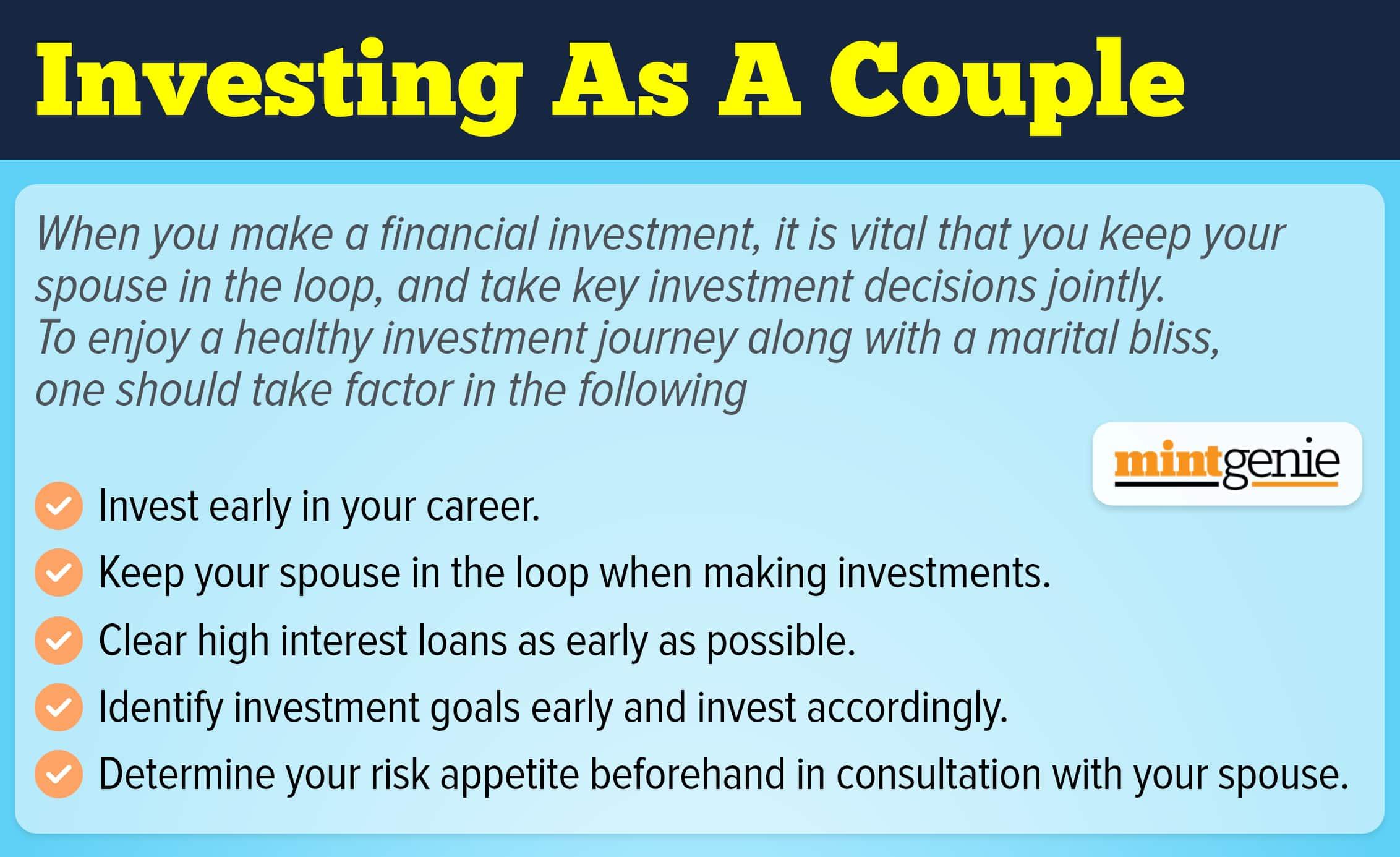

When you are in a committed relationship, you are likely to be saddled with an immense emotional stress to live up to your partner’s expectations, almost every day.

You may not express your love everyday — well even if you can, you will run out of the right words after a few successful attempts. So, some try to compensate for it by giving a physical gift, or through symbolic gestures like giving access to their finances including debit card and internet banking.

These things will surely cheer up your partner initially, and you will get full marks on loyalty, trust and love quotient. But as far as financial prudence is concerned, you become far more vulnerable than earlier.

Let us imagine a few hypothetical scenarios:

Case 1: Tina and Ravi are a couple and they decide to share their net banking passwords and the credit card details – besides those of their social media accounts. Well, their seamless social media access to one another can bolster their loyalty for each other – but the net banking!?

Ahem! Ahem! This can open a can of worms because if the love disintegrates later, the first thought that would cross your mind would be to change your password before all hell breaks lose.

Case 2: Tina and Ravi are a couple and they have a common bank account and common pool of money where they save and invest. Tina spends money wisely, doesn’t believe in overspending and saves little whenever she can.

On the other hand, this fella Ravi may have a lot of love for Tina, but not for her habit of saving and investment. This, whether they like it or not, will soon become a source of argument between the two every other day. So, what probably started with a good intention will have severe consequences.

Case 3: Tina and Ravi are a couple where Tina earns three times of what Ravi earns. When they open a joint account and manage their finances together, they commit to cough up 20 percent of their incomes every month. While Ravi is taking out one-fifth of his income as promised, but it is paltry in comparison to Tina’s share.

So, although each partner is doing the best they can, it falls short of the other’s expectations. Again, this can be a source of discord in the time to come.

Case 4: Tina and Ravi are a couple and they take joint investment decisions, and because of collective thought process, they may take some wrong bets and lose a significant amount of money. Despite two incomes they will be headed for a big trouble since they were walking the same road. Making individual investment decisions is similar to diversification which Tina & Ravi missed.

As we saw, finance is an extremely personal matter, and it may not always be in the best interest of the couple to jointly manage their finances as one.

At the same time, it is not completely irrational to take joint decisions. As they say – it is good to listen to everyone around you, but you should eventually take a call based on what you think is the best move.