There are a number of ways to invest in equities. Apart from direct investment and mutual funds, Portfolio Management Service (PMS) is another way to go.

PMS is an investment service where investors get the ability to tailor a portfolio as per their investment needs and financial targets. It offers investors control over the choice of portfolio they want. It is mostly an investment choice for big investors who have a large capital.

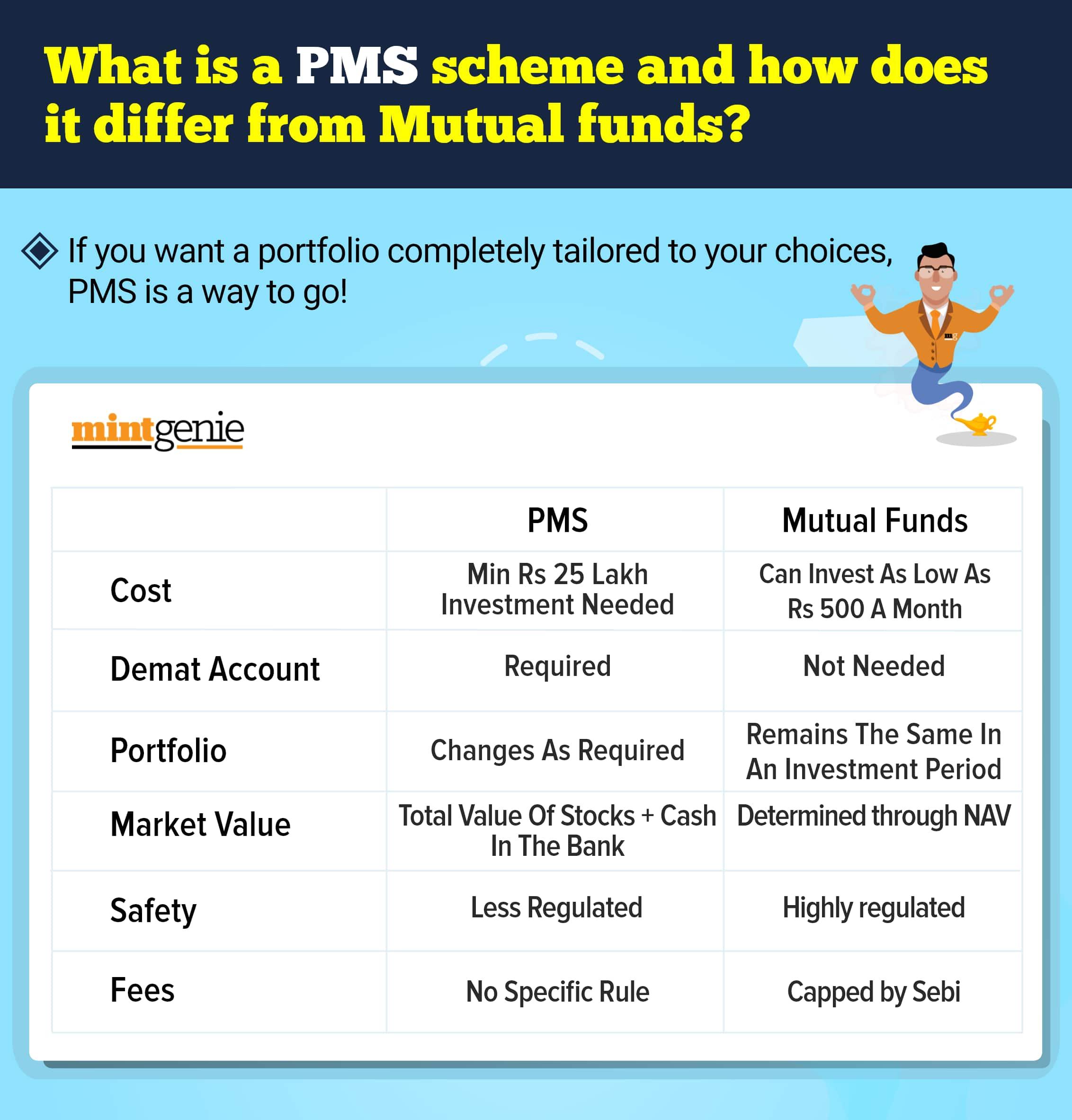

So how is it different from mutual funds?

1) The main point of difference comes in the cost. To invest in a PMS, an investor needs a minimum of ₹25 lakh, in some brokerages, this amount is even ₹50 lakhs, while to invest in an MF, you can start as low as a ₹500 SIP.

2) To invest in mutual funds, you do not need a Demat account. It is a basket of stocks where a number of investors invest. Meanwhile, for a PMS, you need a separate Demat account, as well as a different bank account, and the investor base is very low as compared to mutual funds.

3) While in mutual funds, the pool of stocks invested in stays the same throughout the investment period, in PMS a more customised approach is offered. The investors are more active in the choice of stocks and that is reflected in their portfolio.

4) In a mutual fund, the market value is determined by the Net Asset Value (NAV) of the units held whereas, in PMS, it is the sum of the total market value of the stocks held in the investor's Demat account and the cash in the bank account.

5) Mutual fund charges are capped by the market regulator Sebi whereas the fees for PMS have no specific Sebi guidelines.

6) There is also tighter regulatory control on mutual funds as compared to the investments through PMS which makes MFs safer.

7) In PMS, investors own shares in their name while in a mutual fund, the investor owns units of the scheme. The shares are in the name of the mutual fund rather than the investors.

8) Transparency is a benefit in PMS. The investor will know of all the purchases made as well as the sale of shares. He will also be aware of the date of transaction, fund manager fees, which stock made money, which stocks lost money, etc. PMS offers full transparency in money terms. of the transaction, portfolio manager’s exact fee amongst others. However, in mutual funds, the investor is not aware of all the portfolio changes when they happen. They get a monthly report of final holdings and total expenses.

9) Also, unlike mutual funds, PMS is not set in stone in regards to holdings. If the fund manager senses a loss, he can very easily sell the needed shares which helps avert risk. Fund managers are allowed to take aggressive calls to maintain a 100 percent cash position if needed. However, this is not the case with MFs. Such aggressive decisions cannot be taken in the case of an MF, since the investor base is very large. Generally, for the investment period, MFs stick to the portfolio at hand and try to cover losses in the long term.

10) Taxation is a benefit for MFs. In MFs, fund managers do not have to incur any tax when they buy or sell shares in the scheme, but in PMs, investors will be taxed by capital gain or loss on the sale of a share.

11) PMS managers are directly answerable to investors if they lose money since the scheme is tailored to suit the investor's need and for wealth creation. Meanwhile, mutual fund managers do not have any such obligations to their investors.

Now that we know the difference between mutual funds and portfolio management services, it is important to clearly analyse your goals and capital position before deciding where to invest.