Sukanya Samriddhi account is a popular savings instrument amongst Indian parents with daughters. And rightly so. An ultra-safe, government-guaranteed instrument that gives tax-free returns. But will just opening a Sukanya Samriddhi Yojana (SSY) account for your daughter’s future be enough?

The answer is no. And there are a few reasons for it, which we shall see in a bit. But please understand that the Sukanya account is a solid product. But what I am trying to highlight here is that considering the rising costs of education and marriage expenses, chances are high that just saving via Sukanya may not be enough and you would need to invest more elsewhere.

Gives 7.6% now. But not forever. And not enough.

The Sukanya Yojana currently gives 7.6% interest. But if you look at the rising cost of higher education, it will be obvious that it often has very high inflation. So your investments in this will generate debt-like returns and will not be enough to beat inflation that applies to goals like higher education, marriage, etc.

Also, the rate is currently at 7.6%. But this is not fixed for the entire tenure as the government resets it every quarter. And just to refresh your memories, the scheme was launched with initial rates of 9.1 percent! So it’s possible that in a few years, if the broader rate trajectory of the economy is downwards, then even Sukanya rates will grind down to lower levels.

The tenure of this policy is in decades (21 years to be specific). So basically, this product is designed for the long term. And if you think objectively, then your best bet to generate inflation-beating returns in the long term is equity. So if your daughter’s goals are more than 10 years away, then you should be investing more in equity funds and less in debt, unless of course, you are a very conservative saver.

Being in the wrong asset for very long can result in inadequate savings and this is a risk that you would never want to get exposed to when dealing with children’s future. Right?

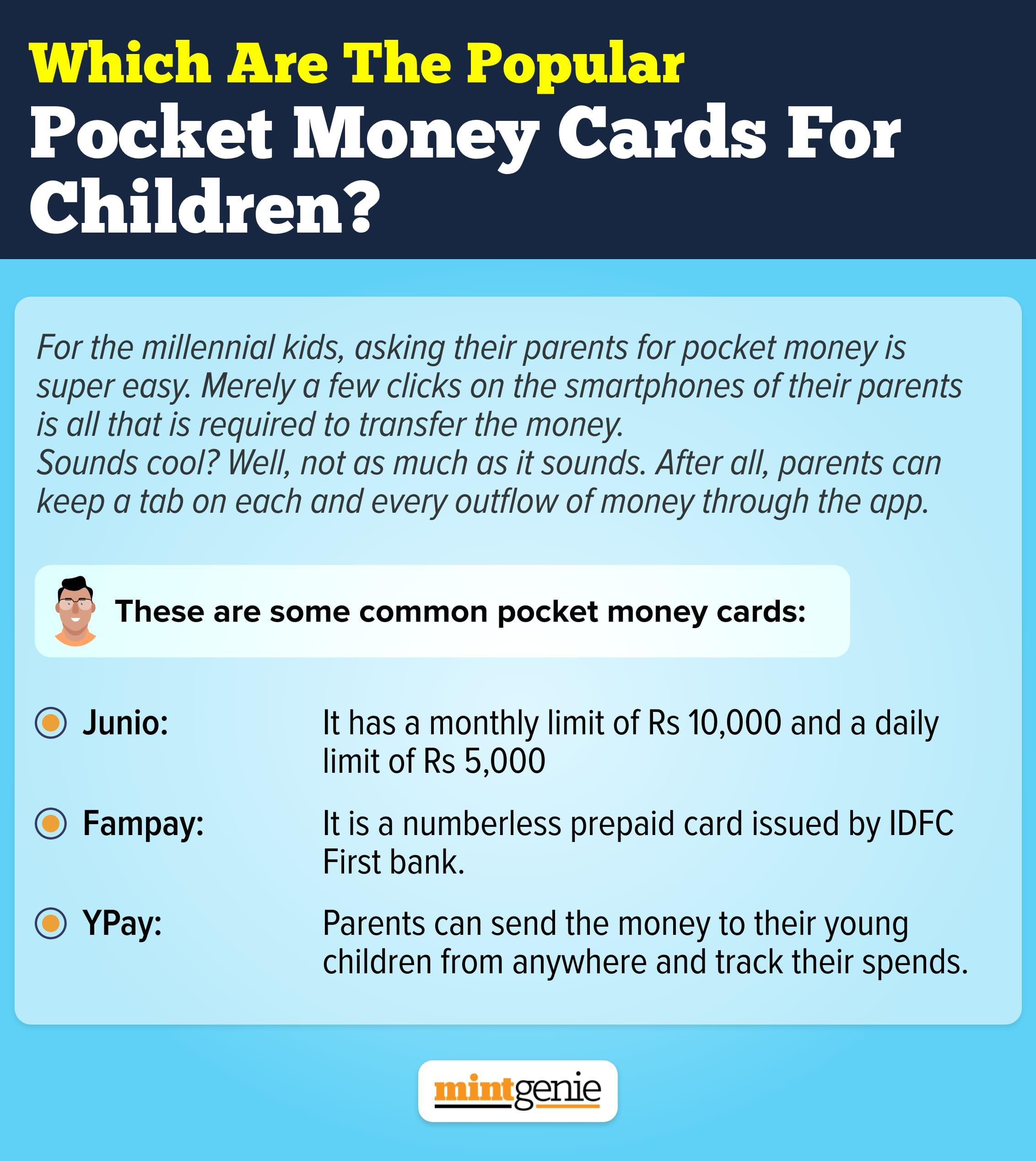

READ MORE: Mutual Fund Returns: These children’s funds fetched over 16 percent in 3 years

Strange restrictions in sukanya rules

The government wants the money saved in Sukanya to be used for daughter’s education and marriage only. To be fair, these are the major goals that most Indian parents save for.

But the structure of an SSY account is such there are few restrictions and rules that make it less investor friendly. Let me explain.

From the date of account opening, the Sukanya account has a tenure of 21 years (till girl’s marriage). Some people get confused and feel that it's about age 21 for the girl child. But that is not the case. The tenure is 21 years from the date of account opening. Also, the entire corpus is locked-in till the girl attains the age of 18. And even then, only up to 50% can be withdrawn for higher education expenses. But what you need much more for your daughter’s higher education than that? So this restriction can be a problem when you need money.

Another strange rule is that you can only make deposits till the 15th year. So, the account tenure is 21 years but you can only make deposits for the first 15 years and not the last 6 years! The corpus will still generate returns for the full 21 years. But why this restriction to invest only till the 15th year? What if you want to save more?

READ MORE: Saving early for your child's studies: 4 key points to remember

What is the solution?

When you are investing with such a long investment horizon, then you should always have some allocation to equity. By ‘some’ I do not mean 100%. You can always use Sukanya as one of the investments for your daughter. But the other choice can and should be equity funds.

Your next question might be how to divide your investments between Sukanya and equity funds?

Depending on your risk appetite, you can choose one of the following strategies:

- Aggressive – Put 70-80% in equity funds and 20-30% in Sukanya Account

- Balanced – Put 50-60% in equity funds and 40-50% in Sukanya Account

- Conservative – Put about 30% in equity funds and 70% in Sukanya Account

Remember that goals like education, experience high inflation. And even though Sukanya will give predictable returns, it will still be less than what inflation might be. So please add a dose of equity to your daughter’s portfolio to get an overall higher return than what would be possible if you went only with the SSY account.

Dev Ashish is a SEBI-Registered Investment Advisor and Founder (Stable Investor). He provides fee-only financial planning and investment advisory services to small and HNI clients across India.