You will find so many people inquiring how much retirement corpus would be enough for them. Some even ask if they must aim for a ₹5 crore retirement corpus. As odd as it may sound, investing with the intent to accumulate such a massive corpus stems from the fear of not having enough money in hand post-retirement owing to the impact of inflation and the continued decreasing value of money. The prices of essential commodities and services are increasing, which means that we would need more money to avail of the same goods and services.

Financial Planning: Is ₹5 crore enough for retirement? Here's your answer

TL;DR.

Instead of targeting a standard retirement corpus, you must assess how much money you would need in your post-retirement phase depending on your current lifestyle expenses and inflation rate.

Calculating retirement corpus

There is no easy way to find out how much money you would need in the future. However, your planning today will depend on what you estimate for tomorrow. One way is to find out the future value of your financial needs based on how much you spend today and the current inflation rate. You may use the retirement calculator online to find out how much money would be enough by the time you retire.

To check if ₹5 crores would be enough for you to pay off your expenses and maintain your current lifestyle, you must find out the future value of money based on inflation. To estimate the retirement corpus that we must have to take care of our old-age expenses, let us make the following assumptions based on which

- Current age: 30 years

- Age at which retirement is planned: 60 years

- Life expectancy: 80 years

- Current monthly expenses: ₹40,000

- Time left for retirement: 30 years

- Estimated inflation rate per annum: 7%

This would translate to:

Monthly expenditure at the time of retirement: ₹3,04,490

Yearly expenditure at the age of retirement: ₹36,53,882

Provision for expenses on healthcare and travel: ₹3,00,000

Inflation rate affecting travel and healthcare: 7%

Expenses on healthcare and travel at the time of retirement: ₹22,83,677

Yearly expenditure post-retirement: ₹59,37,559

Monthly expenditure post-retirement: ₹4,94,796

Expected inflation rate post-retirement: 10%

Life expectancy post-retirement: 20 years

Expected returns on earnings post-retirement: 6%

Corpus needed at the time of retirement: ₹17,92,30,104.

The myth that ₹5 crores would suffice for your retirement is nothing short of a myth. This estimated corpus is a huge amount, thus, underlining the need for aggressive investments in mutual funds, especially equities, and myriad other investment opportunities while also ensuring enough health insurance coverage in hand to meet medical expenses.

Planning your retirement corpus

This brings us to the next pertinent question in retirement planning, “How do we plan our retirement corpus?” A lot depends on your risk profile. Irrespective of the market volatility, you cannot help but invest a part of your earnings into equities to earn returns that beat the inflation rate while also helping you create a corpus in the long run.

To start with, you can invest in a large-cap fund followed by aggressive investments in hybrid funds, equity-linked savings schemes (ELSS) and small-cap funds.

If you are looking forward to a fixed pension amount, you can relegate a part of your earnings to the National Pension Scheme (NPS).

Setting apart what you might need to pay for sudden emergencies in an emergency corpus, you may park a small part of your earnings in debt funds and corporate bonds.

After staying invested in equities and equity-related instruments during the first 25 years, earnings from them must be gradually shifted to debt funds, fixed-income plans and bank deposits depending on the money requirement. This ensures that your earnings from equities do not suffer owing to a sudden market crash while continuing to earn relatively stable returns from their debt counterparts.

Monthly investment (in Rs) | Nature of investment | Category Average Returns (in %) | Investment tenure (in years) | Corpus accumulated

(in Rs) |

| 30,000 | Large-cap fund | 14 | 25 | 8,18,18,331 |

| 15000 | Aggressive hybrid fund | 13 | 25 | 3,40,71,525 |

| 12500 | ELSS fund | 15 | 25 | 4,10,50,922 |

| 7500 | Small-cap fund | 15 | 25 | 2,46,30,553 |

| Total Corpus Accumulated | 18,15,71,331 | |||

For added tax benefits, you can invest ₹4,500 in NPS for the next 30 years. To date, NPS investors have earned roughly 14 per cent returns on their investments. Taking a conservative approach, let us assume that you earn around 12 per cent on the funds parked in this scheme.

Monthly investment (in Rs) | Name of the investment | Average Returns (in %) | Investment tenure (in years) | Corpus accumulated |

| 4500 | National Pension Scheme | 12 | 30 | 1,58,84,612 |

Source: https://www.npstrust.org.in/content/pension-calculator | ||||

You can either take out the entire accumulated corpus if invested in NPS Tier-2 Scheme or opt for a monthly pension scheme depending on how much percentage of the earnings you want to be converted into an annuity. However, you cannot purchase an annuity for less than 40 per cent of the amount earned. Apart from the added tax benefits, NPS investments allow you access to a regular pension throughout your post-retirement phase, thus, allowing you enough money in hand to pay for your essential expenses.

To achieve the much-desired retirement corpus, you must invest ₹65000 in equities every month for the next 25 years. However, five years before your retirement age, you must shift your funds systematically to debt funds, corporate bonds, post office savings schemes, senior citizen savings schemes and bank deposits.

People with a lower risk appetite may opt to put money in the public provident fund (PPF) and related government schemes. However, the downside is that you must stay invested for at least 15 years, which makes it difficult to withdraw money in case you suddenly need the money.

Both PPF and ELSS funds offer tax benefits under Section 80C of the Income Tax Act, 1961. However, the lock-in period in ELSS funds is three years compared to the prolonged tenure of 15 years in PPF, thus, allowing you to withdraw money from the former in case you wish to reinvest the money in a better investment option. Staying invested in ELSS funds beyond the lock-in period would ensure you increased returns due to the compounding effect.

Putting money in gold by investing in gold mutual funds, gold ETFs or sovereign gold bonds (SGBs) will ensure you an effective hedge against inflation other than earning returns higher than the inflation rate. However, gold investments must not exceed 10 per cent of your investments owing to relatively moderate earnings from them. Alternatively, you may invest a bit in silver and platinum though many personal finance experts advise against putting too much money in them owing to the extreme volatility in their prices.

Reinvesting your retirement corpus

Post-retirement, evaluate how much money you would need in the short run, say for the next five years. Invest the remaining amount in fixed-income instruments or those investment options that are relatively less volatile and hence are less risky than others.

The golden years of your life are for you to enjoy and make the most of your remaining time in pursuing your hobbies and interests ignored to date. However, enough money in hand is a precursor to your much-needed financial security. This is important as money though cannot buy happiness can surely help you find ways to be more content in your life.

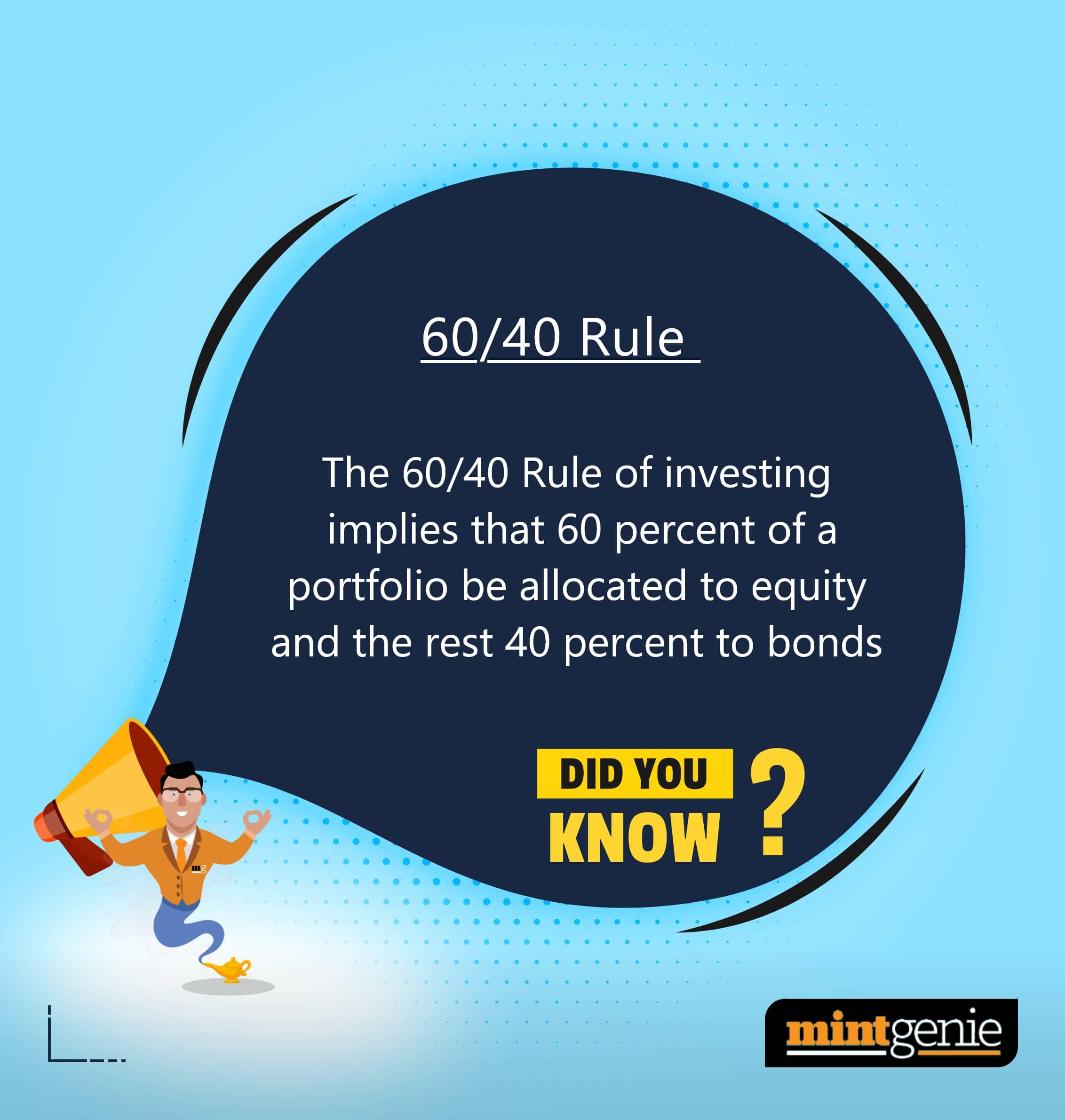

The 60/40 rule of investing implies that 60 per cent of the portfolio be allocated to equity.

First Published: 27 Sep 2022, 08:44 AM IST

Related Stories

personal finance

Looking to invest in National Pension Scheme? Here are the best NPS plans in terms of returns in the last year

Team MintGeniepersonal finance

Porting Annuities: PFRDA holds discussion with IRDA; Here's what happened

Team MintGenie

Explain Like I am 5

personal finance

PFRDA's assured return scheme in final stages; launch may take another few months

Team MintGeniepersonal finance

NPS Tier II: When a retirement fund works like an investment scheme too

Team MintGenie