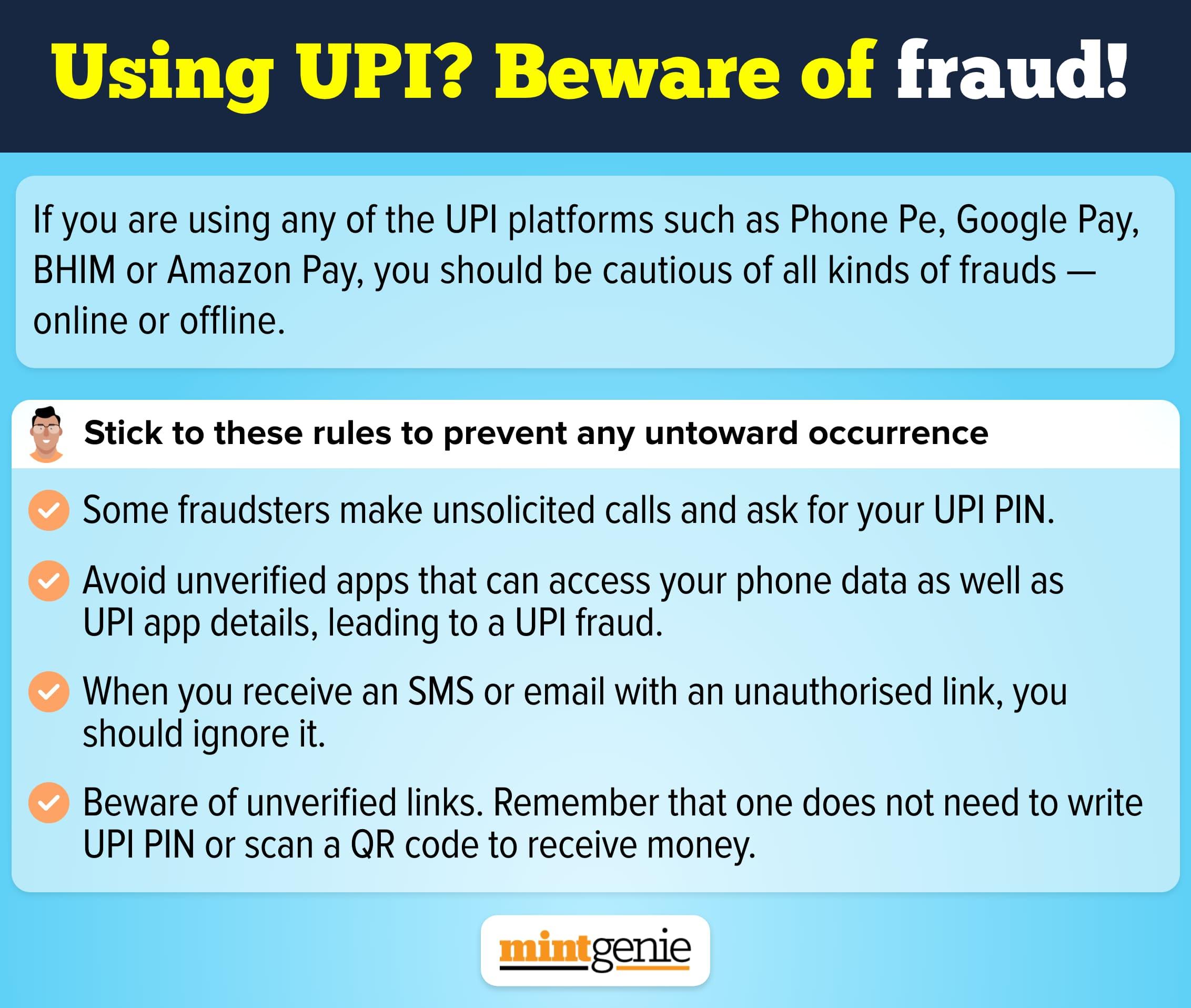

They say that the excess of everything is bad. But when it comes to UPI payments, the age-old maxim ceases to apply. For almost every small transaction, consumers have migrated to the Unified Payment Interface (UPI) and have stopped using cash for almost all purposes whatsoever.

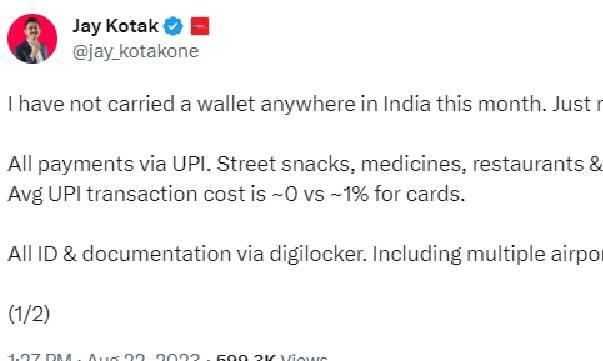

Jay Kotak, co-head of digital bank Kotak 811 and son of Uday Kotak, posted on X (formerly twitter) that he did not carry a wallet anywhere in India during the entire month and instead carried only his mobile phone.

He claimed to have made all payments via UPI including those for street snacks, medicines, restaurants and even tips.

And he is certainly not alone. From students to young professionals, small vendors to auto wallas and tea stall operator to momo sellers – everyone gives the option of making online payment via UPI. And most customers seem to be availing the option, too.

This growing phenomenon seems quite evident when you scan through the monthly statistics shared by the NPCI (National Payments Corporation of India).

Undoubtedly, number of UPI transactions has been growing month after month and year after year. In July, the total value of UPI transactions stood at ₹15.34 lakh crore, reporting a 44 percent year-on-year growth.

In terms of number of transactions, the figure was 9.96 billion, reporting a 58 percent year-on-year growth.

UPI is projected as a success story of India’s digital infrastructure around the world.

From Bhutan to Nepal and UK to UAE, several countries have adopted UPI enabled payments, thus expanding the global footprint of Indian digital payment system.

During his recent visit to France, PM Narendra Modi announced that Indian tourists will be able to use UPI during their visit to Eiffel Tower.

When Germany’s Federal Minister for Digital and Transport Volker Wissing came to India recently, he experienced the convenience of UPI first-hand as he made a small payment to a vegetable vendor through UPI. The video of making the payment was also shared on X by German Embassy India's official handle.

Counter-intuitively, it can be seen as an unhealthy practice to follow everywhere all the time.

Let us explain why.

1 Bank statement: First of all, when you make every payment digitally, then it is recorded as a bank transaction. It leads to a longer bank statement at the end of the week, month, quarter and year.

Imagine when you make nearly 10-15 transactions every day digitally, your monthly transactions can be anywhere between 300 and 450. So, six months later, if you are asked to send your bank statement for the purpose of raising a loan or something else, your statement may run into 200 odd pages.

2 Leaving a digital trail: When you are making every payment digitally, you are leaving a digital trail of what you did, where you went, what you ate, even how much you ate, and how many times you did that, so on and so forth.

On the face of it, this appears harmless but when you understand the magnitude of data it generates, and how it can be used to manipulate your buying behaviour online through targeted adverts, you will definitely be more surprised than amused.

3 Extra spending: It has been asserted adequately enough and empirically proven that making payment digitally usually leads to a higher monetary outgo vis-à-vis making payments in cash.

In other words, when you don’t see the physical money leaving your wallet, you end up spending more. On the other hand, when you make payments in cash, your monetary outgo is likely to remain in moderation.

4. Technological dependence: When you depend on your mobile device for every transaction under the sun, you are running the risk of putting all your eggs in one basket.

In case your phone gets conked off, gets infected by a malware or the worst of all – gets lost, you are prone to get stranded.

So, we can say that making payments in cash sometimes is not only a good habit but can really be a saviour particularly on the occasions when your smartphone doesn’t remain ‘smart’ anymore.