When you start earning in your early or mid-20s, you must have a lot of ambitions to own material possessions, to travel, to buy your first car or to lay your hands on the latest smartphone in the market. Your first few months’ salary might fall short of the total expenses you have thought of. This calls for the need to buy these products on credit. For a salaried person, getting a credit card is nothing more than a walk in the garden.

But it can be a double-edged sword. Unless you know how sharp the sword can be, this financial weapon might hurt you badly.

So, read further to know how a credit card can be used, and what are the precautions that need to be taken before overleveraging it, and what consequences will you face if you miss the due date, so on and so forth.

Should you get a credit card?

If your monthly income exceeds your monthly expenses by at least 30-40 percent then you can take a credit card. It will take care of your credit card bills. And if you want a credit card only to meet the shortfall of your income against your expenses then it is clearly a bad idea to buy things on credit. Borrowing now to pay later without having a future income to pay is equivalent to kicking the can down the road.

What is a credit card billing cycle?

The credit card billing cycle refers to the monthly cycle during which all purchases made are added to the credit card statement. For instance, if a card’s statement is generated on the 10th of every month then the billing cycle will start from 10th of previous month and will continue until 9th of this month. This means all purchases made during this month are added to the statement.

Following this, the customer gets 15-20 days to make the payment. Let us assume the last date to make the payment is May 25 for the statement generated on May 10, this implies the customer has 15 days to clear his dues.

When a bank official claims that the customer will have 45 days interest free period, then s/he is referring to the 30 days of billing cycle and 15 days grace period to clear off the dues. So, something purchased on April 10 will be included in the statement released on May 10 – for which the customer will have time up to May 25 to make the payment.

How many credit cards are ideal?

There are several advantages for having multiple credit cards: higher capacity to spend, improvement in credit score and option of balance transfer. Let us explain how it works.

If you have three credit cards with a credit limit of ₹2 lakh each, then overall you have access to ₹6 lakh of credit. And if you are spending ₹3 lakh in total then you can stagger the expenditure across three cards. This way, each card will get 50 percent credit utilisation. This helps in the credit score.

Finally, you can transfer the credit from two cards to the third one under the process called balance transfer.

The number of credit cards depends on your credit needs. If your credit needs are high, you can apply for more than one credit card. This is good for your credit score. But beyond a point, this might also look bad because this means too many pending credit lines are open.

As a matter of fact, there is no definite answer to how many cards are ideal, although two is not too much if you have regular credit card bills and payments. It must be understood that applying for too many credit cards in a short span of time is not advisable because this is considered a method to manipulate the system by borrowing from one to pay the other, and sustaining the chain for a long time.

Another disadvantage of keeping too many credit cards is that you are likely to forget the bill or due date since keeping a track of too many due dates is not feasible. And one missed deadline can jeopardise your entire financial planning.

What should be the limit of your credit cards?

A credit card limit is the maximum due balance one is allowed to keep without having to pay a penalty for it. The banks, before determining credit card limit, factor in your income, existing outstanding loans and most importantly – your credit history. Usually, a customer does not know about the credit card limit until after filing out the form and submitting with the banks. As a rule, banks allow credit limit up to 3-4 times of card holder’s monthly income, subject to good credit score and not-too-high outstanding loans.

With the passage of time and after having paid credit card bills on time, the credit limits can be raised by banks unilaterally or even on the customer’s request.

At times, when the customer has a high credit expenditure lined up, he can either apply for more than one card, or can request for raising the credit limit. The purpose of both the options is to borrow less than the total credit limit available, so as to keep credit score high. Let us understand how this works.

When you have a credit card limit of ₹1.5 lakh on one card and expenses lined up for the same amount, then you can apply for raising the limit to avoid utilising 100 percent of your credit limit.

Let us assume you applied for the credit limit and it was subsequently raised to ₹3,00,000 then even after spending ₹1,50,000, you would have utilised only half of the total credit card limit. This is seen as a good practice, and a decent credit score follows.

How do credit card payments and usage affect your CIBIL score?

CIBIL is a credit information company that measures the creditworthiness of borrowers in India., It assesses the customers’ credit worthiness by a measure called CIBIL score — a three-digit number between 300 to 900 — to evaluate a customer’s ability to repay loans.

Limiting your overall credit card spend below 30 percent of your credit card limit is good for your CIBIL score. When you borrow more than this, it will adversely impact your credit rating.

When you make a purchase, you generally have a 45-day period to pay for that purchase. On the due date, you can either pay the minimum amount or the total outstanding for that month. When you make the minimum balance, you carry forward your dues for one month to the subsequent month. This way, you hamper your CIBIL score. On the top of it, you overburden yourself with interest which can be as high as 36 percent per annum.

What happens if you don’t pay by the due date?

When you do not pay by the due date, you roll over your dues to next month. This will attract interest on your outstanding balance every month. And it will continue to accumulate. For instance, if you made a purchase of ₹10,000 in a month, and by the due date, you don’t pay this bill- it will roll over to next month, drawing interest at three percent every month.

Credit card companies calculate their interest by the following formula:

(Monthly interest x 12)/365 (x) Credit card balance (x) number of days it took to make the payment.

This is meant to multiply the interest charged on each day by the number of days the customer took to make the payment.

Let us assume that you took six months to repay the money, you will end up paying 18 percent interest on the due amount, which will come to nearly ₹1,800, plus other penalty charges and 18 percent GST ( ₹324) on interest.

So, had you paid on the due date, you could have saved ₹2,124 ( ₹1,800 + 324). When you calculate interest at the compounding rate, the figure will be even higher.

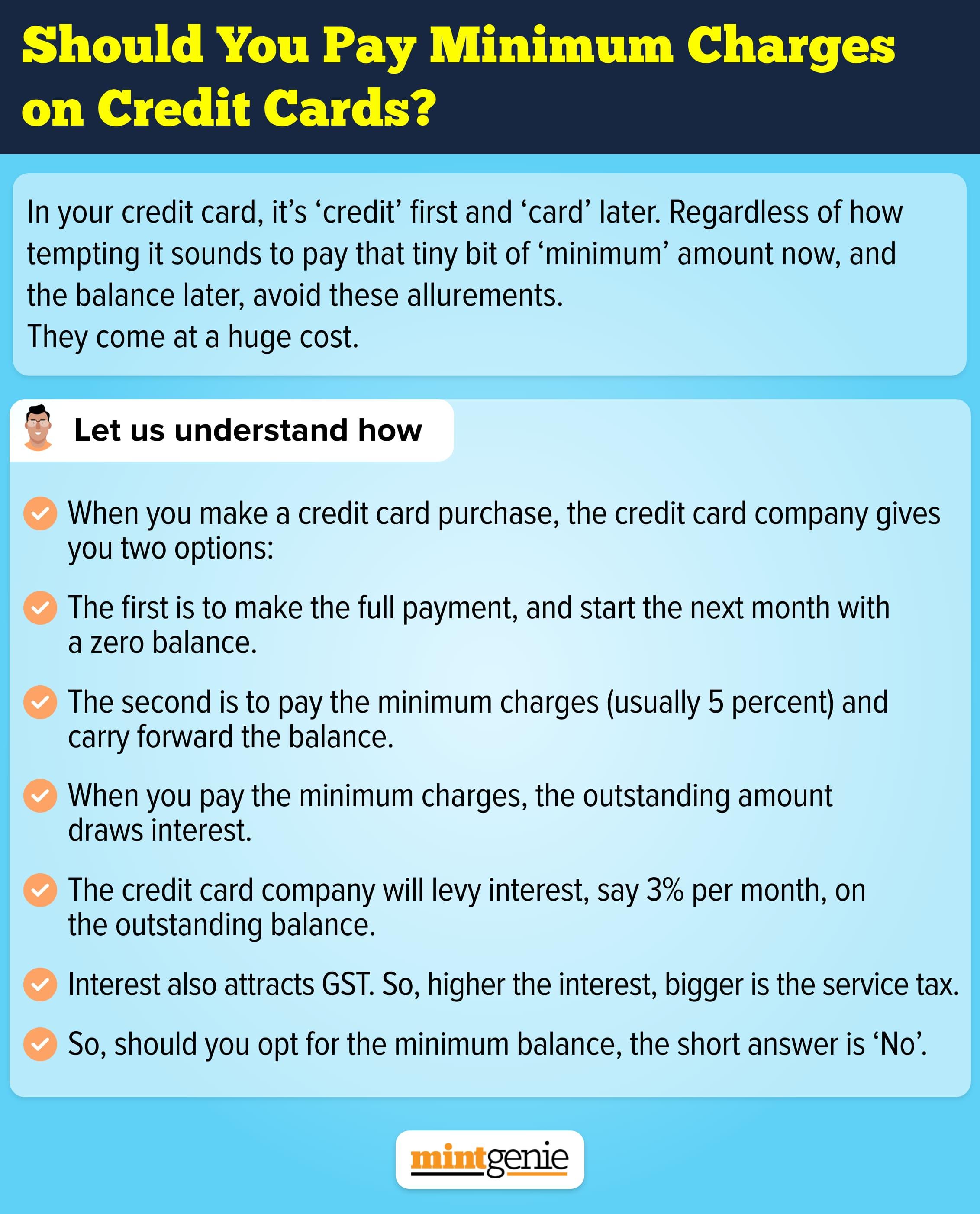

What's the minimum payment and should you opt for it?

When you make a credit card purchase, you are supposed to make the payment by the due date of the next month. The credit card company gives you two options, the first is to make the payment and start the next month with zero balance. The second option is to make the minimum payment (usually 5 percent of the total figure) and carry forward the balance to the next month. So, if someone asks whether you should opt for it, the short answer is ‘No’.

This is simply a way to procrastinate a due payment without having to face penalty charges. But it does not mean that the outstanding amount will not attract interest.

The credit card company will levy its usual interest rate, say three percent per month, on the outstanding balance. Not only this, the interest also attracts GST at the rate of 18 percent. So, higher the interest, bigger is the service tax.

Let us assume that you made a purchase of ₹4,000 and the minimum due is ₹200 (5 percent of ₹4,000). This will roll over the balance which is ₹3,800 to the next month. In the next month, your credit card bill will include the outstanding balance of ₹3,800 plus interest plus 18% GST on interest.

3,800 + (3 % of 3,800) X 118/100 =

3800 + 114 X 118/ 100 =

₹3800 + 134 =

₹3,934.

So, you will pay an extra ₹134 on a small amount of ₹3,800. And if you continue to roll over, the interest and GST will keep mounting.

What are the interest rates charged by credit card companies?

SBI Advantage plus credit card: The interest rate charged by this credit card is 2.25 percent per month.

HDFC Regalia credit card: The interest rate charged is 3.6 percent per month.

ICICI Bank Instant Platinum Credit card: The interest rate charged by ICICI bank on this card is on the lower side which is 2.49 percent per month.

Citibank Rewards Credit Card: The interest rate on Citibank credit card is 3.75 percent per month.

How credit cards lead to debt traps?

Make sure to pay your credit card bill on time. In case you miss a due date, the next instalment will include bills for two months plus interest for the previous month. If you postpone payment of the bill by a few months – the outstanding amount will rise significantly, practically pushing you into a debt trap.

Never try to buy time by merely paying the minimum due. Remember that this does not waive off interest on the outstanding amount.

Try to spot the early signs of a debt trap. The debt will not mount in one day. It gradually balloons week after week, and month after month. When you overlook the early signs, the day won’t be far when you will have too huge a debt to pay off.

Before you start to use a credit card indiscriminately and exhaust its entire credit limit, make sure that you have the means in the foreseeable future to repay the debt. The credit card money is not free money. They say that there ain’t no such thing as a free lunch.