Investors who want to earn a higher return vis-à-vis what is offered by a fixed deposit (FD) or even by a non-banking financial corporation (NBFC) can explore an alternative in peer-to-peer lending platforms.

Although these platforms are at a nascent stage in India, and there are not many popular names in the game, but the ones that exist include Faircent, liquiloans and LenDenClub.

LenDen Club invites investors on the portal by claiming that it has been offering 10-12 percent consistent portfolio returns for the past five years. On Faircent, lenders can earn anywhere between 12 to 28 percent return, states its website. The platform charges a non-refundable 2 percent transaction fee.

It is vital to note that these entities are not unregulated. The banking regulator Reserve Bank of India (RBI) treats these lending platforms as NBFC P2P.

The rules and regulations that steer these entities include the following: Company that runs these P2P platforms must maintain a minimum net owned funds amounting to ₹2 crore. The regulator has also set a total lending cap of ₹50 lakh for total exposure across all platforms.

Also, the RBI guidelines on Dec 23, 2019 state that the lender investing more than ₹10 lakh across P2P platforms will produce a certificate to P2P platforms from a chartered accountant.

Precautions to be taken

One must be clear of the fact that P2P lending is meant to help those who are desperate to borrow money. And investors can earn interest by lending to these borrowers temporarily and earn interest.

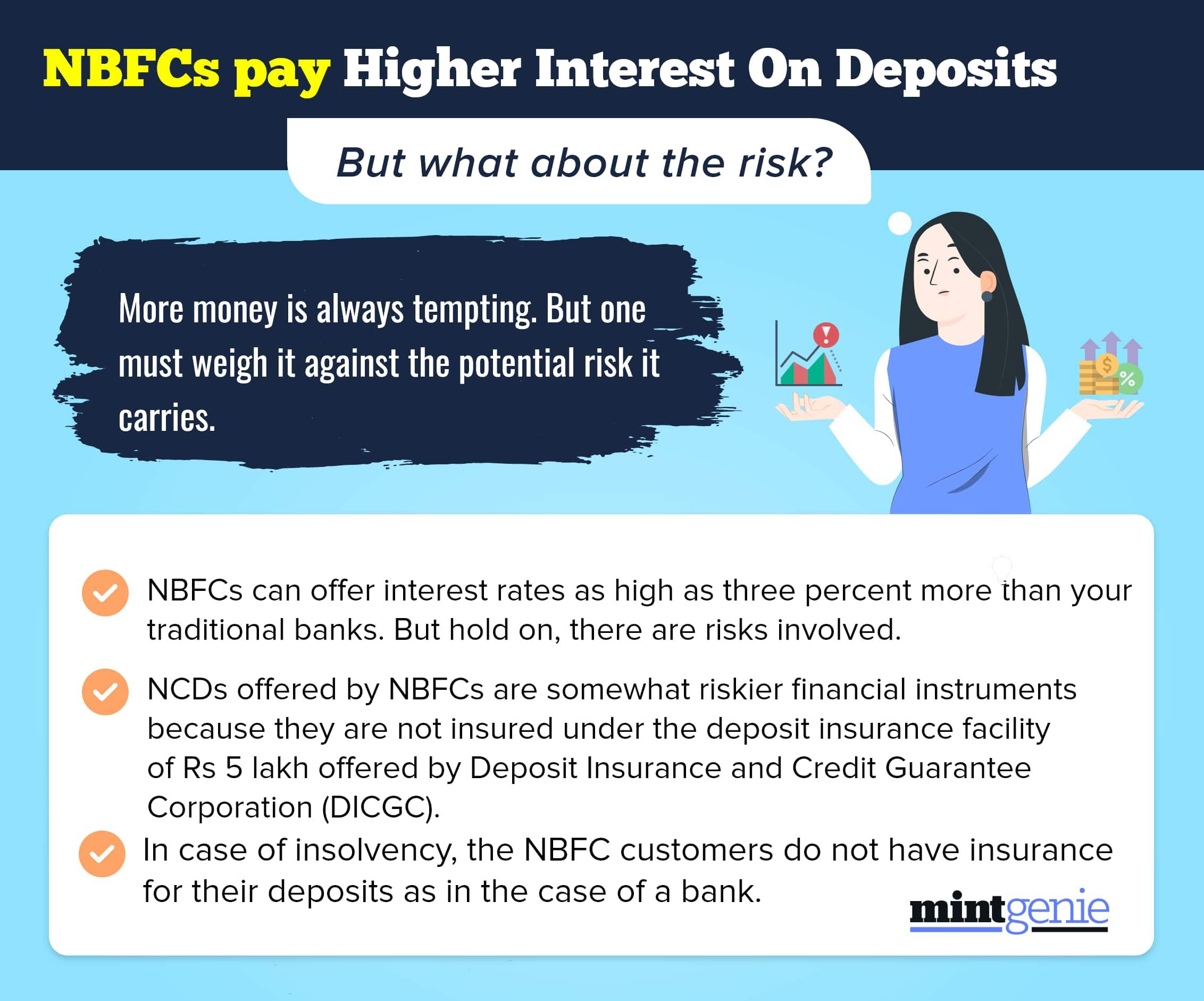

It, therefore, should not be seen as an investment product that offers high returns and hence cannot be compared with mutual funds or FDs. If a bank happens to default, one can recover the funds to the tune of ₹5 lakh by virtue of the insurance given by the DICGC (Deposit Insurance and Credit Guarantee Corporation).

And as one would know there is no such safety net for P2P lending. Hence once default takes place, it is not easy to recover the loan from the borrower.

However, these platforms claim that they adhere to stringent credit assessment for borrowers which is based on income, financial stability, repayment history and credit score.

However, it is important to note that the borrowers on these platforms come to these platform resulting from the difficulties in availing loans from traditional financial sources such as banks and NBFCs.

There could be a number of reasons for this such as weak credit profile or lack of any credit history. Consequently, they carry high default risk and are willing to pay interest rates, sometimes as high as 18-20 percent. So, it is not prudent to completely bank upon the methodology of risk assessment deployed by these platforms.

S Sridharan, founder and principal officer, Wealth Ladder Direct says, “There are two risks. One is that these platforms don’t have a proper collection mechanism of recovering the loans. And second is the high credit risk. These platforms usually get the customers who have a poor credit score. So, people should be careful about the principal coming back. Also, these platforms are in the nascent stage in India and it will take a long time before they become established.”

There is no wonder then at the time of lending, all the lenders are supposed to submit a declaration to P2P platforms that they have understood all the risks associated with lending transactions and that P2P platform does not assure return of principal/payment of interest, according to the RBI’s guidelines.