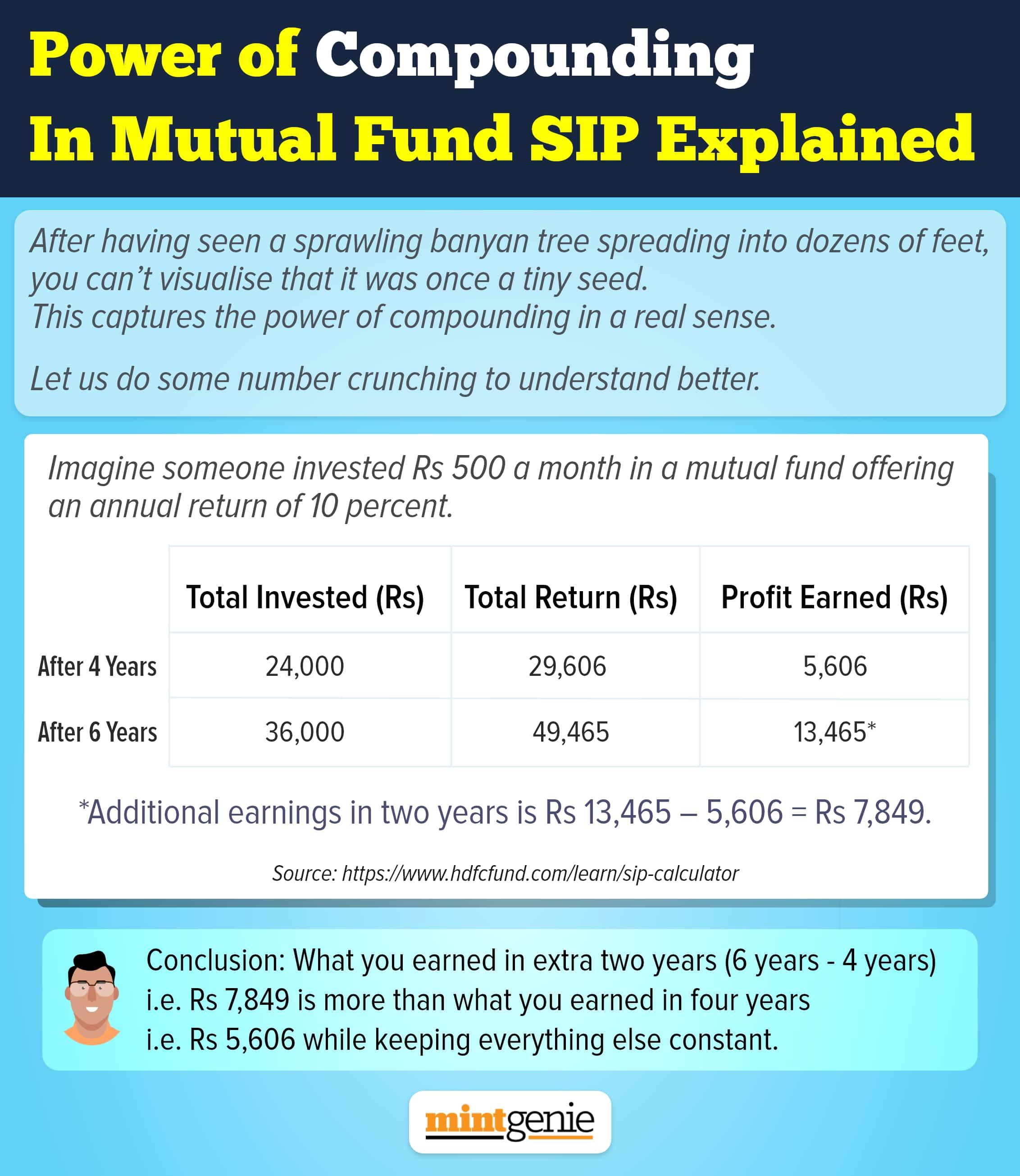

Most individuals invest in various financial products with the motive of getting the highest possible return on investment. However, the choice of financial products depends on the investor’s risk profile. Accordingly, the investor has to factor in the expected rate of return based on their risk profile. In this article, you will understand how the expected rate of return impacts the final corpus you will accumulate.

Risk profiling: Before we understand the impact of the expected rate of return on the final corpus, you need to understand the risk profiling of investors. It is the investor's risk profile based on which the financial products for investment are selected. Further, it is the financial products based on which the expected rate of return depends.

Based on risk profile, investors can be categorised into three broad categories:

Aggressive: An investor with an aggressive risk profile has a high-risk appetite. These investors can invest in financial products that carry high risks, such as equity mutual funds or credit-risk debt funds. These investors expect high returns to compensate them for the high risk they are taking.

Conservative: An investor with a conservative risk profile has a low to no appetite for risk. As a result, these investors invest in financial products that are safe or carry very low risk. Usually, they have to be content with low returns. They usually choose from fixed-income products, such as bank fixed deposits, bonds, debt mutual funds, and small saving schemes (PPF, NSC, etc.)

Moderate: An investor with a moderate risk profile sits between an aggressive and a conservative investor. So, they can neither take high risks nor are content investing in low-risk, low-return financial products. They can consider investing in hybrid mutual funds that invest in a combination of equity and fixed-income products. The proportion of equity and debt may vary across different products and may be managed dynamically by the fund manager. Over the long term, the returns from hybrid funds are usually higher than debt products, but lower than equity products.

Impact of the expected rate of return on the final corpus

In the earlier section, we understood the risk profiles of investors, the financial products they may invest in, and the kind of returns they can expect. Let us now understand how the expected rate of return can impact the corpus you will accumulate.

Rani, Sheela, and Asha are investing for their retirement in the following manner:

- Rani has an aggressive risk profile and chooses to start a SIP with Rs. 5,000/month in an equity mutual fund for 20 years and is expecting a return of 12% CAGR.

- Sheela has a moderate risk profile and chooses to start a SIP with Rs. 5,000/month in a hybrid mutual fund for 20 years and is expecting a return of 10% CAGR.

- Asha has a conservative risk profile and chooses to start a SIP with Rs. 5,000/month in a debt mutual fund for 20 years and is expecting a return of 8% CAGR.

Let us see how much amount they will accumulate

Investor | Monthly investment | Investment time horizon | Expected rate of return | Accumulated corpus |

Rani | Rs. 5,000 | 20 years | 12% CAGR | Rs. 49.96 Lakhs |

Sheela | Rs. 5,000 | 20 years | 10% CAGR | Rs. 38.28 Lakhs |

Asha | Rs. 5,000 | 20 years | 8% CAGR | Rs. 29.65 Lakhs |

As seen in the above table,

- Rani will accumulate the highest amount of Rs. 49.96 lakhs as her investment gives the highest return of 12% CAGR.

- Sheela will accumulate Rs. 38.28 lakhs as her investment gives a return of 10% CAGR.

- Asha will accumulate the lowest amount of Rs. 29.65 lakhs as her investment gives the lowest return of 8% CAGR.

The general rule is the higher the return on investment; the higher will be the amount accumulated, other things being the same. But, in high-return financial products, the risk involved is usually higher. Similarly, financial products with a sovereign guarantee or low risk usually give lower returns.

Factors that influence the risk profile of an investor

In the earlier section, we saw how individuals with an aggressive risk profile can take high risks and have the potential to earn higher returns. However, an individual's risk profile can change over a period of time or due to certain factors. Some of these factors include:

Age: Usually, as a person ages, the risk appetite diminishes. For example, most individuals have a high-risk appetite when they are young. As their age increases, their risk appetite usually reduces with every passing year.

Financial liabilities and responsibilities: Usually, as a person takes on big financial liabilities, such as a home loan, it may impact their risk-taking ability. Similarly, when a person gets married and becomes a parent, their risk-taking ability may reduce.

Over time, with increasing age and other factors, as the risk appetite reduces, the individual may rebalance their investment portfolio by reducing equity exposure and increasing debt exposure. Due to a change in the above investment portfolio, the investor will have to reduce the expected rate of return.

Start early to benefit from the magic of compounding

In this article, we have understood how the expected rate of return impacts the corpus that you will accumulate. The higher the return on investment, the higher will be the amount that you will accumulate. Among most financial products, equity mutual funds have given one of the highest returns, if not the highest, over long investment periods.

Hence, you should start your equity mutual funds investment journey early in your career, preferably as soon as you start earning. When you start early, you have age on your side and can afford to take higher risks and expect higher returns. Also, in the short run, equity markets are volatile, but in the long run, they have the potential to create wealth for you.

Gopal Gidwani is a freelance personal finance content writer with 15+ years of experience. He can be reached at LinkedIn.