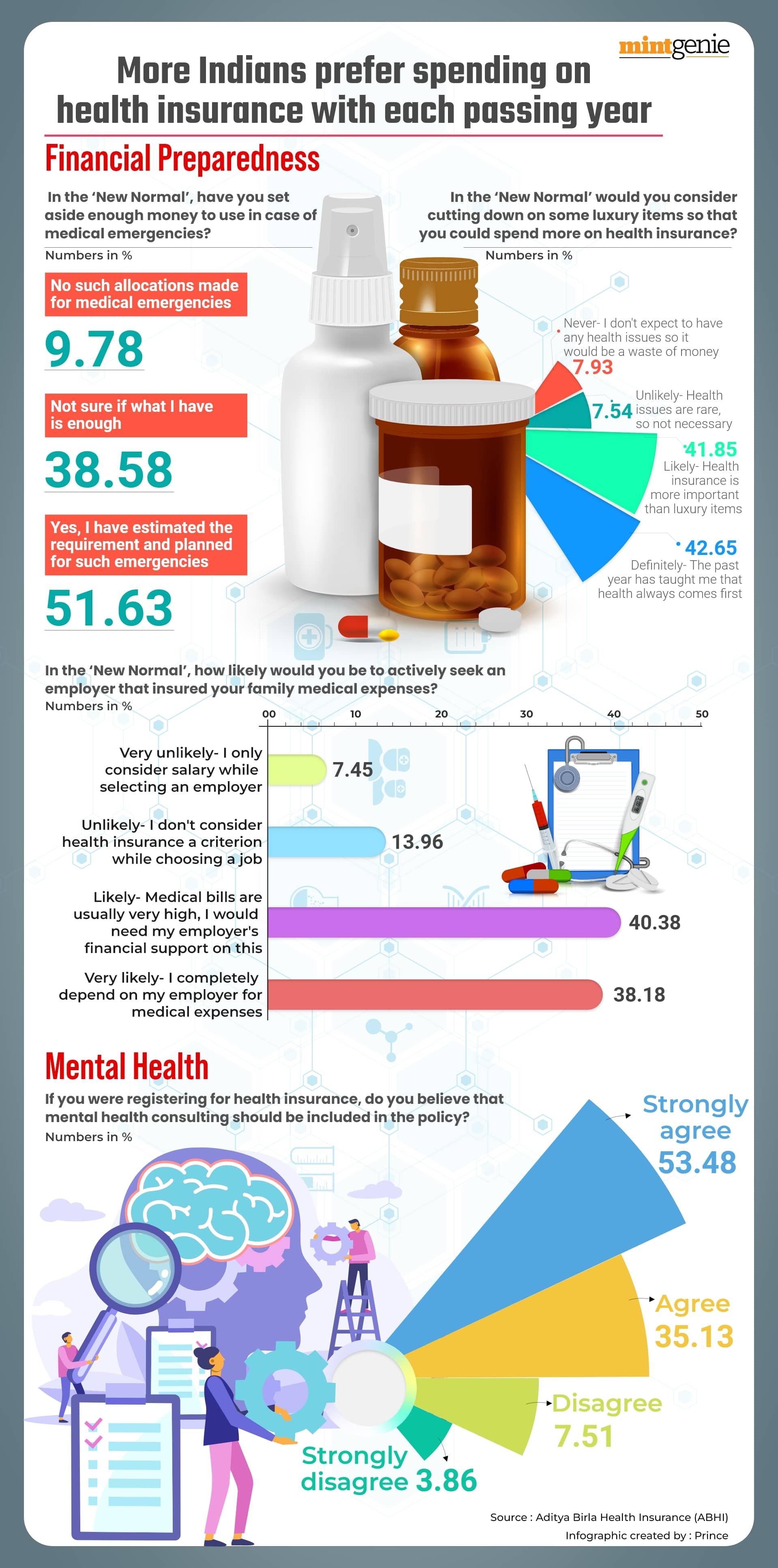

Good health is not about your looks or weight; it is the absence of illness that sets one free both in mind and body. While the whole country celebrates “Independence Day”, the senior citizens in our families are mostly confined to their houses owing to poor health conditions. High medical costs prevent so many people from seeking the necessary treatment.

Undoubtedly, health insurance holds great importance for senior citizens due to their heightened susceptibility to health issues. Buying them the much-needed health insurance means giving them a feeling of “independence” from the fear of succumbing to illness or not availing the benefit of the available medical infrastructure. However, choosing the right health insurance plan for one’s parents or in-laws, or other senior citizens in the family is not easy.

Essential factors to consider while buying health insurance

Selecting a health insurance scheme for elderly individuals can prove to be a complex and laborious task. When purchasing a health plan, it’s crucial to consider key factors such as coverage for hospitalization and the associated premiums.

Pre-existing illnesses

Old age is synonymous with health problems, which means that you must be aware of possible medical conditions that plague your aged loved ones. Health insurance policies commonly impose conditions on pre-existing illnesses that fall under their coverage. These policies might entail elevated premiums or even policy denial based on this criterion. It is vital to thoroughly review the terms and conditions specifying which pre-existing illnesses are included before selecting a health plan.

Consider the following aspects regarding pre-existing illnesses within health insurance policies:

- A pre-existing illness refers to a medical condition diagnosed before obtaining the health insurance policy.

- Typically, pre-existing illnesses are not covered during the initial two to four years of the policy, known as the pre-existing illness waiting period.

- Following the waiting period, the insurance provider might cover pre-existing illnesses, though this could involve higher premium charges.

- Some health insurance policies might entirely exclude specific pre-existing diseases from coverage.

Carefully examining the terms and conditions of the health insurance policy is essential to ascertain which pre-existing illnesses are encompassed and to comprehend the waiting period.

In-patient hospitalization coverage

Ensuring comprehensive in-patient hospitalization coverage holds immense significance within a health insurance plan tailored for senior citizens. Given their heightened susceptibility to health issues, senior citizens often face increased hospitalization instances. Hence, selecting a plan with optimal in-patient hospitalization coverage becomes paramount.

When opting for a health insurance plan focused on maximum in-patient hospitalization coverage for senior citizens, consider the following pointers:

- The sum insured denotes the maximum amount the insurance provider will reimburse for your medical expenditures. It's essential to choose a sum insured adequate enough to cover anticipated medical costs during hospitalization. For senior citizens, it's advisable to opt for a sum insured of at least ₹5 lakhs.

- The plan's coverage should encompass all foreseeable medical expenses, encompassing hospital stays, physician fees, surgical procedures, and medications. Confirm whether the plan extends coverage to pre-existing conditions and assess the waiting period. Opting for a plan that covers pre-existing ailments post a two-year waiting period is prudent for senior citizens.

- An extensive network of affiliated hospitals facilitates seamless cashless treatment. Verify if your preferred hospitals are part of the insurance company's network.

- The plan should also provide supplementary advantages like preventive health check-ups, daycare treatment, and ambulance services. These perks can prove invaluable for senior citizens, given their heightened vulnerability to health challenges.

Expenses post-hospital treatment

Expenses incurred after hospitalization, known as post-hospitalization expenses, encompass costs such as follow-up medical appointments, diagnostic tests, and medication. Typically, the eligibility period for these expenses spans from 60 to 90 days after the patient's discharge from the hospital.

In the case of senior citizens, insurers often impose specific criteria and limitations on the scope and extent of post-hospitalization expense coverage. This is largely due to the higher likelihood of chronic health conditions among senior citizens, which can result in escalated post-hospitalization expenditure.

Consider the following factors regarding post-hospitalization expenses for senior citizens:

- The eligibility period for post-hospitalization expenses might be comparatively shorter for senior citizens compared to younger adults.

- The coverage amount designated for post-hospitalization expenses might be less extensive for senior citizens compared to their younger counterparts.

- Certain post-hospitalization expenses, such as home care or long-term care, might not be covered by some insurers for senior citizens.

Deductibles payable

Health insurance premiums are generally higher for senior citizens than younger adults. This variance arises from the greater likelihood of senior citizens utilizing their health insurance and incurring elevated medical costs.

Furthermore, deductibles for senior citizens are typically set at a higher level than those for younger adults. A deductible represents the initial amount that the policyholder must personally cover before the insurance provider commences reimbursement for medical expenditures. A heightened deductible implies that the policyholder will need to bear a more substantial out-of-pocket expense before the insurance coverage taking effect.

When selecting a health insurance plan for senior citizens, it's imperative to account for both premiums and deductibles. The policyholder should opt for a plan that aligns with their financial capabilities, encompassing both monthly premium commitments and potential out-of-pocket costs.

Co-payment and sub-limits

When considering a health insurance plan for senior citizens, two significant aspects to take into account are co-payment and sub-limits.

Co-payment refers to the portion of each medical expense that the policyholder is required to personally cover. Typically expressed as a percentage, such as 10 per cent or 20 per cent, co-payments contribute to the overall cost of the medical service.

Sub-limit designates the maximum amount the insurance provider will reimburse for a specific medical expense. These limits are commonly established for specific medical categories like room and board, surgical procedures, or medication costs.

Distinct co-payment and sub-limit structures may be presented for senior citizens as opposed to other age groups within health plans. This distinction arises from the higher likelihood of senior citizens having chronic health conditions, which can result in elevated medical costs.

While choosing a health insurance plan for senior citizens, it's essential to consider co-payment and sub-limits. Opting for a plan featuring lower co-payments and sub-limits, if feasible, can help minimize the policyholder's personal expenditure, thus keeping out-of-pocket costs manageable.

Nothing beats a life free of diseases. No doubt that continued research and development have ensured the best treatment for all. However, this comes at a price, and in some cases the costs can be exorbitantly high, thus, underlining the need to have a health insurance in place, especially, for the senior citizen members in our families who are more likely to suffer from health disorders in long run.