There is no better feeling than motherhood in the world. The joy of being able to bring life to fruition is second to none. As we observe Mother’s Day on May 14 this year, let us ring in the celebrations with a popular adage by an equally popular author Robert Browning, “All love begins and ends here”.

Mother’s Day 2023: How can mothers plan their retirement with mutual fund investments?

TL;DR.

Enjoy motherhood but not at the cost of your well-being. Practice self-love by investing in yourself and for yourself while planning your child’s future and finances.

While we all talk about mother’s love and it being second to none like the yesteryear actress Kate Winslet aptly describes, “Mothers who work full time – they’re the real heroes”, we must also respect the need for self-love.

Mothers like you must practice self-love. This day is not about receiving gifts alone but also about gifting yourself the gift of self-preservation. The first step to self-care is ensuring self-preservation and this is possible only when you secure your mind and future well. Self-preservation is not possible unless you have adequate finances at your disposal.

Plan your retirement corpus

If you have a mind that functions well enough, you must know that all is not lost today and that you have a future too. There is a future that is awaiting you when you will be all old and experienced and hopefully financially independent too. Do not let the golden years of your life fade away in desperation for money and the frustration of rutting in financial instability.

Nisha Sanghavi, a Certified Financial Planner & Director, Promore Fintech said, “Women tend to live longer than men so it becomes an integral goal to plan and invest for retirement which most of them ignore.”

To have a financially secure future tomorrow, ensure that you plan your retirement well in advance. Set the groundwork for retirement early in life. This starts with deciding how much retirement corpus you would need to pay off your post-retirement expenses.

Know your financial goals

First, decide your financial goals. How much money do you wish to set aside as emergency corpus and essential spending before moving on to save and invest? Retirement is a long-term proposition, so you must consider your old-age expenses including estimated pension income, medical expenses, a trip to foreign locations, pursuing your hobbies, buying a comfortable home at a desired location, a possible entrepreneurial venture, and more.

Rajani Tandale, Product Head – Mutual Fund, 1finance.co.in said, “To calculate a sustainable retirement corpus, consider the following factors - Current expenses, inflation, expected rate of return, retirement age, life expectancy, and expected market return on investments. Use a retirement calculator to determine the corpus and monthly savings needed.”

| Retirement Corpus Calculator | |

| Current Age | 34 years old |

| Retirement Age | 60 years |

| Current Annual Household Expenses | ₹7,50,000 |

| Life Expectancy after Retirement | 20 years |

| Expected Inflation Rate | 8% p.a. |

| Returns Expected till Retirement | 12% p.a. |

| Returns Expected post Retirement | 9% p.a. |

| Annual Expenses at Retirement | ₹55,47,265 |

| Retirement Corpus Required | ₹101,787,864 |

| Monthly Investment Required | ₹47,319 |

| Source: 1finance.co.in | |

Sanghavi added, “Women generally take mini breaks in life, which I personally term as mini-retirements as the situation brings them into like - At start being single, getting married, having family, parents’ ailments lead them to take sabbatical, growing up children needs mother so women take breaks too and then it goes on and on. So during these breaks, corpus created through investment would come to the rescue. So, it is very important for women to invest and also take charge of their finances.”

Decide on your investments

Second, start by planning your investments once you have figured out how much money you might need. This means that you must not refrain from your retirement planning even while you may be enjoying your motherhood. The magic of compounding is not possible unless you lend enough time to your investments to grow and compound.

Choose your mutual fund investments

Third, since you are starting quite early in life, you may as well engage in some risk-taking by putting a part of your earnings in mutual funds. You just do not decide on your mutual fund investments suddenly. There are myriad parameters such as past 10-year returns, expense ratio, fund manager’s experience, portfolio allocation, portfolio turnover ratio, and more to decide which mutual fund would align with your financial goals and risk profile.

While deciding to invest in mutual funds, how should women, especially, mothers must decide which mutual fund category to opt for?

Pratibha Girish, Founder, Finwise Personal Finance Solutions said, “Firstly, invest for the long term at least five to seven years. Expect volatility, choose funds that are consistent in performance, protect the downside, and stick to the mandate. If you are unsure of the category select Flexicap to start with.”

If you are new to investing, you think of passive investing like allocating a part of your income to index funds. You may start either with any Nifty50 or Nifty100 or the S&P 500 Index fund that invests in a basket of stocks listed in a particular index. The stocks are listed in proportion to their market capitalization, thus, explaining how gradual stock market growth results in increased earnings over the period.

| Name of the fund | Three-year returns (in %) |

| HDFC Index Fund - S&P BSE Sensex Plan | 26.17 |

| Nippon India Index Fund | 26.08 |

| Bandhan Nifty 50 Index Fund | 26.69 |

| UTI Nifty 50 Index Fund | 26.68 |

| ICICI Prudential Nifty 50 Index Fund | 26.60 |

| Source: Kuvera.in | |

The risk appetite is the highest when young, especially for women in the age group 25-35 years and open to investing in the market. Their choice of funds can be from among the mid-cap and small-cap funds with some also resorting to putting their money in thematic funds for higher yields.

Some of the best-performing funds in these categories that have helped investors create wealth and accumulate a decent corpus in the long run include

| Fund category (as per market cap) | Name of the fund | Three-year returns (in %) |

| Small Cap category | Quant Small Cap Fund | 66.34 |

| Nippon India Small Cap Fund | 49.77 | |

| Canara Robeco Small Cap Fund | 47.83 | |

| ICICI Prudential Small Cap Fund | 47.53 | |

| Mid Cap category | Motilal Oswal Mid Cap Fund | 41.31 |

| SBI Magnum Mid Cap Fund | 41.14 | |

| HDFC Mid Cap Opportunities Growth | 37.39 | |

| Nippon India Growth Fund | 36.99 | |

| Thematic Fund category | Bandhan Infrastructure Growth | 40.93 |

| DSP India t.i.g.e.r. Growth Fund | 39.90 | |

| Aditya Birla Sun Life Infrastructure | 39.78 | |

| Franklin Build India Growth | 39.33 | |

| Source: Kuvera.in | ||

If you are aged above 40, you may then move on to putting your money in large-cap funds that yield good returns while being relatively less volatile in the long run. Many middle-aged investors not willing to take too many risks or expose their investments to continued market movements also prefer hybrid mutual funds for their stability and allocation to both equities and debt. The returns are however lower than their mid-cap, small-cap, and thematic fund counterparts.

| Fund category (as per market cap) | Name of the fund | Three-year returns (in %) |

| Large Cap Fund Category | Nippon India Large Cap Fund | 33.19 |

| HDFC Top 100 Fund | 29.51 | |

| SBI Blue Chip Fund | 28.35 | |

| ICICI Prudential Blue Chip Fund | 28.24 | |

| Edelweiss Large Cap Fund | 27.03 | |

| Hybrid Fund Category | Quant Multi Asset Growth Fund | 39.43 |

| ICICI Prudential Multi Asset Fund | 30.51 | |

| JM Equity Hybrid Bonus Principal Units Fund | 30.50 | |

| HDFC Balanced Advantage Growth Fund | 30.38 | |

| Edelweiss Aggressive Hybrid Growth Fund | 25.75 | |

| Source: Kuvera.in | ||

Most importantly, investment preferences change with time, and early starters may consider shifting their investments from one market cap to another. However, a lot depends on whether you have invested your money in other options too and how far you are from your financial goals.

Flexibility also matters, which is why women nearing their 50s shift their investments to risk-free options like debt funds, bank deposits like fixed and recurring deposits, and other schemes to ensure that their earnings are not wiped out due to unforeseen circumstances affecting the market or macroeconomic factors like war, epidemic, etc.

Focusing on asset allocation

You cannot ignore the importance of asset allocation while planning your retirement. This also explains why experts also ask investors to scan the portfolios of various fund houses to understand returns pursuant to them. Be aggressive about saving for retirement and invest more of your portfolio in funds following a high-risk-return approach. As you approach retirement, you begin to reallocate your capital from equities to debt. It doesn't matter whether someone uses index funds, mutual funds, or any other investment option like exchange-traded funds (ETFs) wherein you can trade baskets of stocks in the secondary market.

Undoubtedly, you must focus on your motherhood. But, also refocus on where you are headed in life. Your financial sanity is your priority, so make sure to secure your own finances as you secure your child’s needs.

As our forefathers always said,

"You can't pour from an empty cup, so take care of yourself first."

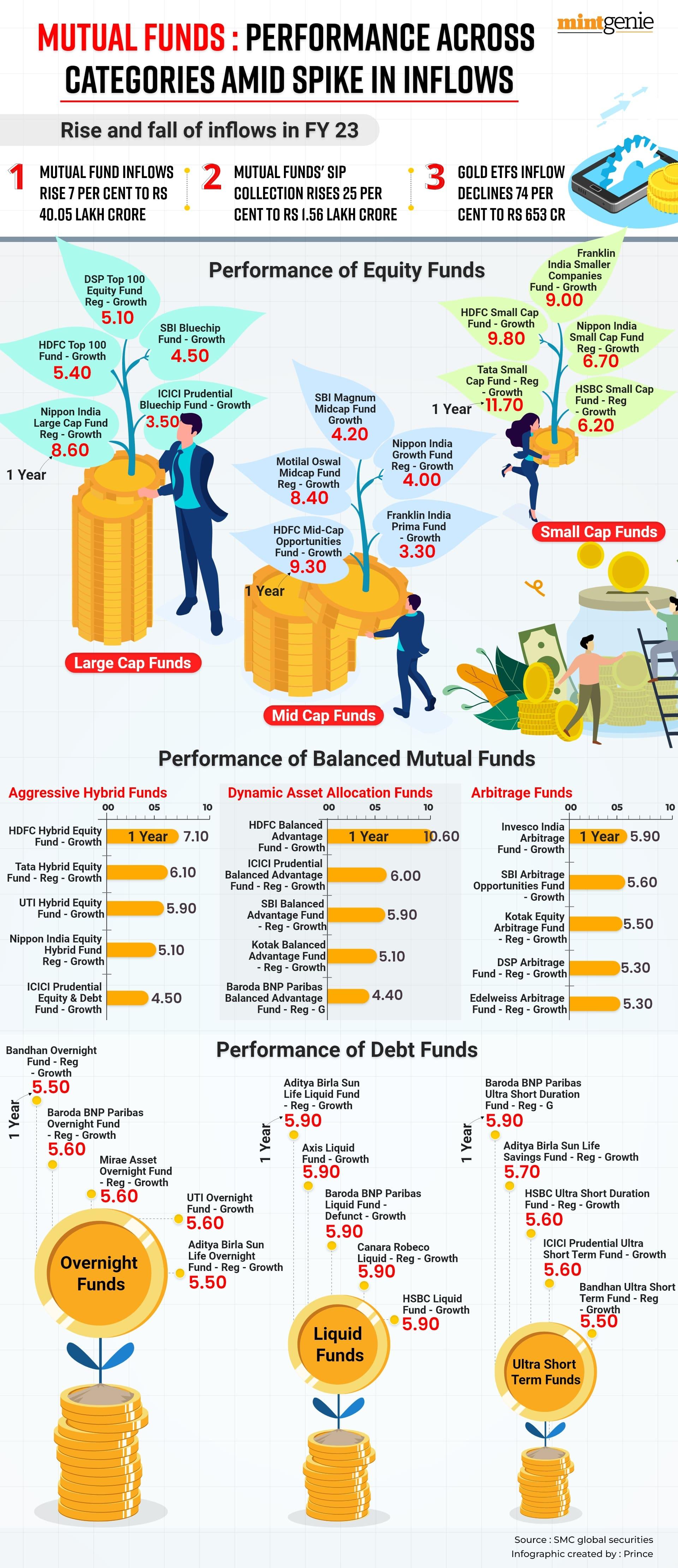

Mutual Funds' SIP collection rises 25 per cent to ₹1.56 lakh crore in FY23

First Published: 14 May 2023, 10:16 AM IST

Related Stories

personal finance

Mother's Day 2023: Why health insurance is a necessity for young mothers

Shreeraj Deshpandepersonal finance

Mother's Day 2023: 6 ways to plan your finances well in advance to enjoy your maternity break

Abeer Ray

Explain Like I am 5

personal finance

Mother’s Day 2023: 5 important financial lessons we can learn from our mothers

Abeer Raypersonal finance

This Mother’s Day, give your mother something that secures her financial future

Abeer Ray