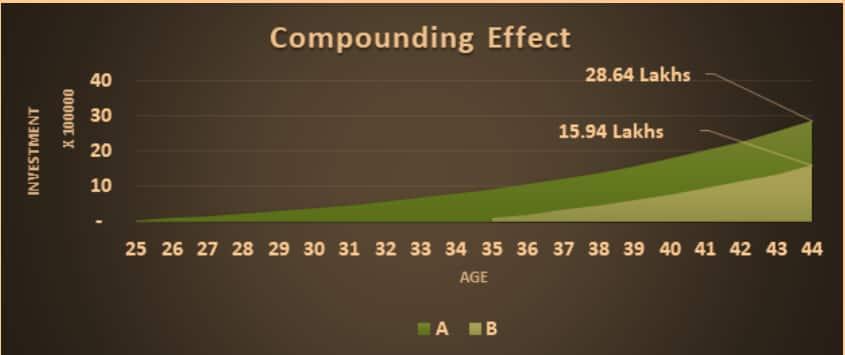

Q3. I am 27. I started investing in mutual funds two years ago. What effect will compounding have on my investments?

Time has the greatest influence on your investment portfolio. Over time, a small amount of money can grow into a substantial amount, thanks to the power of compounding. This is achieved by letting the returns be reinvested so that it sets off a cycle of returns yielding more returns. The more time this cycle is allowed to play out, the larger your returns. Therefore, it is important to start investing early to benefit from the power of compounding.

Let’s compare the case of two friends A and B.

| Particulars | Pearson A | Person B |

| Annual Investment Amount | 50,000 | 1,00,000 |

| Returns | 10% | 10% |

| From Age | 25 | 35 |

| Till Age | 44 | 44 |

| Total no. of years investment was made | 20 | 10 |

| Total investment | 10,00,000 | 10,00,000 |

As we can see in the above example, A & B both invest the same amount of Rs. 10 L but A starts early and B starts 10 years later. As a result, although A starts with half the investment value as compared to B, A stays invested for double the no. of years and ends up with a higher corpus at the age of 44. An extra Rs. 12.7 L comes in due to the compounding effect.

Thus, we can say, yes, in your case, too, you are on the right track. Compounding will help your investments grow big if given enough time. Keep investing regularly to take benefit of compounding on your investments as it is considered a powerful investing concept (as you can see from the above example).

It is advisable to start investing from the time you start earning and stay invested till your retirement unless there are some liquidity requirements. If you withdraw money, then make sure you tap the earliest invested portion first so that you benefit from a taxation point of view.

Q4. I am a senior citizen and I need an additional source of income to meet my expenses. I currently have pension coming in, I live in my own house along with my spouse but the rising maintenance and helper charges are taking a toll on me. What do you suggest?

For most senior citizens, the house one owns is the largest component of wealth. Reverse mortgage monetizes the owner’s equity in the house as an asset.

You could opt for this option and generate a 2nd stream of income. You will have to mortgage your house to a lender. The lender will then start paying you periodically right through your lifetime. You do not have to make any repayment of principal or the interest.

The maximum tenure of the loan is 20 years.

In case you move to another house permanently, you may choose to prepay the loan and the accumulated interest, release the mortgage and reclaim ownership of the house.

If the borrower dies, the lender may sell the house to recover the principal and the accumulated interest. Someone from the borrower’s family may choose to be the buyer, thus keeping the property within the family.

Advantages

- It enables house-owning senior citizens, who have no other assets or inadequate income, to meet their financial needs. It partially provides social security.

- The loan amount should not be used for speculation (shares or real estate), trading or business.

- The borrower will continue to be the owner of the house.

- The borrower does not have to repay the loan during one’s lifetime and as long as one stays in the same house.

- All payments received by the owner under RML shall be exempt from income tax under section 10(43) of the income-tax Act,1961.

Settlement of loan

- The loan shall become due and payable only when the last surviving borrower dies or permanently moves out or sells the house. Typically, a “permanent move” means neither the borrower nor any co-borrower has lived in the house continuously. The lender may obtain documentary evidence to support this.

- The realized sale value of the property is used to settle the loan (principal plus interest).

- The borrower of the estate of the borrower shall be provided with the first right to settle the loan before selling the property. A reasonable amount of time, say up to 2 months may be provided for the sale when repayment becomes due.

- If the sale proceeds yield a surplus after settling the loan, that will be passed on to the legal heirs or estate or specified beneficiaries of the borrower.

- If the proceeds fall short of the outstanding principal and interest, the mortgage loan is capped at the value of the home equity. In this case, the lender bears the loss.

International Money Matters Pvt Ltd is a SEBI registered investment advisory firm. If you have any personal finance queries, click here to talk to advisors from IMMPL.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.