After many years of putting in a lot of effort, people are undoubtedly entitled to a joyful retirement, in which they may finally follow their passions or spend their golden years with their loved ones without worrying about work-related obligations. It is essential to plan for retirement well in advance to live a happy post-retirement life. So, to secure your financial future, you must make prudent investments.

Making a plan for your retirement guarantees that you have a backup income stream to cover regular bills, unexpected medical costs, or other financial crises.

Different investment options can help you plan for your retirement. Today, we will talk about pension plans offered by insurance companies and retirement mutual funds so that we can compare these two investment options.

But first, let us see what these pension plans and retirement mutual funds are.

What are pension plans?

A pension plan is a retirement strategy specifically created to offer investment and insurance benefits after retirement. As per this plan, you make regular investments while still working and build a corpus that can be used after retirement. The accumulated corpus can assist you and your family fulfil the needs that arise after retirement, and a well-chosen retirement plan can help you beat inflation.

What are retirement mutual funds?

Retirement mutual funds are solution-oriented mutual funds meant for planning retirement. The market regulator, SEBI, introduced this category in 2017 during the Categorisation and Rationalisation of Mutual Fund Schemes.

These hybrid mutual funds invest in a mix of equity, debt and other asset classes. To cater to the different investors in their different life phases, the retirement mutual funds come with three plans: aggressive, moderate and conservative.

Aggressive plans invest a significant part of their assets in equities, and the conservative plan has the lowest allocation to equities.

Differences between retirement funds and pension funds

Let us look at their differences so that we can understand both the investment options better.

Phases

As we have mentioned earlier, retirement funds have three plans to cater to an investor’s journey from a young investor with minimal financial responsibilities to an investor on the brink of retirement.

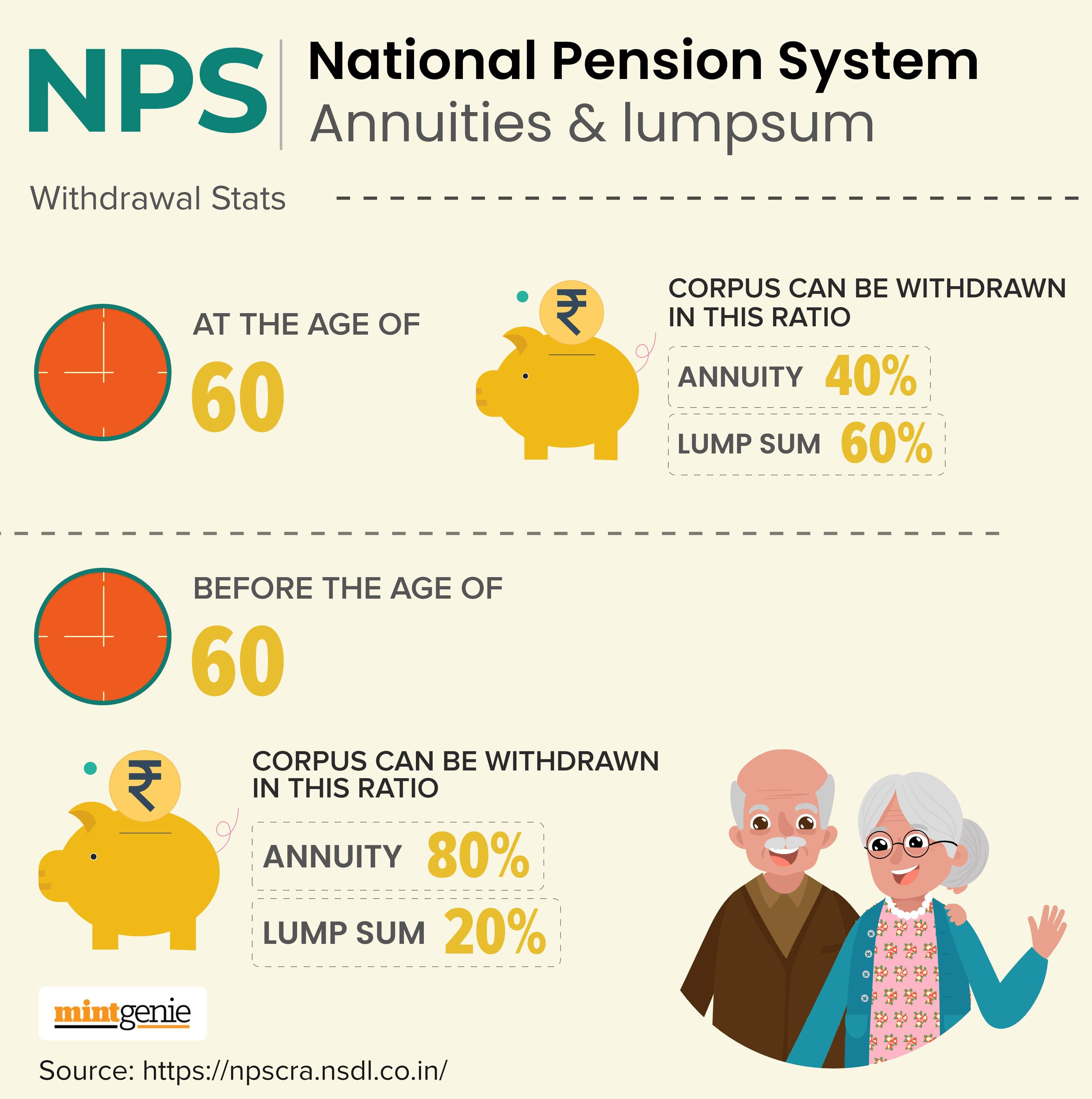

However, in the case of pension funds, there are two phases: the accumulation phase and the vesting phase. During the accumulation phase, the investors accumulate funds, and after retirement, when you receive money from your pension plan, you are said to enter the vesting period.

Annuity

Annuity is the fixed income you receive every month from your retirement investment option based on your overall contributions. After the contribution phase of the pension plan, you can buy an annuity plan to receive a fixed monthly income.

However, in the case of retirement mutual funds, there is no concept of an annuity. An investor can take a financial decision that best suits their requirements. Investors can continue investing in the fund and set up a Systematic Withdrawal Plan (SWP) that will transfer a fixed amount to your bank account while the rest of the investments will keep on growing.

Tax benefits

Contributions made to pension plans are exempted from tax under section 80C of the Indian Income Tax. Investors can invest up to Rs. 1.5 lakhs in a pension fund and get tax benefits.

However, the income in the form of annuities is taxable.

However, although retirement funds have a lock-in period of five years, investments made to retirement funds don’t have any tax benefits.

In case redemption takes place from a conservative plan after three years of investment, the capital gains are taxed at 20% after indexation. Capital gains on investments within three years are added to the investor’s income and taxed as per the income slab. We assume that a conservative plan has a maximum allocation to debt instruments.

Insurance cover

Insurance cover is available on the customer’s death if premiums have been paid without fail. However, retirement mutual funds don’t provide any insurance benefits.

Risk

Pension plans generally carry low risks. In the case of retirement plans, the associated risk will depend on the equity allocation of the plan. Aggressive plans carry higher risks as it has a higher exposure to equity and equity-related instruments than a moderate or conservative plan.

Flexibility

Pensions are not flexible retirement savings products. A pension is a predefined plan that cannot be changed once it is set up, and most pensions prohibit withdrawals during the accumulation phase. In contrast, you have the option to switch from one plan to another to invest in a plan that best suits your requirements.

Final words

When comparing insurance pension plans vs retirement mutual funds, it’s essential to consider your unique situation, financial goals, and attitude towards risk. These factors will affect the type of plan that is right for you.

Padmaja Choudhury is a freelance financial content writer. With around six years of total experience, mutual funds and personal finance are her focus areas.