For women, the journey of financial independence takes on a unique hue due to societal intricacies and distinct economic realities. Despite the challenges, a strategic financial plan can serve as a compass guiding women towards achieving self-reliance.

The foundations of strong financial future (20s-30s)

The nascent stages of a woman's career form the bedrock upon which financial independence is built. The creation of an emergency fund is important not only now but all stages of one’s life. An emergency fund, equivalent to three to six months' worth of living expenses, stands as a cushion against unexpected adversities such as medical emergencies or job losses.

Commencing a retirement savings journey early on can yield substantial long-term dividends. Contributing to provident funds or availing of retirement schemes like the Employee Provident Fund (EPF) or Public Provident Fund (PPF) can instil financial security in the later years. It is prudent to explore investment avenues such as equity mutual funds to harness optimal growth. At the same time, you should focus on tax efficient investment options to optimise after tax returns.

It is important to keep in mind a few things, not just at this stage but throughout. First is diversification, which means that it is crucial that you spread your risk across different asset classes to achieve long-term financial growth and stability. Second, as mentioned earlier, you should invest a substantial portion of your portfolio into equities as with age on your side, you can harness the power of compounding. And third, avoid trying to predict short-term market movements and instead adopt a long-term perspective.

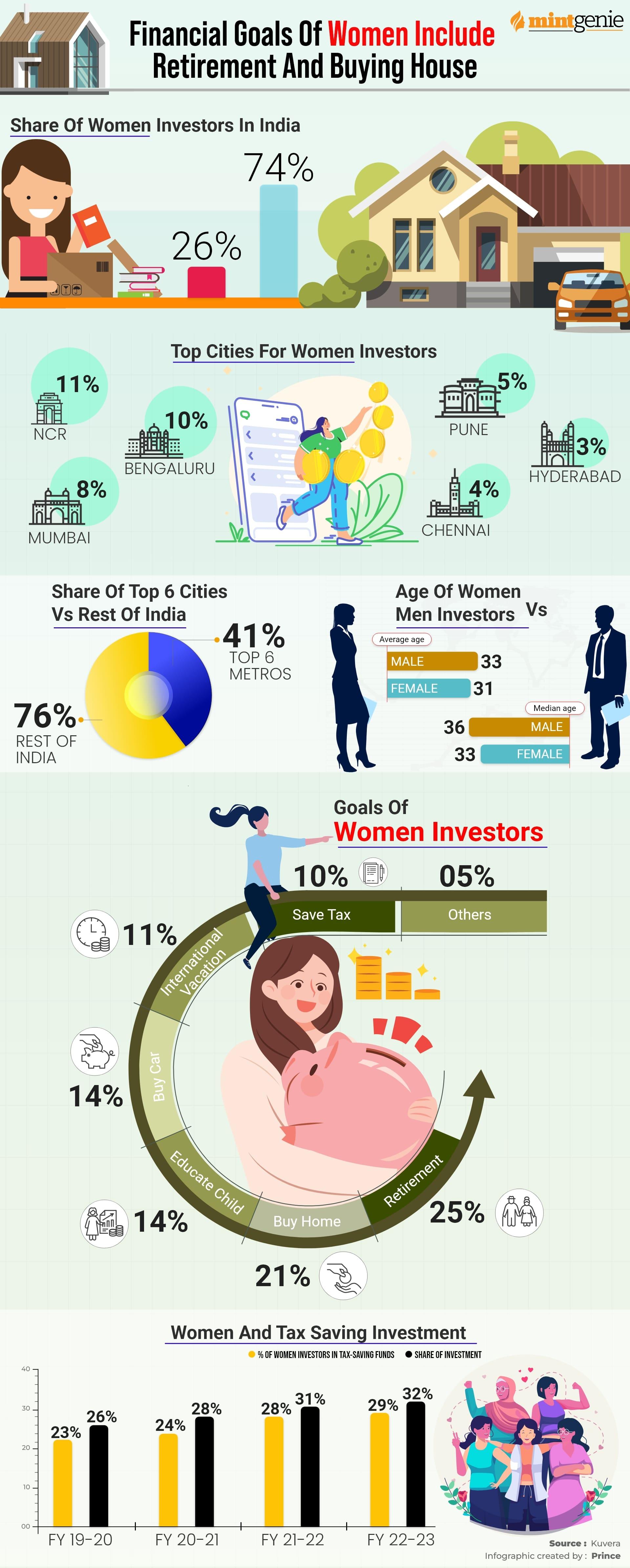

Women have different investing and planning needs than men. While every family has its own dynamic, women are more likely to push pause on their careers to care for children or other family members, and this typically occurs just as they are entering their peak earning years. The cumulative effect on wealth can be profound. Hence it is advisable to start saving at early stages of their career.

Juggling a career and a family (30s-40s)

For many women, the third decade is prime time for getting married, starting a family and shifting gears on a career.

As women steer through their careers, they often find themselves skillfully balancing professional growth with familial obligations. Mow, crafting a budget that encompasses household expenses and provisions for children's needs becomes pivotal. While achieving a harmonious work-life balance remains crucial, maintaining an unwavering focus on long-term financial goals is equally important.

If you take a break from full-time work, step up your investing responsibilities at home. Be the CEO of your home finances. Even if you’re not earning it, you can play a role in amplifying it.

Safeguarding against potential contingencies, including life and health insurance coverage, becomes important. Seeking professional guidance for a personalised investment approach is recommended.

It is also important for married women to be financially independent so that they are prepared for the event of a divorce. Instead of being totally dependent on their husbands, women should be financially literate and in charge of their own finances.

Steadying the ship (40s-50s)

As retirement beckons, women must intensify their savings efforts and prioritise the reduction of high-interest debts. This phase also necessitates revisiting career goals and venturing into avenues that amplify income, such as acquiring new skills or nurturing entrepreneurial aspirations.

This is the juncture for designing an exhaustive retirement plan. Carefully scrutinising potential sources of retirement income, estimating future expenses, and orchestrating strategies around instruments such mutual funds and the National Pension System (NPS) constitute essential steps. Exploring additional retirement-focused investment vehicles can serve to further elevate financial security.

Transition to retirement (50s-60s)

Transitioning towards retirement involves refining the financial blueprint to align with evolving lifestyle preferences. Exploring options for downsizing or relocating can have positive implications for post-retirement financial stability.

Addressing long-term healthcare considerations takes centre stage. Researching, comparing, and securing suitable health insurance plans or creating dedicated healthcare funds can alleviate the financial strains associated with medical expenses in the later stages of life.

The golden years (60s and beyond)

Even in the post-retirement phase, astute financial management remains crucial. Women must chart out a sustainable withdrawal strategy from retirement accounts, accounting for market fluctuations and projected life expectancy. Regularly reviewing investments and adjusting the portfolio as per necessity is indispensable to ensure financial stability during the retirement years.

Estate planning assumes centre stage during this juncture. Collaborating with legal experts to devise a comprehensive estate plan, encompassing elements such as a will, living trust, and power of attorney, ensures a seamless transfer of assets in accordance with one's desires.

The pursuit of financial independence for women is a journey that spans a lifetime, regardless of gender. Indian women, navigating a myriad of societal and economic complexities, must tailor their financial approaches to suit their individual contexts.

Seeking counsel from financial experts and recalibrating the financial strategy as circumstances evolve will empower them to navigate life's uncertainties with resilience, ensuring a secure and self-sufficient financial future. This independence day, it is time to take charge of your finances and chart your way towards financial independence.

Priyanka Wadhwa, Co-Owner, Kapila Krishi Udyog Limited