It is increasingly common for millennials to loosen their purse strings by ₹one lakh on a smartphone and more than this on a premium laptop. Young professionals in metro cities have to battle a great peer-pressure to avoid joining a gym that charges a high membership fee, or to not buy a car which is at least as expensive as their neighbour’s, if not more.

Such compulsions, and many more, might help you move around with your head held high in your society, but financially speaking – these decisions are not only unwise, they are disastrous.

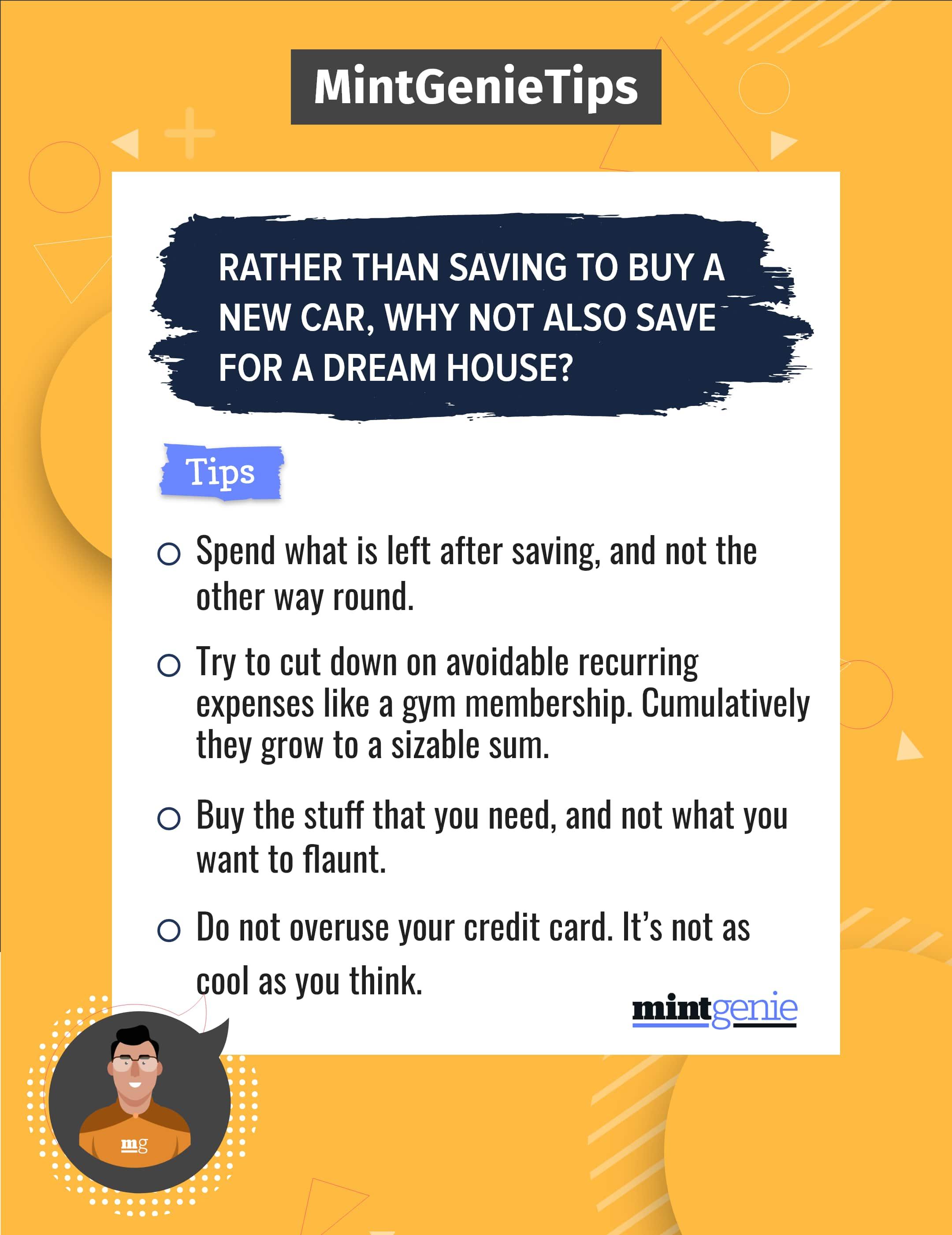

Although there is nothing wrong in buying an expensive smartphone or joining a premium gym, or driving a luxury car, but only if they don’t burn a hole in your pocket. Also, small expenses — more often than not — don’t matter much individually, but collectively, they make a sizable sum, and if invested rightly – can grow into a considerable amount.

Deepak Kumar Aggarwal, a Delhi-based financial advisor and chartered accountant, echoes the same sentiments. “I often tell my clients to cut down on avoidable expenses and increase their allocation to mutual funds or at least fixed deposits. Some of them don’t realise that there is an infinitely vast difference between expenditure and investment. While the former will simply go down the drain, the latter will return to you with sizable appreciation,” says Aggarwal.

How to save money

There could be a dozen reasons for you to cough up money to buy this product, take that membership or order something luxurious. And as we pointed out, everything should appear financially rational so long as it fits in your pocket.

The financial experts and money manager advise to avoid wasteful recurring expenses.

“It is the recurring expenses which are more harmful to your long term financial planning than the one-time expense. For instance, an amount of ₹4,000 a month might appear small, it accumulates to ₹48,000 a year -- with which you can buy 10 gms of gold. So, instead of wasting ₹4,000 a month, you can buy a small piece of jewellery at the end of the year,” explains Deepak Kumar Aggarwal.

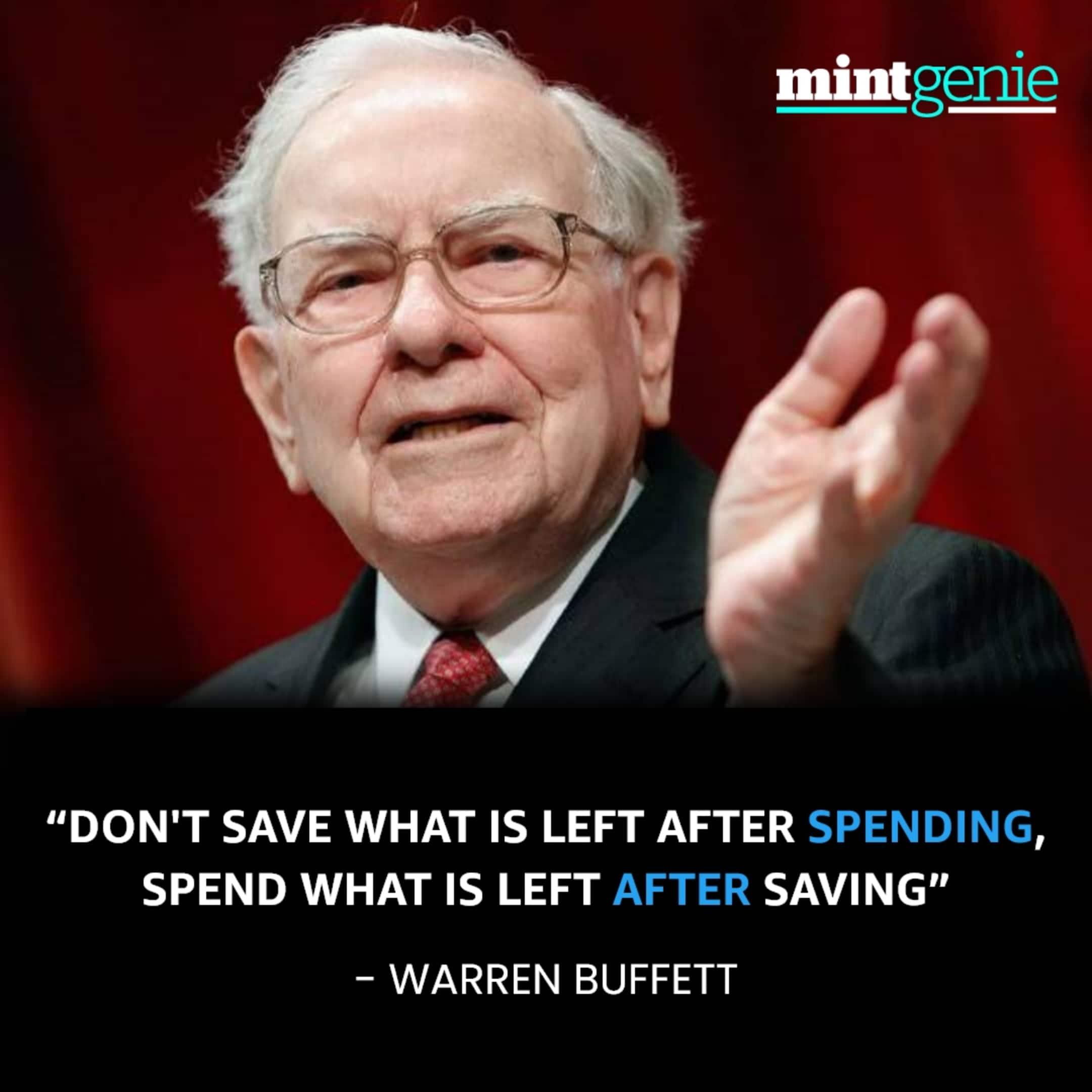

Ace investor Warren Buffet once said, ‘Don’t save what is left after spending. Instead spend what is left after saving.’ Let us understand this with an example. Suppose, you have come to a conclusion that you must keep ₹30,000 per month aside to meet your long term financial obligations such as buying a house and car, paying for your child’s education and saving for retirement, then there shouldn’t be any reason whatsoever to spend more, leaving you with less than ₹30,000 in your hand every month.

So, unless you stick to this personal finance rule, you are unlikely to save adequate money that would meet your financial and retirement goals.

Need Versus luxury

In a quest to save money, remember that you don’t have to compromise your quality of life. Some expenses are avoidable, while some are, in fact, an investment of sorts, and would bear fruits in the long run. For example, someone could be a passionate photographer who visits wildlife sanctuaries and national parks to unwind from work’s monotony.

For this person, spending ₹50,000 on a smartphone that also doubles as a camera may be a rational decision, instead of spending far more money on a digital camera.

Similarly, joining a gym that charges an affordable fee to stay healthy is undoubtedly better than paying huge medical bills should you fall ill.

Likewise, spending a huge premium on a cashless medical insurance policy for your entire family might appear to be an avoidable expenditure every year. But remember that this huge premium can save your fortune, should anyone in the family get bedridden.

So, we can highlight that high or low prices of a material possession is completely subjective and it depends on the size of your wallet. Something which might look cheap to someone may be prohibitively expensive for you.

And whenever you are set to overspend to satiate your instincts, remember the timeless words of Benjamin Franklin — ‘a small leak can sink a great ship’.